MA model estimation and forecasting

Time Series Analysis in R

David S. Matteson

Associate Professor at Cornell University

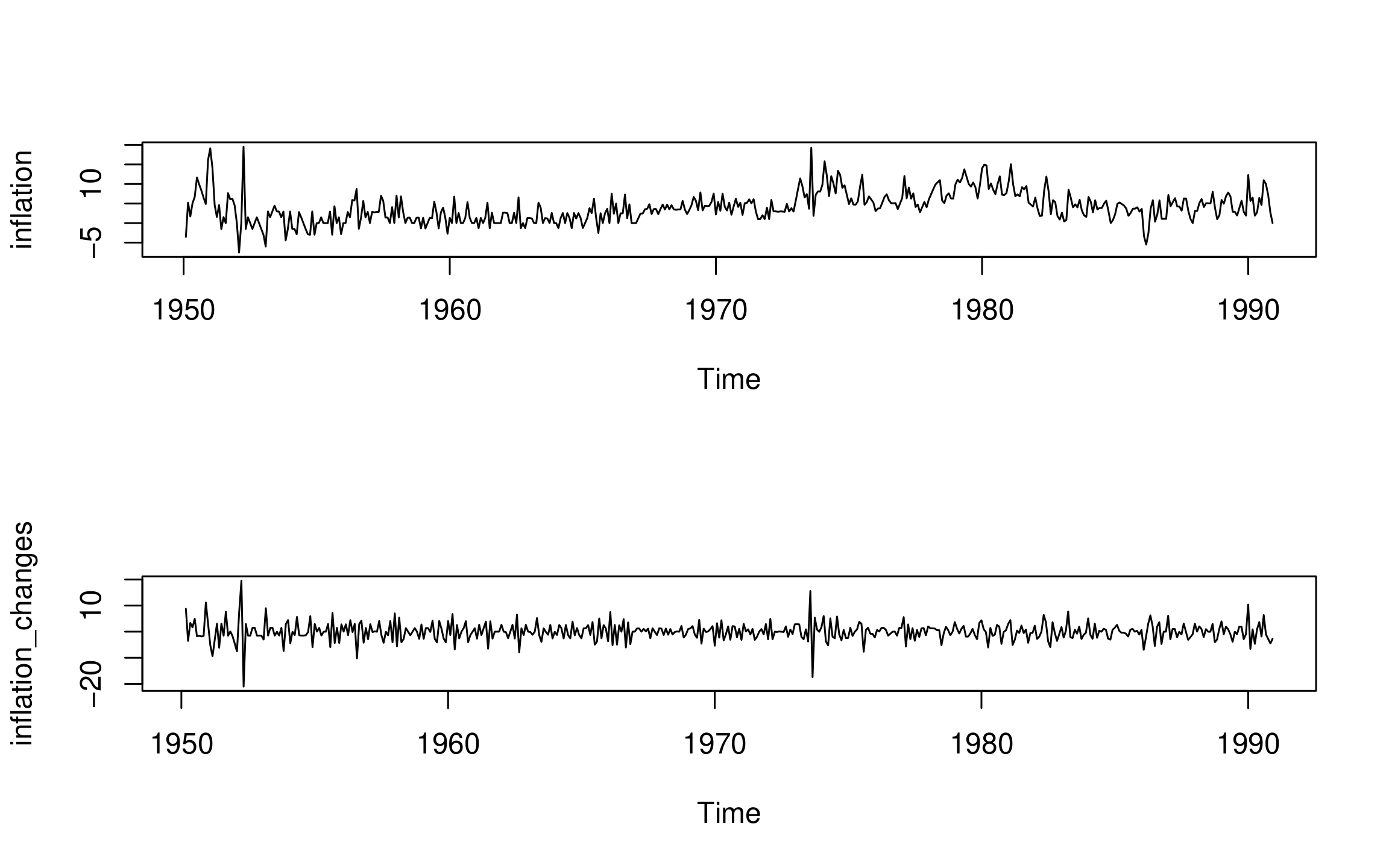

- One-month US inflation rate (in percent, annual rate)

- Monthly observations from 1950 through 1990

data(Mishkin, package = "Ecdat") inflation <- as.ts(Mishkin[, 1])inflation_changes <- diff(inflation)ts.plot(inflation) ; ts.plot(inflation_changes)

