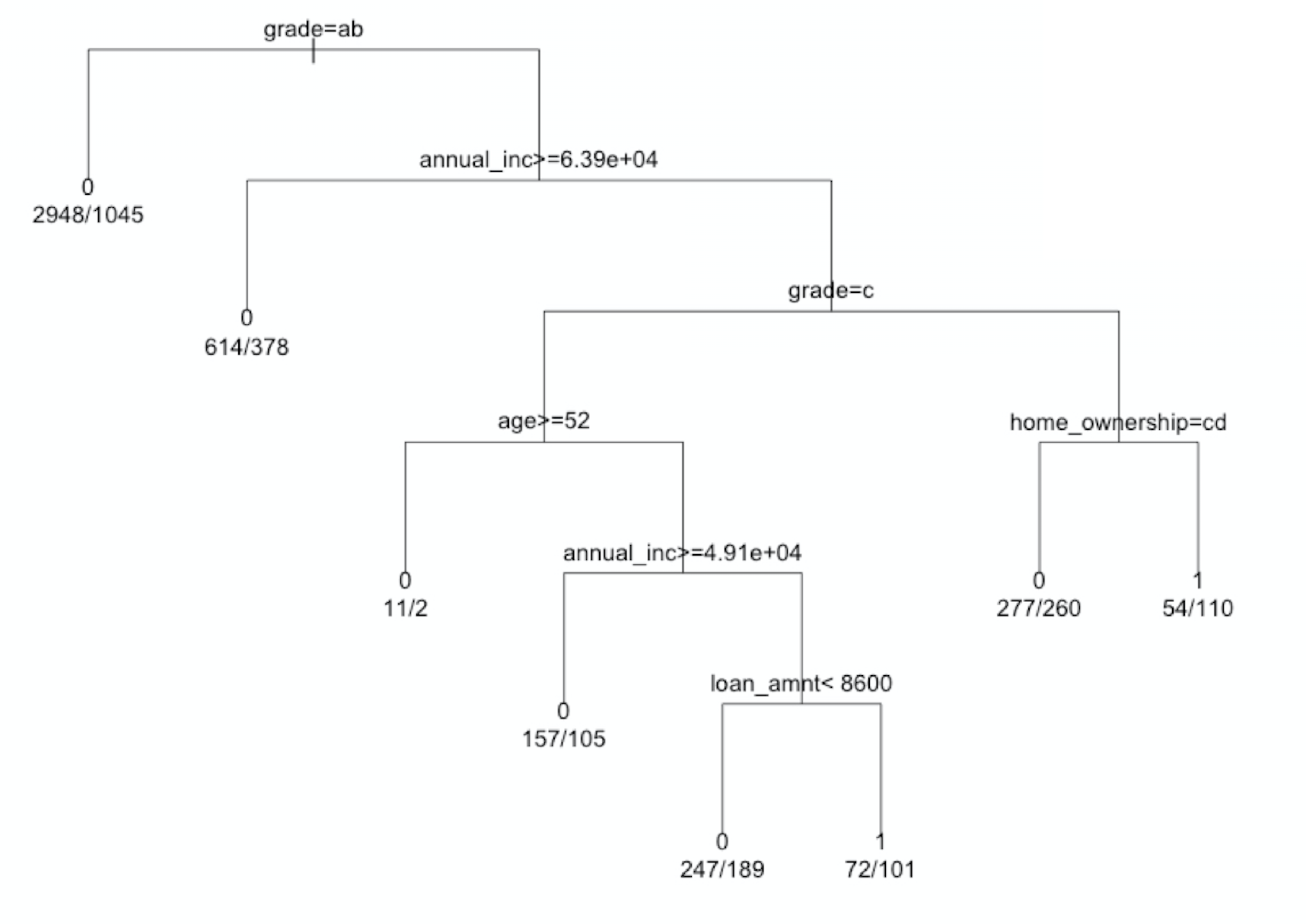

Pruning the decision tree

Credit Risk Modeling in R

