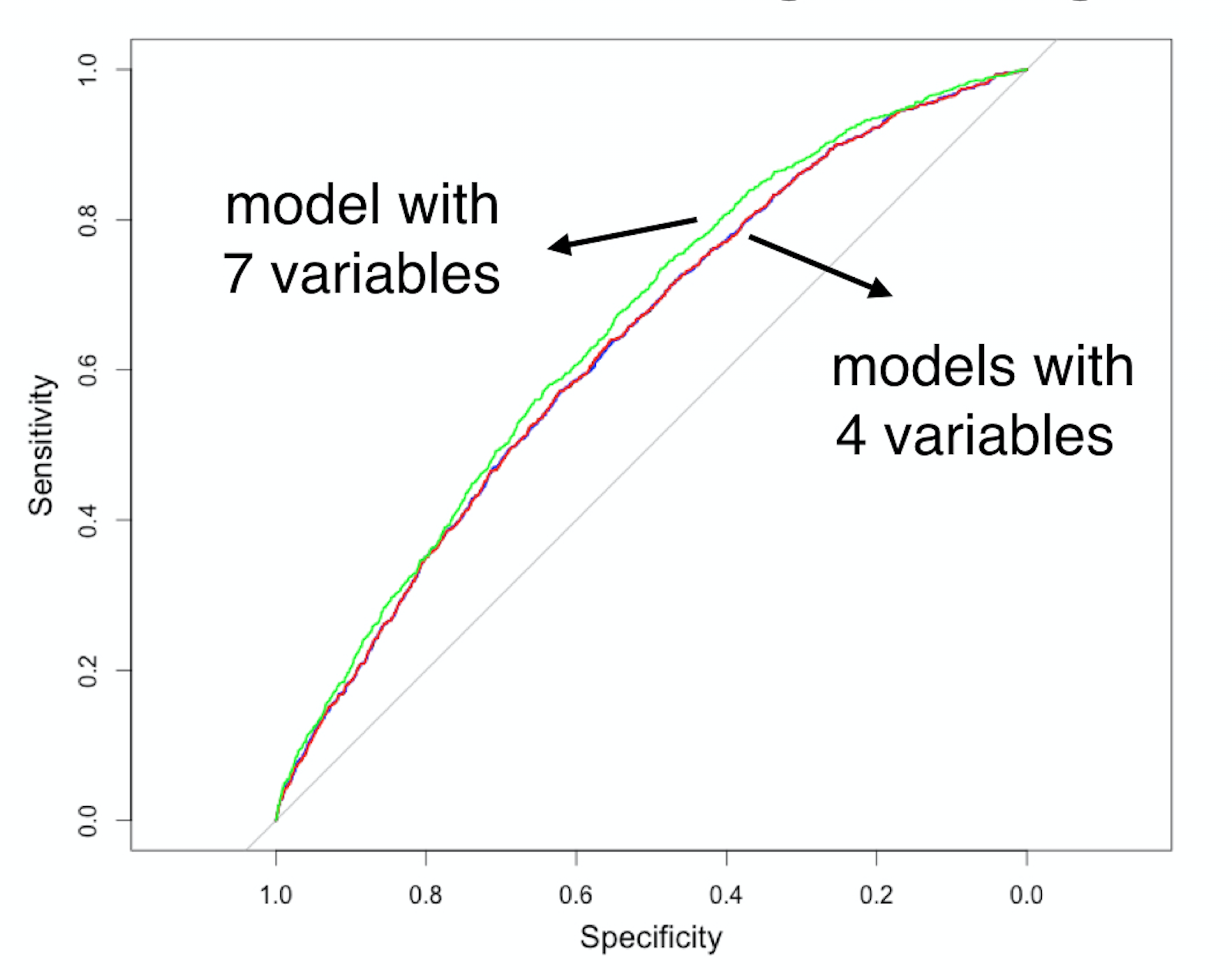

Input selection based on the AUC

Credit Risk Modeling in R

Lore Dirick

