Data splitting and confusion matrices

Credit Risk Modeling in R

Lore Dirick

Manager of Data Science Curriculum at Flatiron School

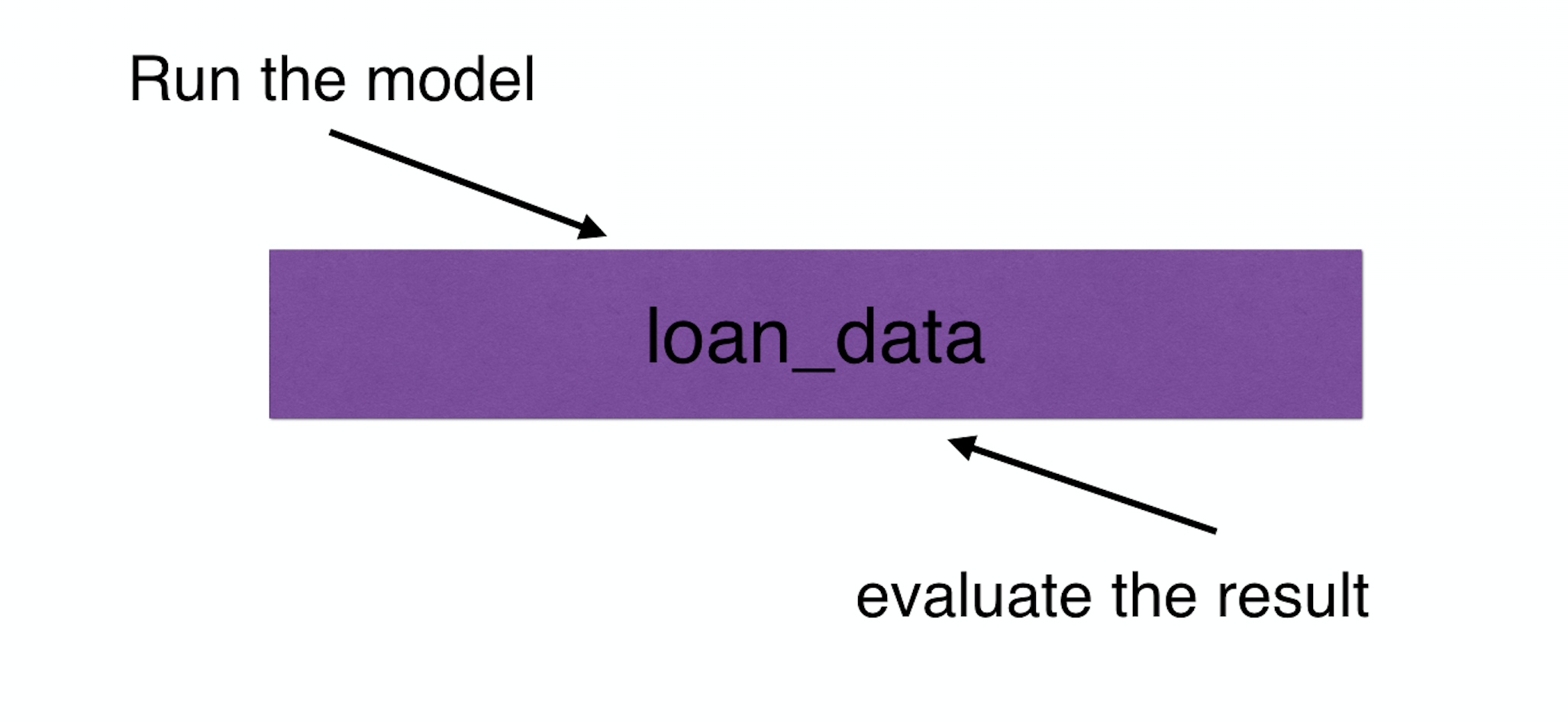