Lore Dirick

Manager of Data Science Curriculum at Flatiron School

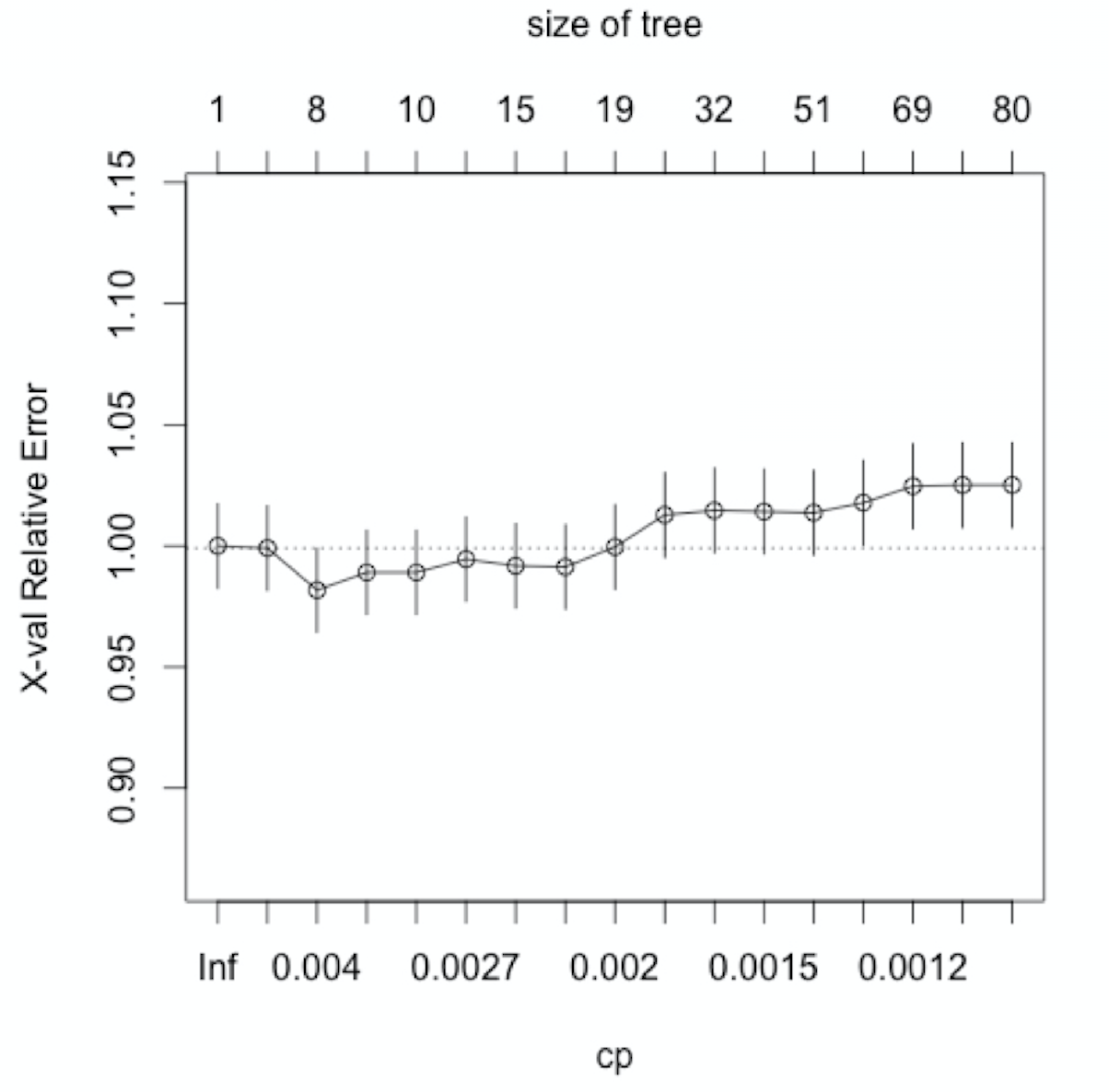

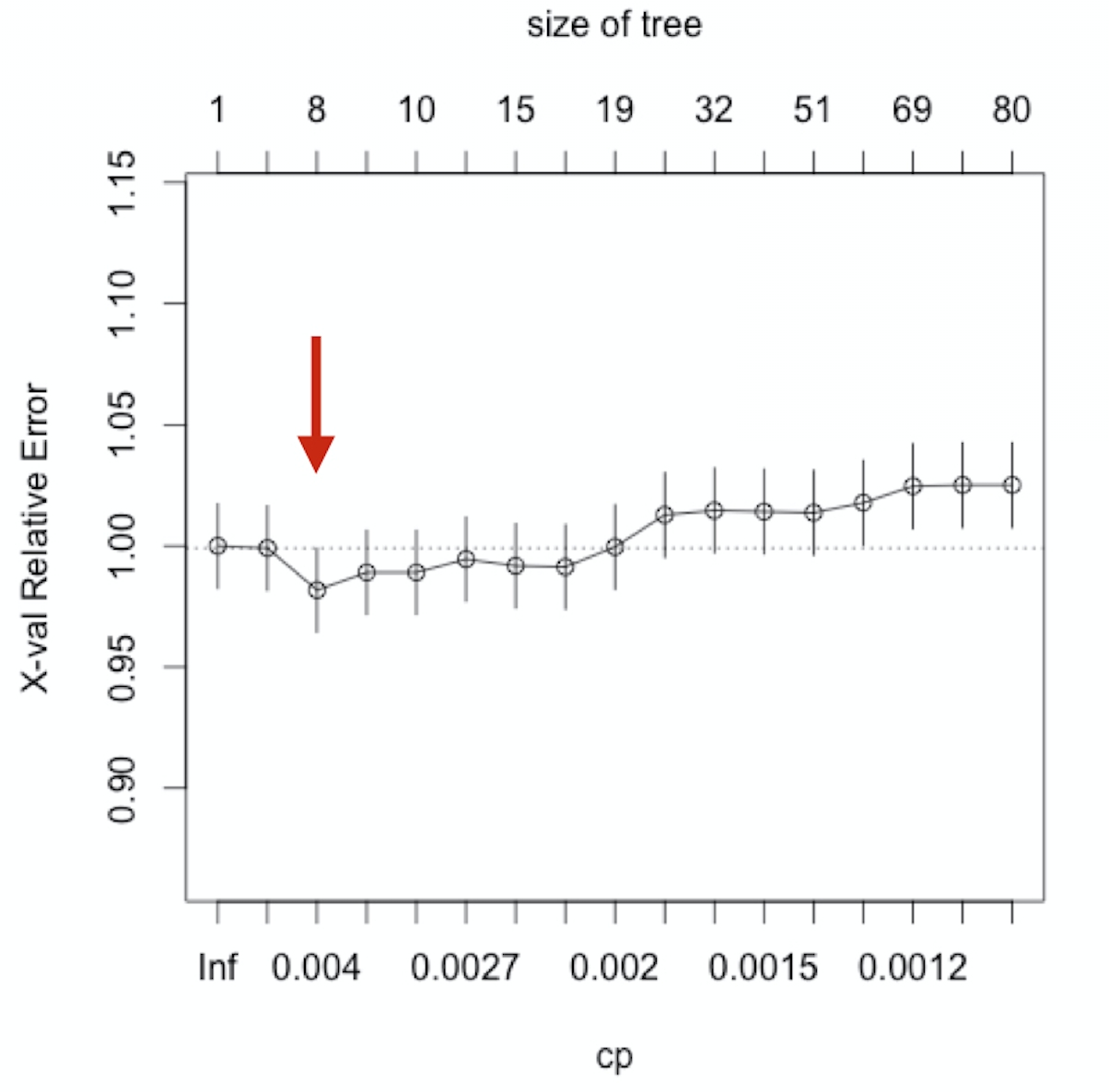

Plotcp and tree_undersample

