Normal probabilities

Foundations of Probability in Python

Alexander A. Ramírez M.

CEO @ Synergy Vision

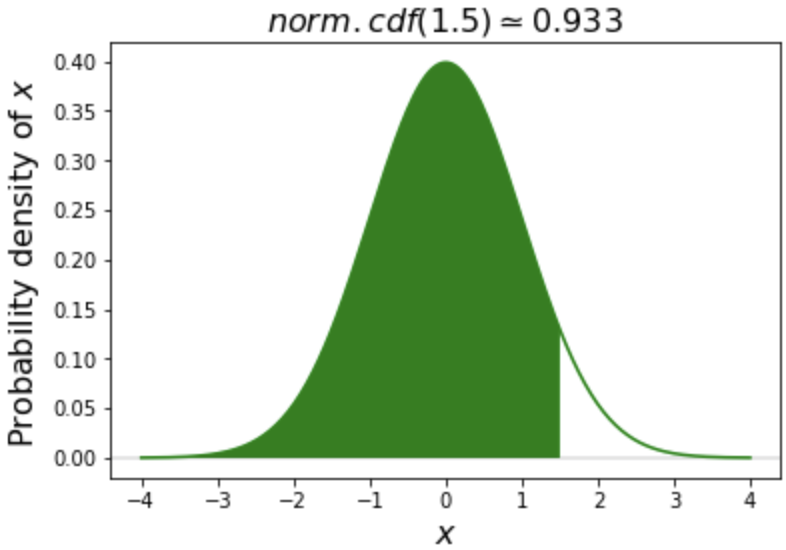

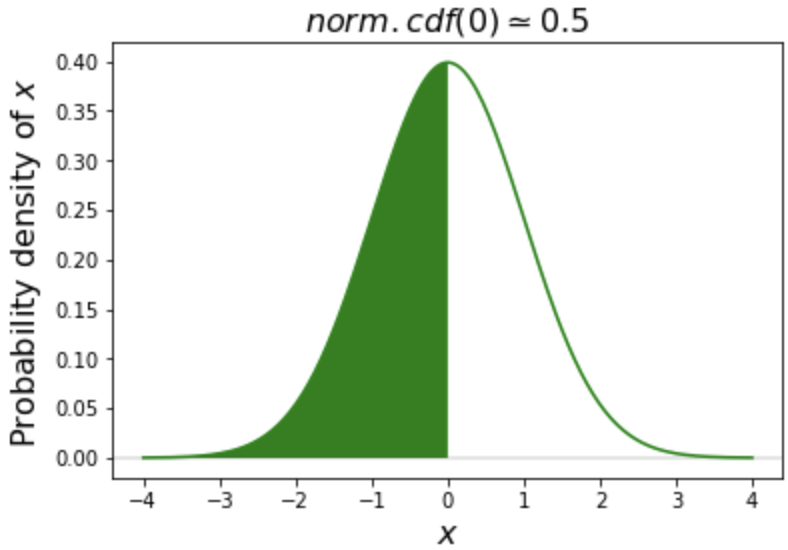

Probability density

$$ $$

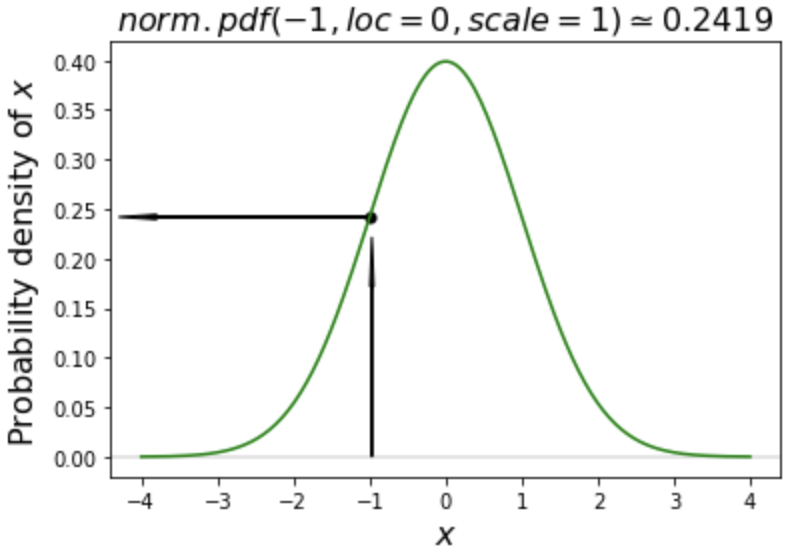