Start analysis

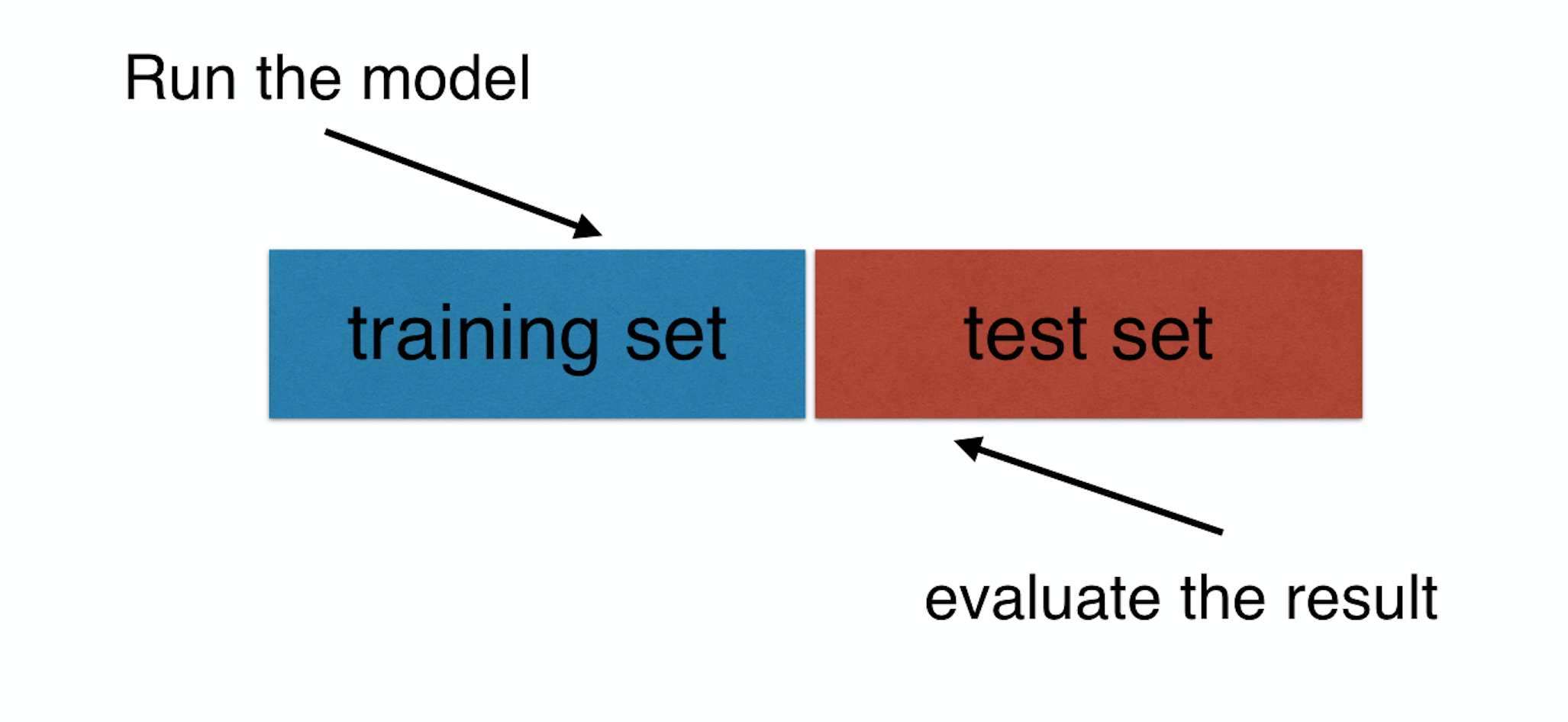

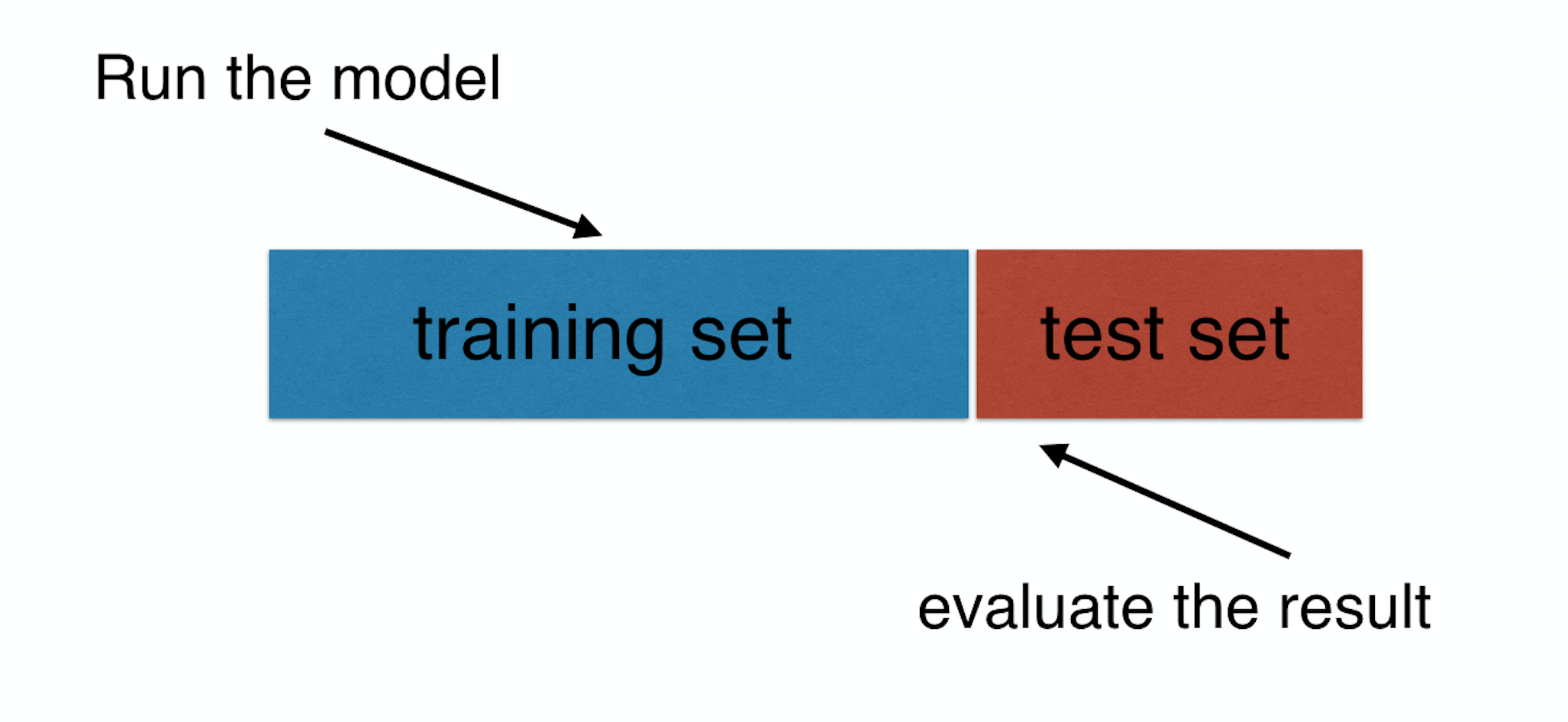

Training and test set

Training and test set