Plotcp and tree_undersample

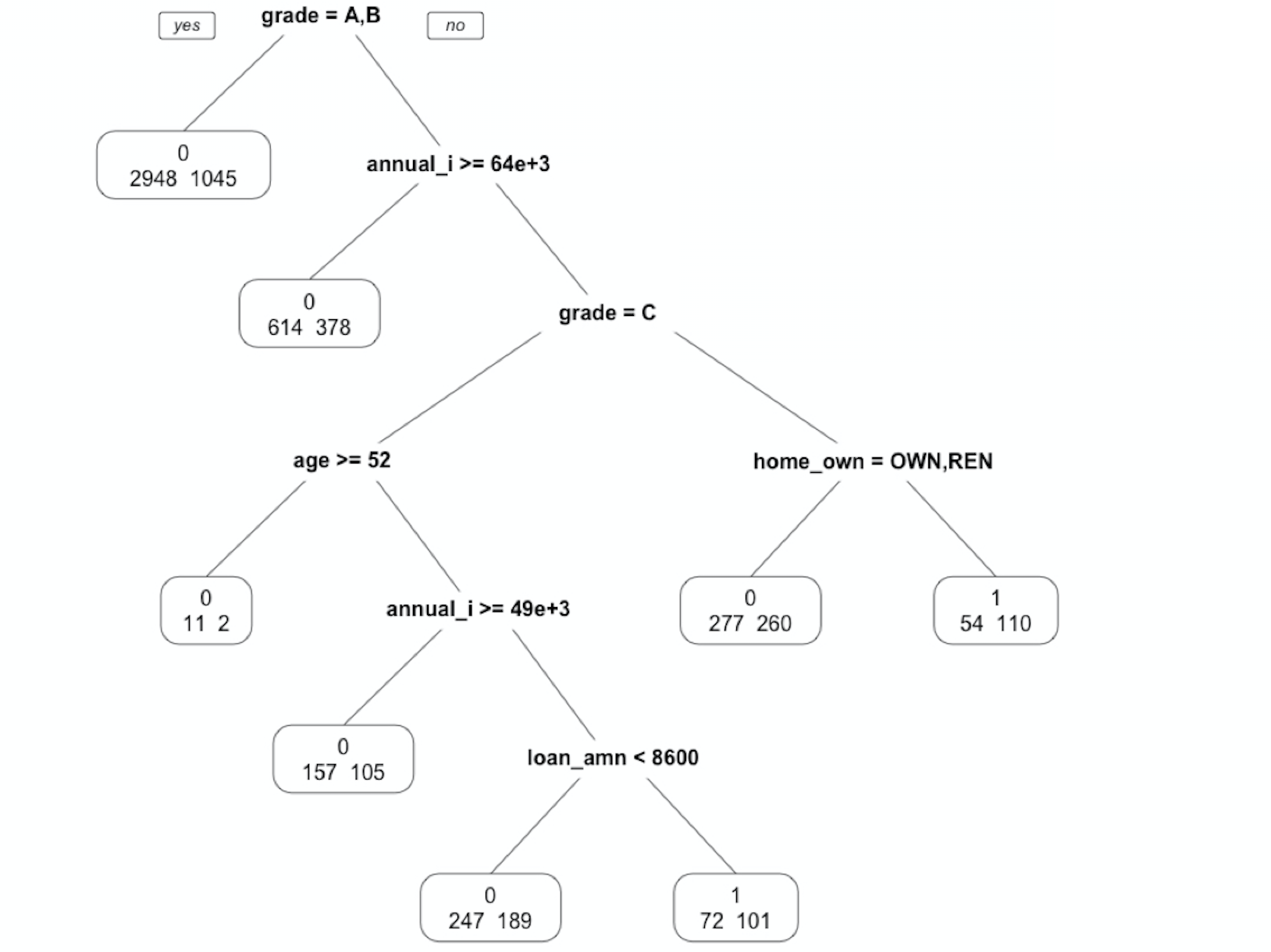

Plot the pruned tree