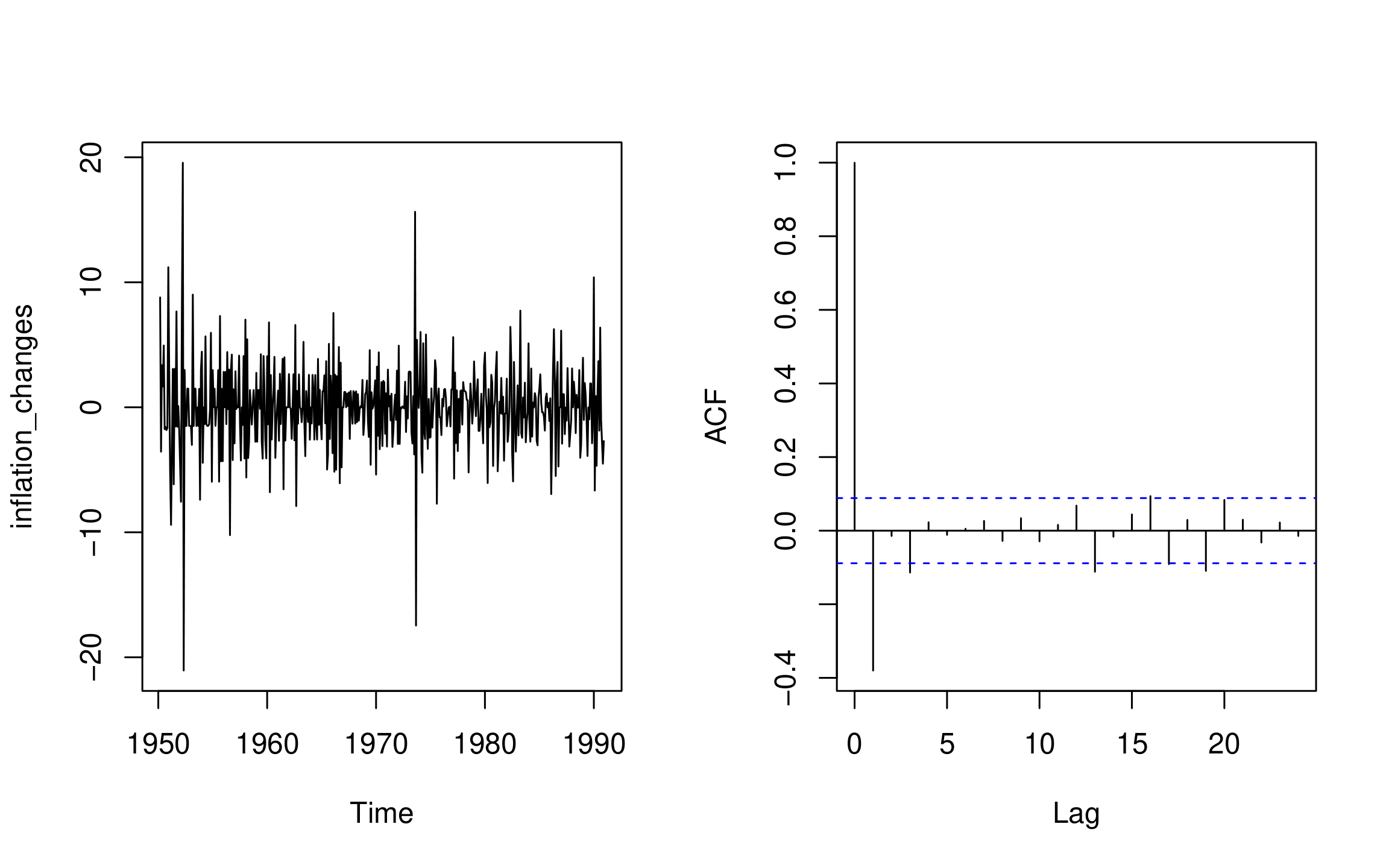

MA processes: changes in inflation tate - II

Inflation_changes: changes in one-month US inflation rate- Plot the series and its sample ACF:

ts.plot(inflation_changes)

acf(inflation_changes, lag.max = 24)

