Stationary processes

Time Series Analysis in R

David S. Matteson

Associate Professor at Cornell University

Stationarity example

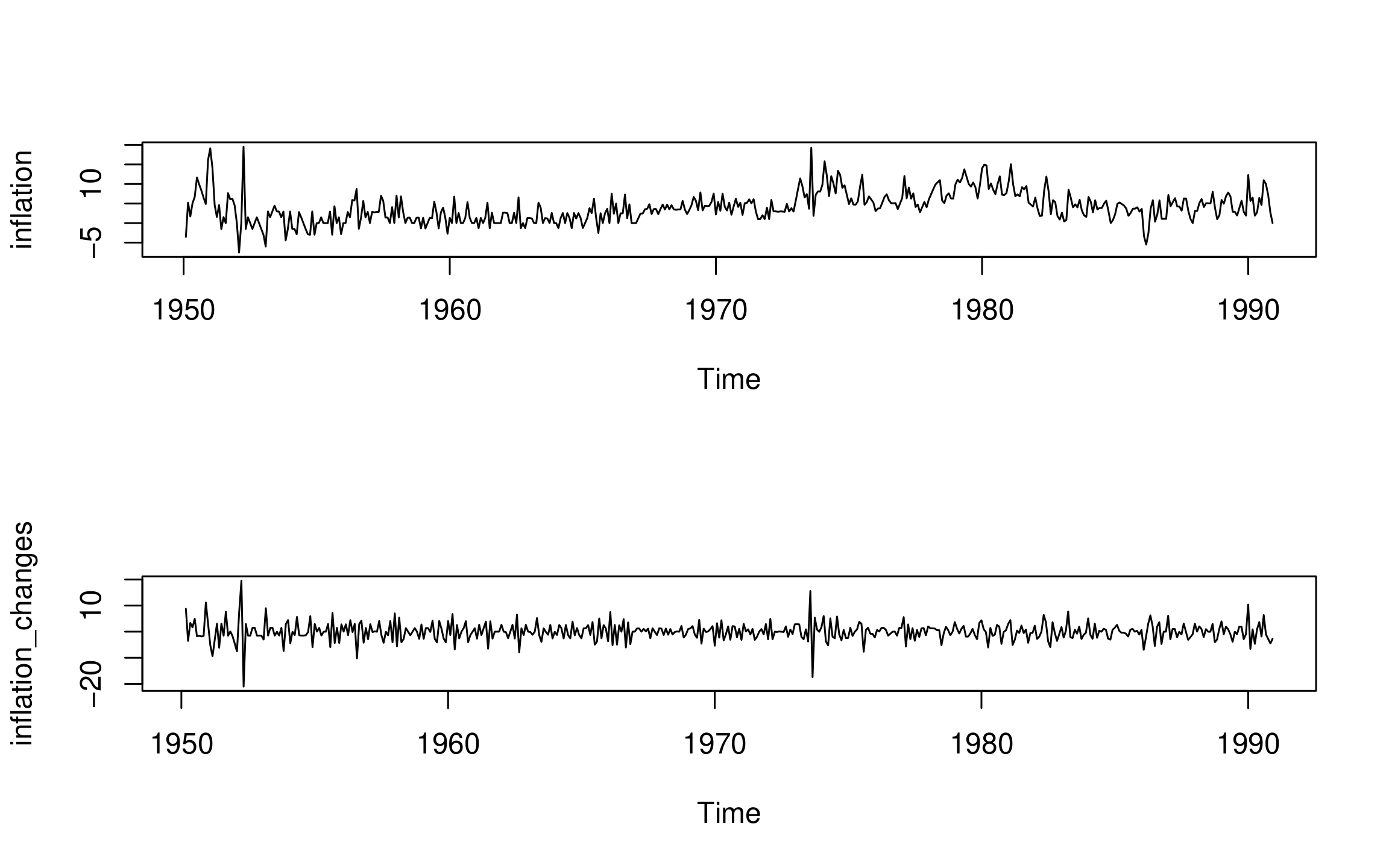

Inflation rates and changes in inflation rates:

Time Series Analysis in R

David S. Matteson

Associate Professor at Cornell University

Inflation rates and changes in inflation rates: