Time Series Analysis in R

David S. Matteson

Associate Professor at Cornell University

The Autoregressive (AR) recursion:

$Today = Constant + Slope * Yesterday + Noise $

Mean centered version:

$(Today - Mean) = $

$ Slope*(Yesterday - Mean) + Noise $

$$(Today - Mean) = $$

$$Slope * (Yesterday - Mean) + Noise$$

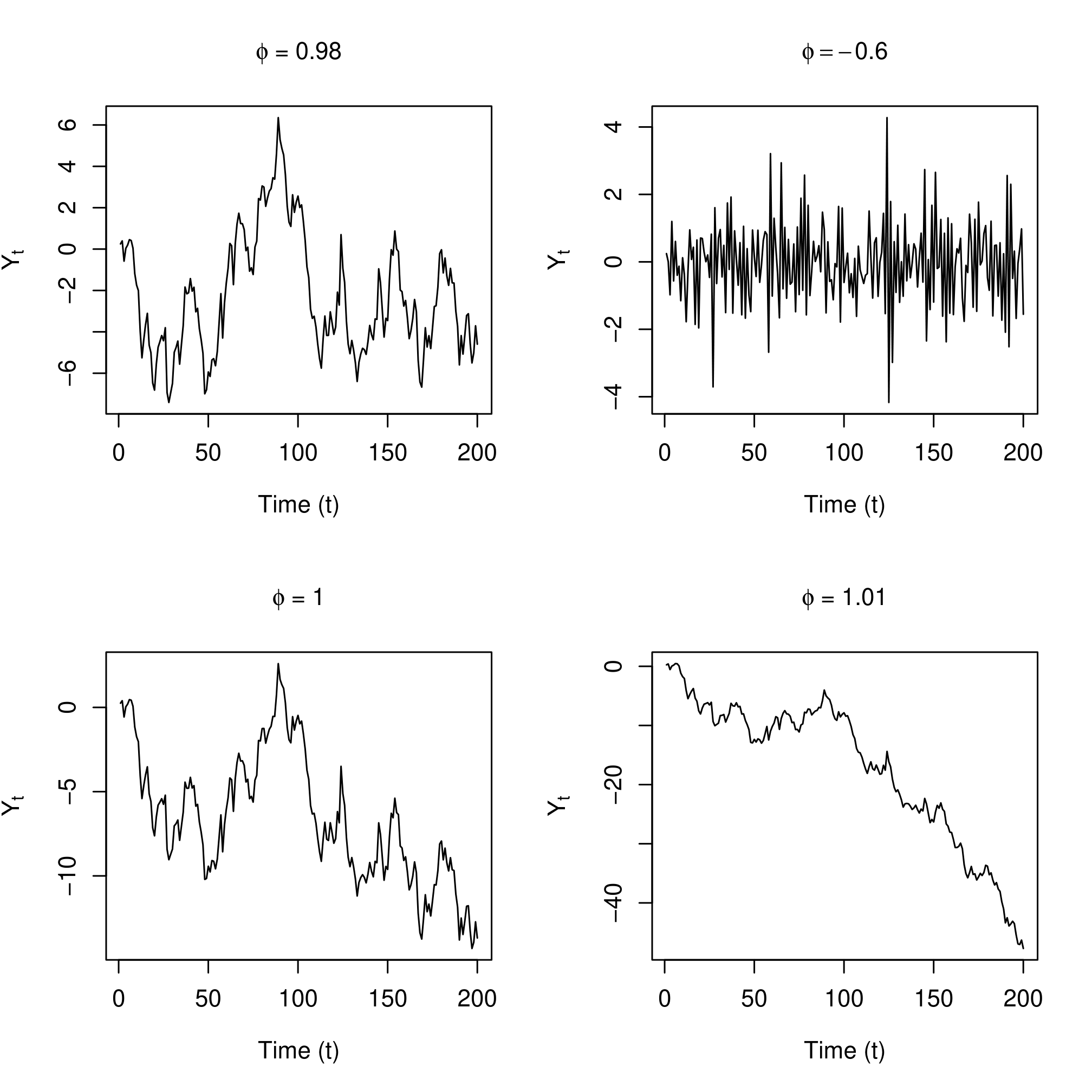

More formally: $$ Y_t - \mu = \phi (Y_{t-1} - \mu ) + \epsilon_t$$ where $ \epsilon_t$ is mean zero white noise (WN).