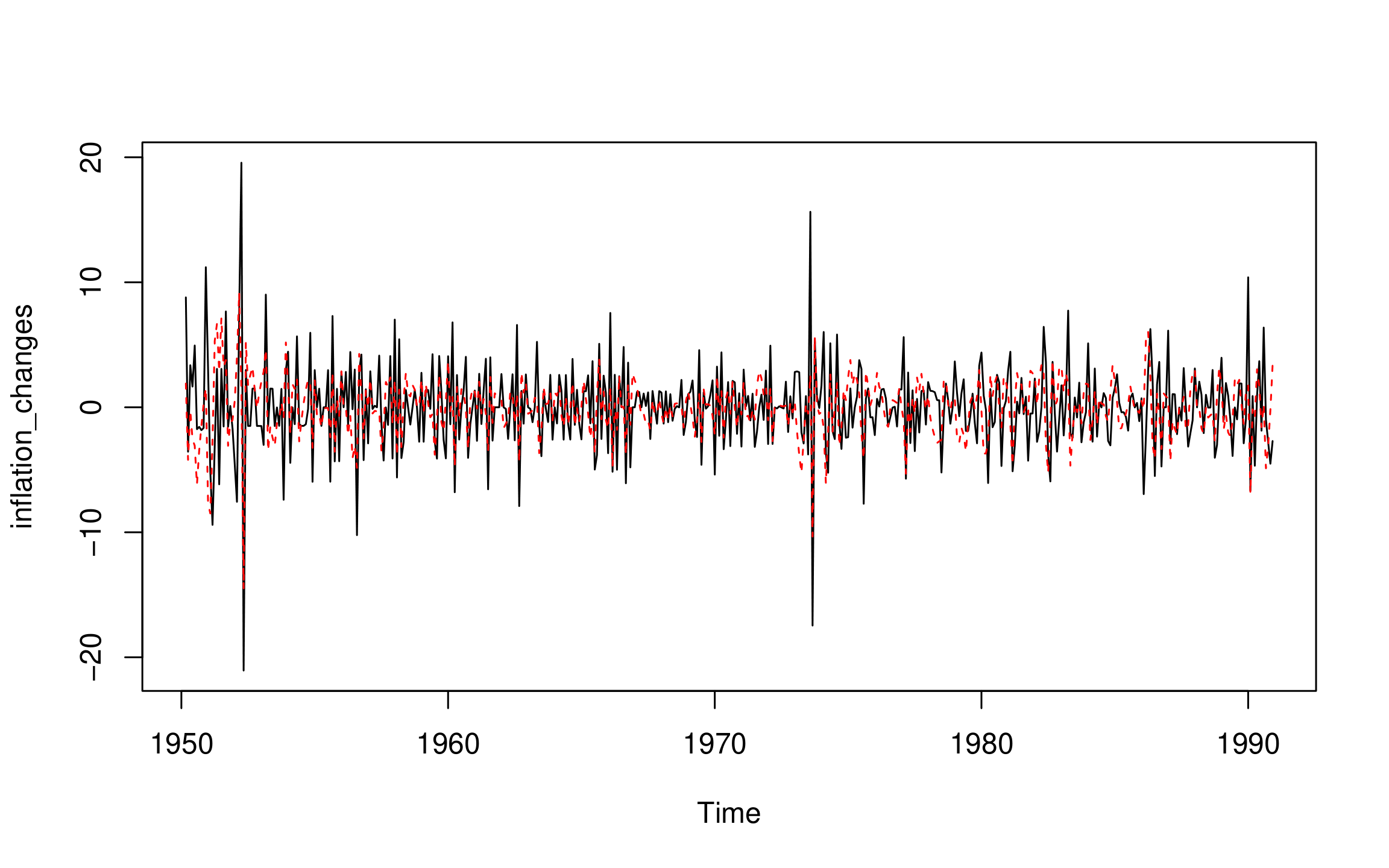

MA processes: fitted values - I

- MA fitted values:

$$\hat{Y_t} = \hat{\mu} +\hat{\theta}\hat{\epsilon_{t-1}}$$

$$\hat{Y_t} = \hat{\mu} +\hat{\theta}\hat{\epsilon_{t-1}}$$

- Residuals =

$$\hat{\epsilon_t} = Y_t - \hat{Y_t}$$

$$\hat{\epsilon_t} = Y_t - \hat{Y_t}$$

ts.plot(inflation_changes) MA_inflation_changes_fitted <- inflation_changes - residuals(MA_inflation_changes)points(MA_inflation_changes_fitted, type = "l", col = "red", lty = 2)