Manager of Data Science Curriculum at Flatiron School

ROC curves for 4 logistic regression models

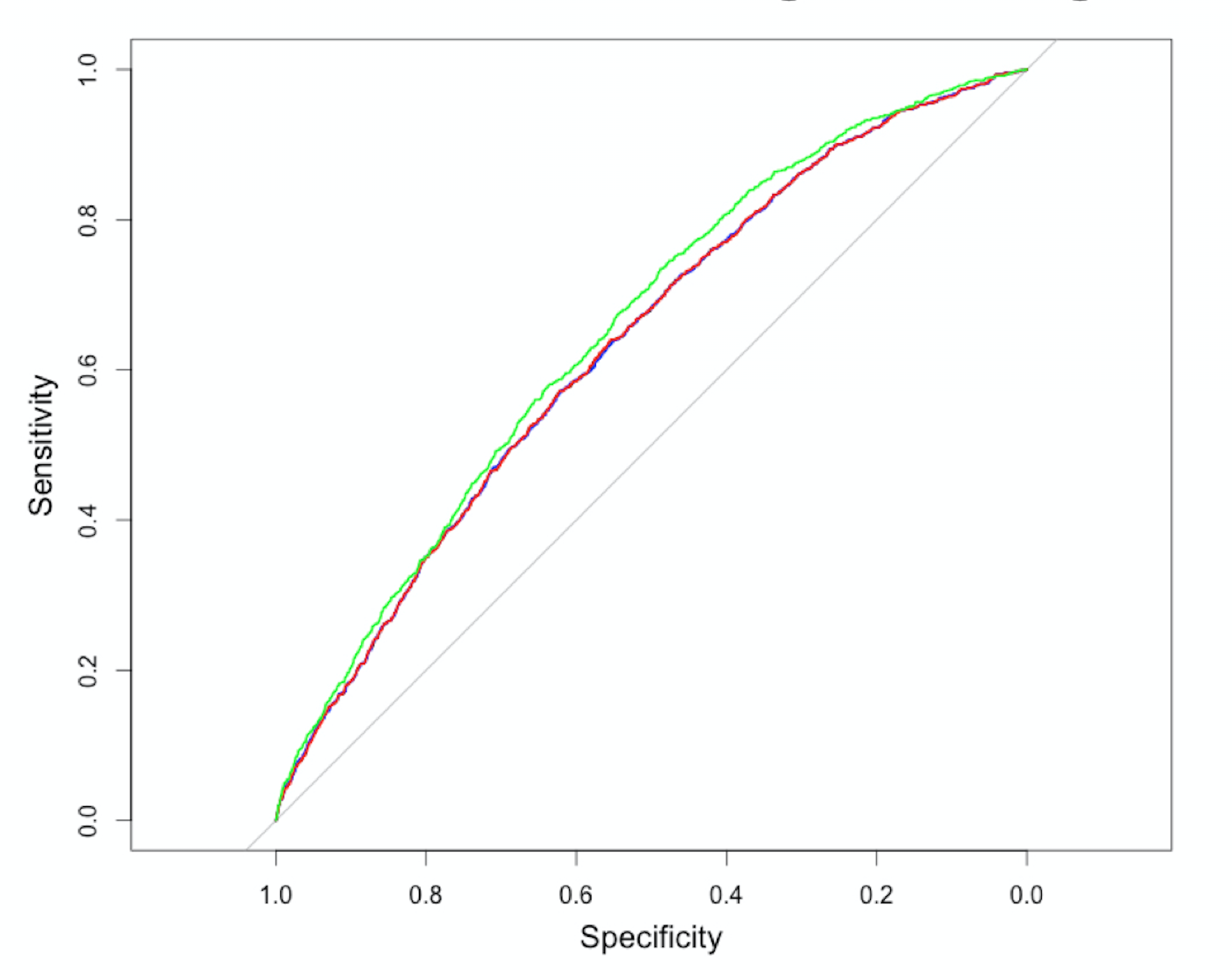