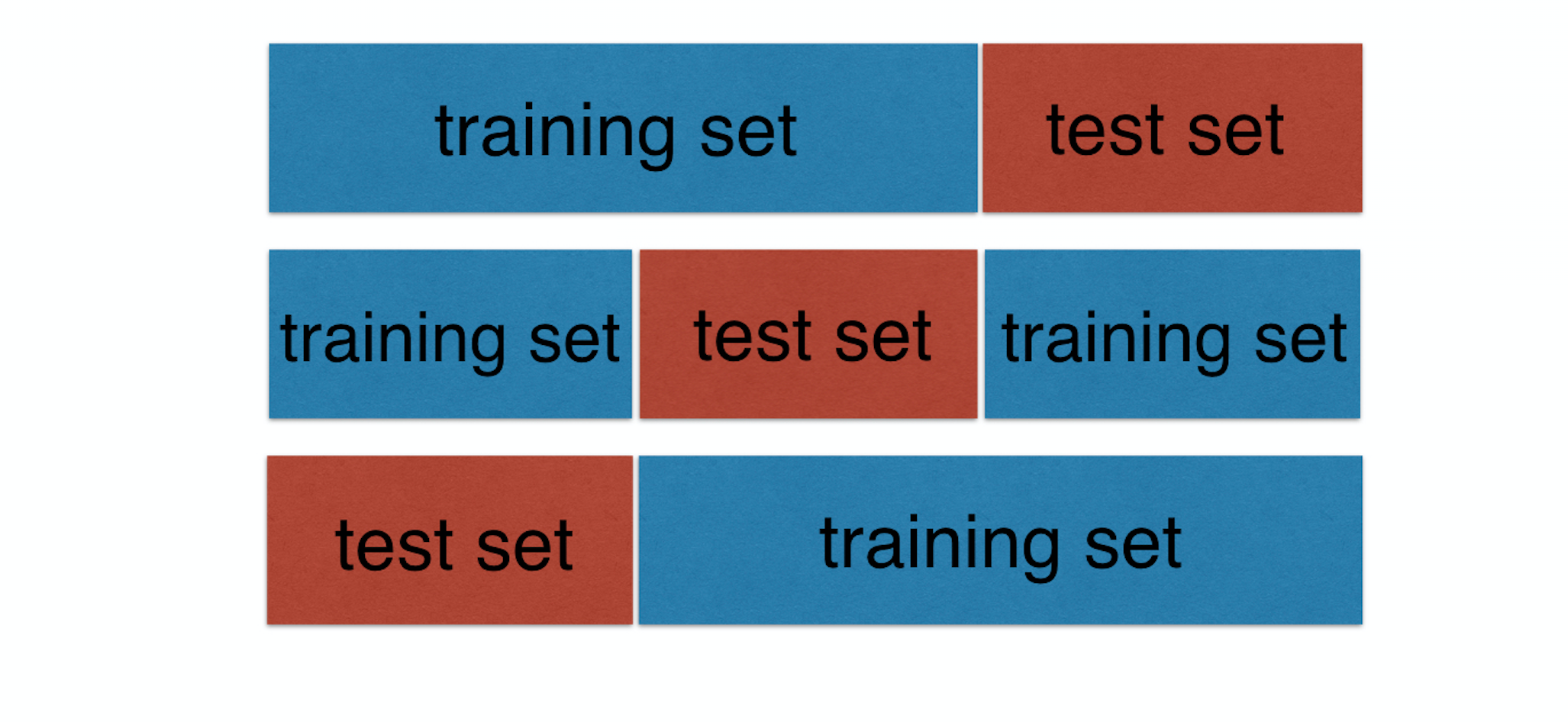

Cross-validation

Credit Risk Modeling in R

Lore Dirick

Manager of Data Science Curriculum at Flatiron School