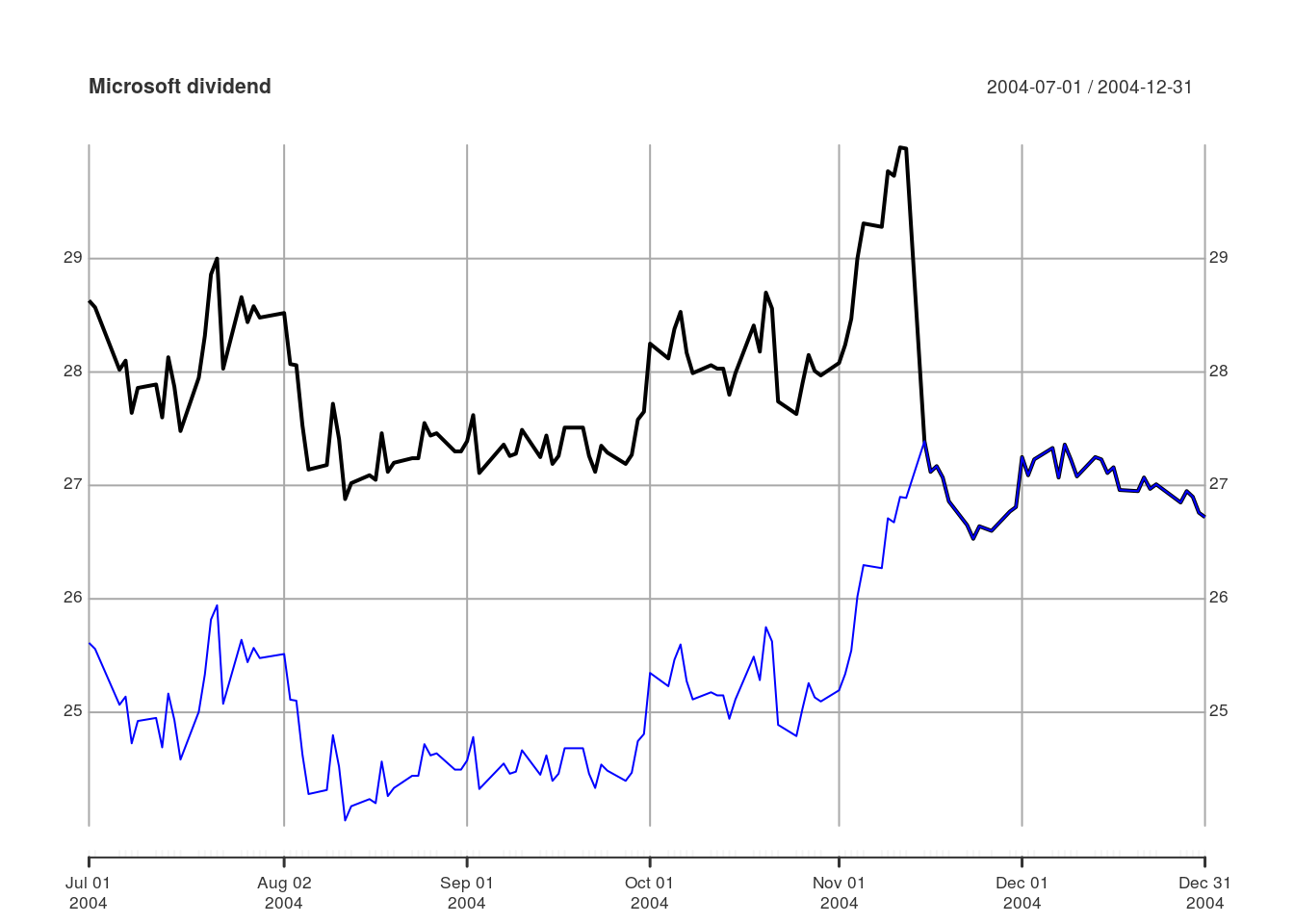

Adjusting for corporate actions

Importing and Managing Financial Data in R

Joshua Ulrich

Quantitative Analyst & quantmod Co-Author and Maintainer

Adjust for stock splits and dividends (2)

Importing and Managing Financial Data in R

Joshua Ulrich

Quantitative Analyst & quantmod Co-Author and Maintainer