ROC curves for 4 logistic regression models

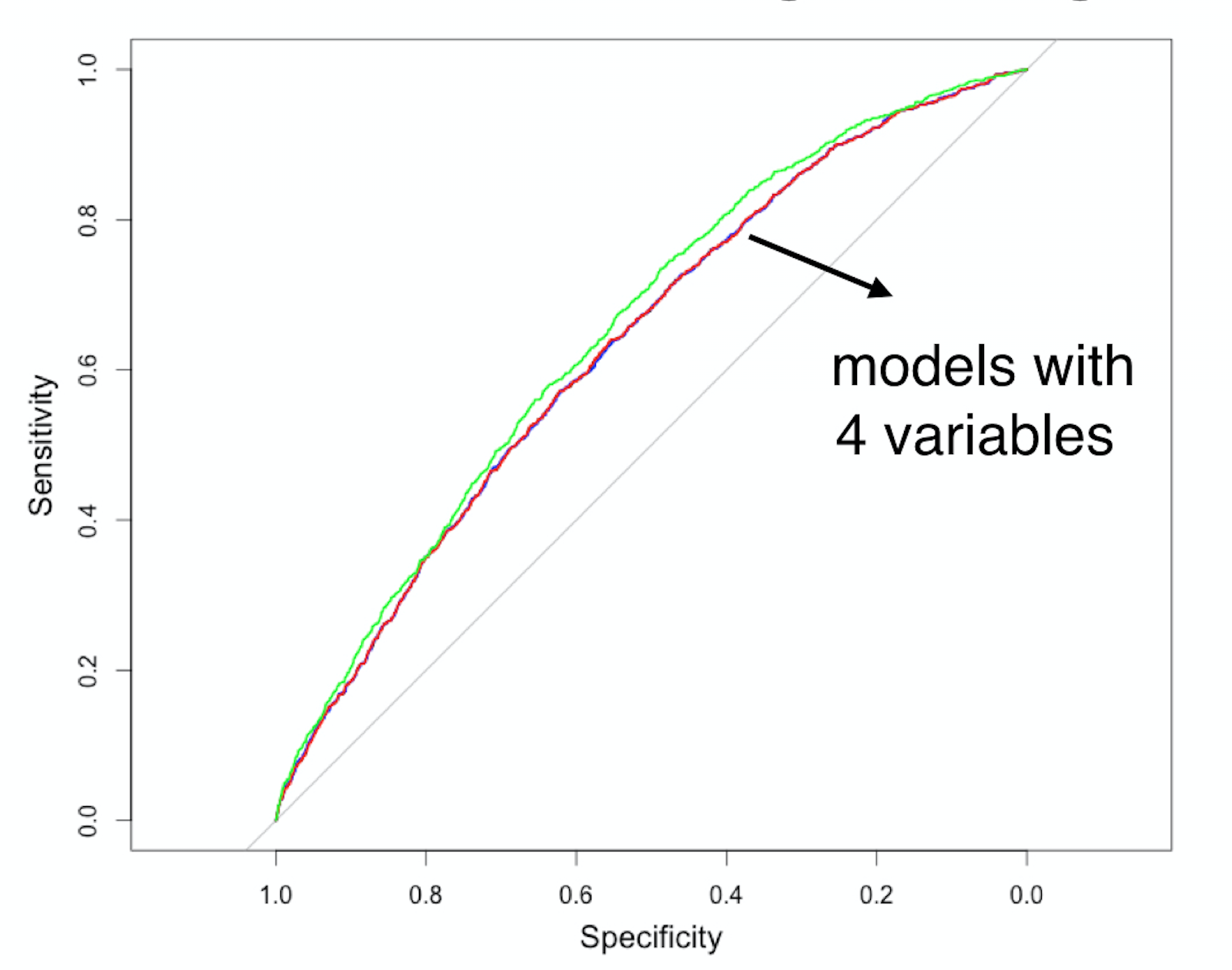

ROC curves for 4 logistic regression models