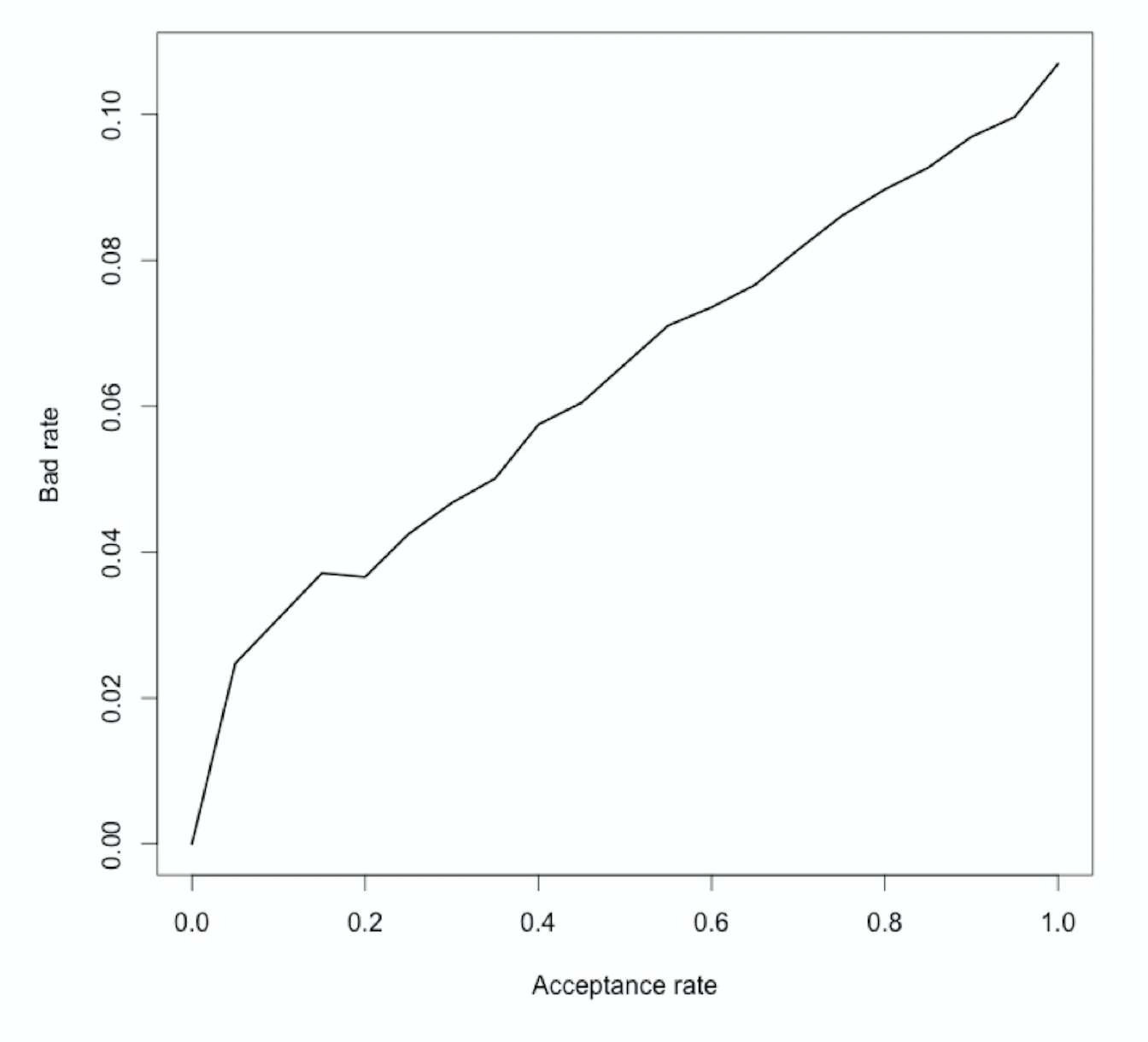

Finding the right cut-off: the strategy curve

Credit Risk Modeling in R

Lore Dirick

Manager of Data Science Curriculum at Flatiron School

The strategy curve

Credit Risk Modeling in R

Lore Dirick

Manager of Data Science Curriculum at Flatiron School