Plot the pruned tree

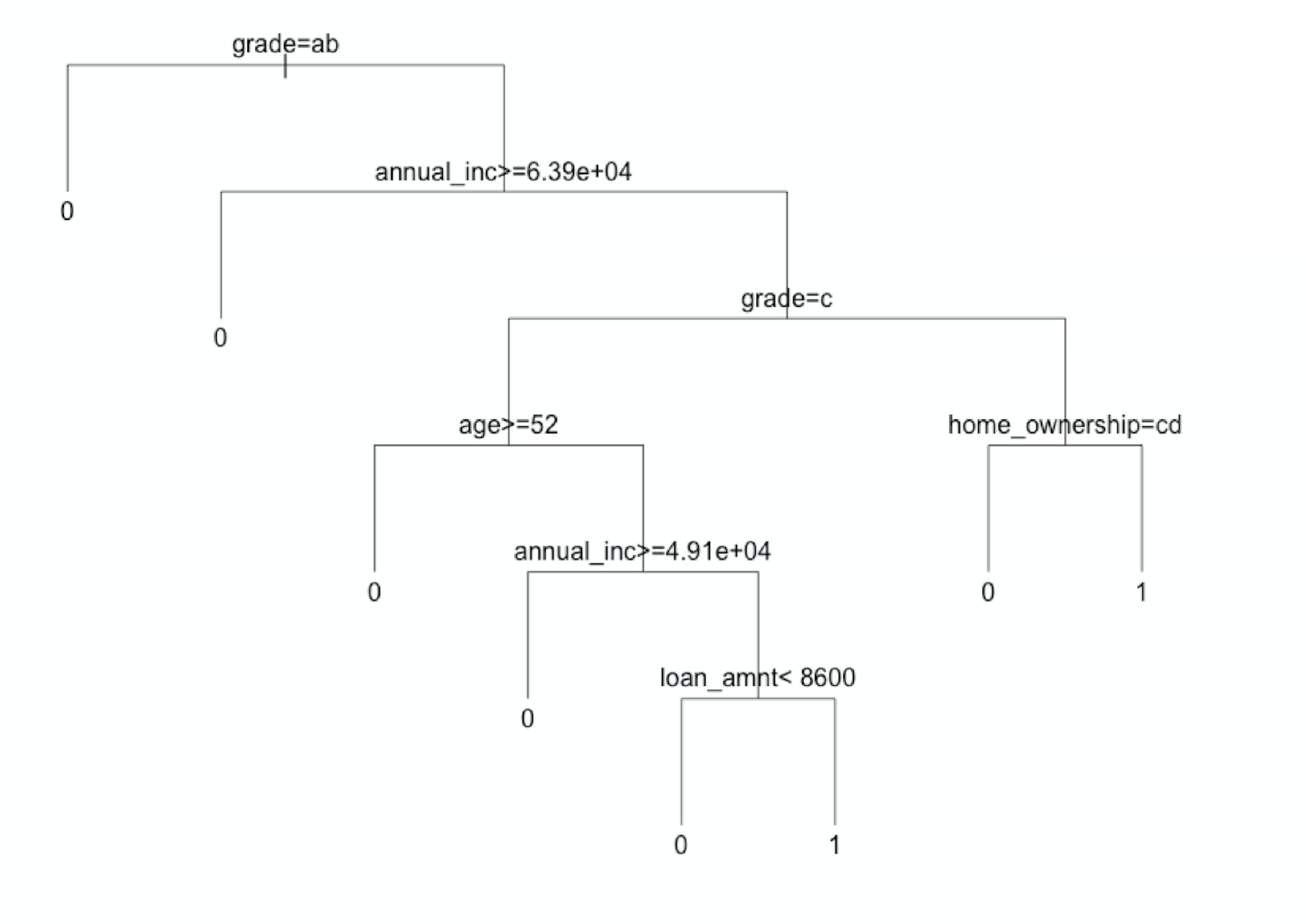