$$Y_t - \mu = \phi(Y_{t-1} - \mu) + \epsilon_t$$

And $Y_t$ is white noise: $(\mu, \sigma _{\epsilon}^2)$

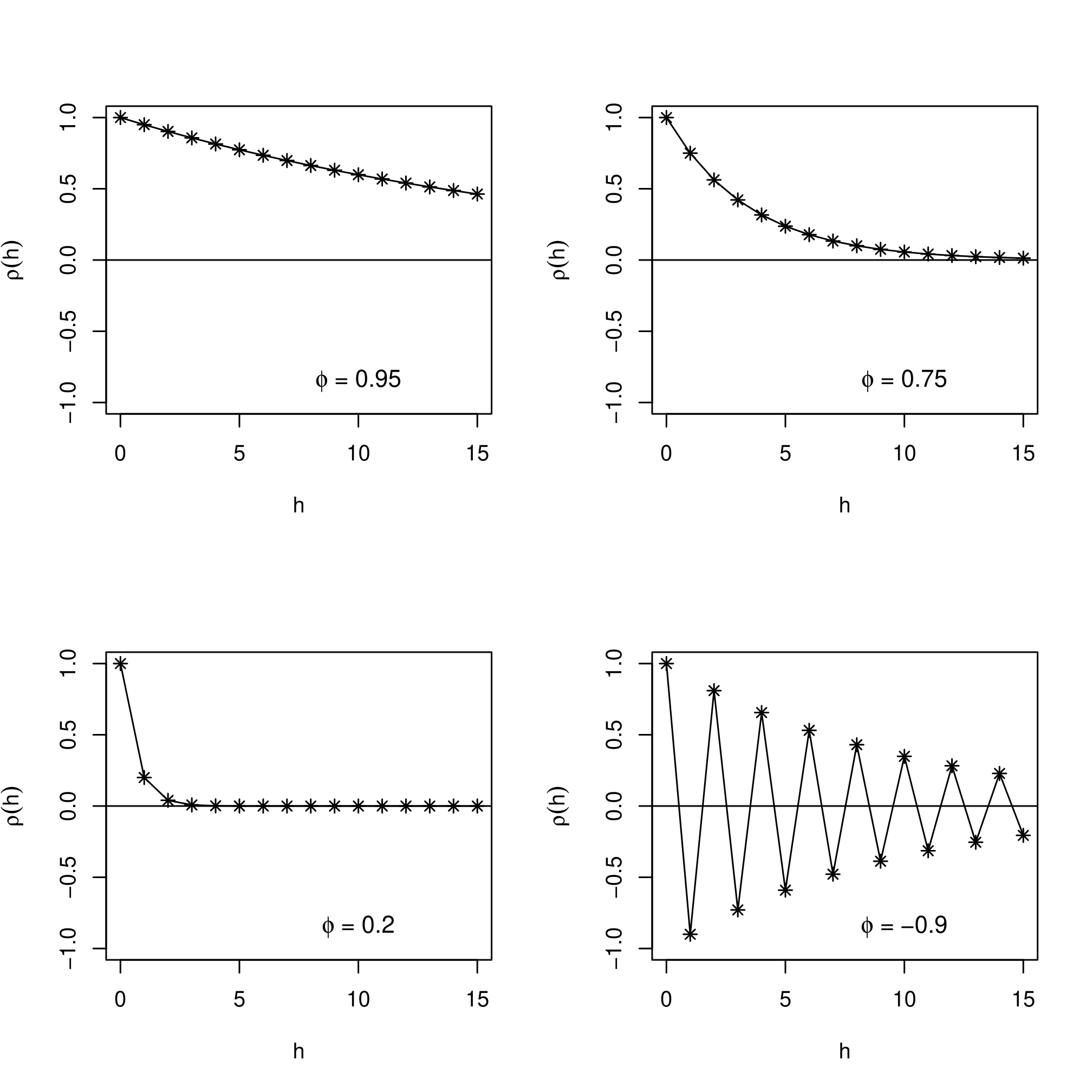

And the process {${Y_t}$} is autocorrelated

Large values of $ \phi$ lead to greater autocorrelation

Negative values of $ \phi$ result in oscillatory time series

If $ \mu = 0$ and slope $ \phi = 1$, then:

$$Y_t = Y_{t-1} + \epsilon_t$$

Which is:

$Today = Yesterday + Noise $

But this is a random walk.

And {$ Y_t $} is not stationary in this case.