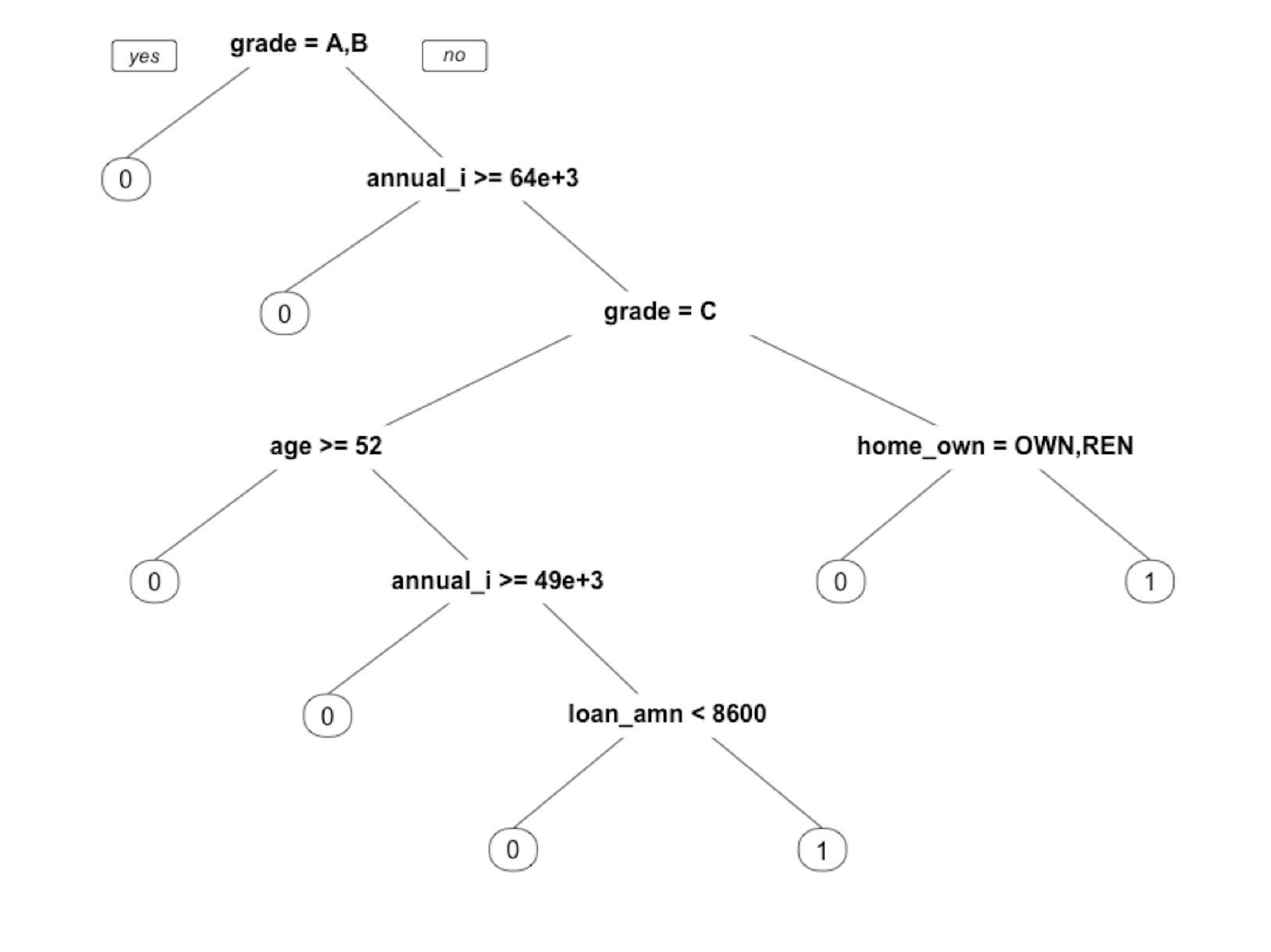

prp() in the rpart.plot-package

prp() in the part.plot-package