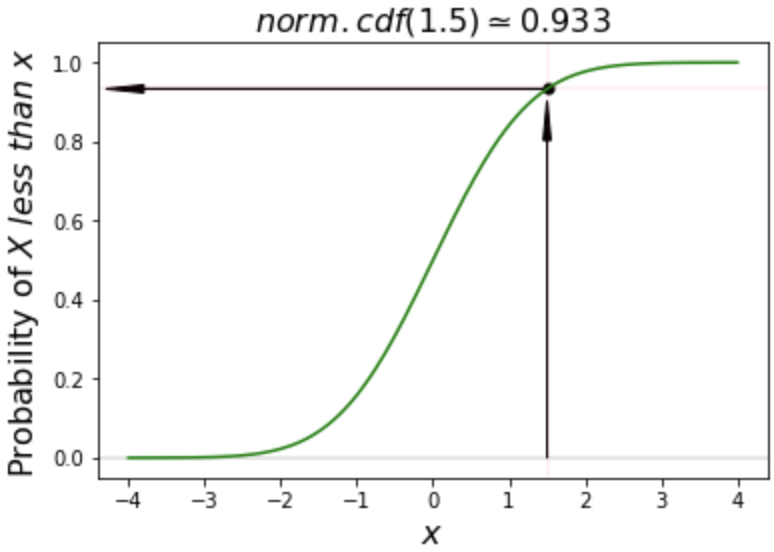

pdf() vs. cdf()

$$ $$

$$ $$

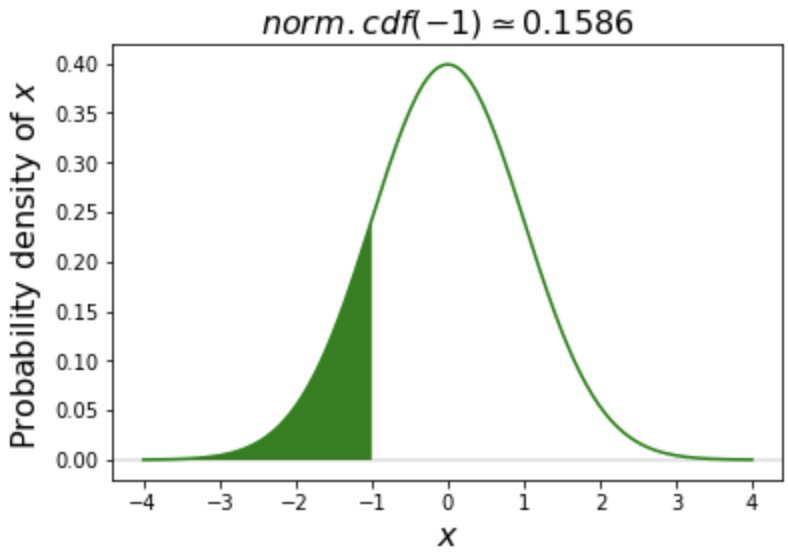

pdf() vs. cdf() (Cont.)

$$ $$

$$ $$

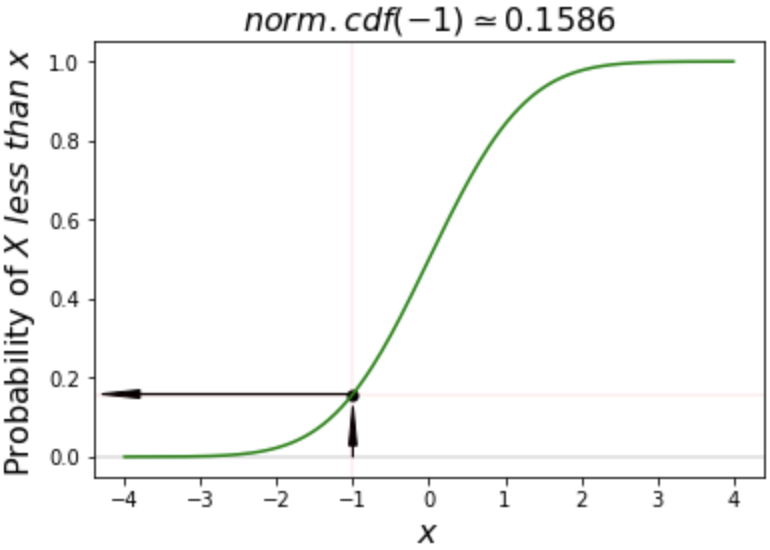

pdf() vs. cdf() (Cont.)

$$ $$

$$ $$

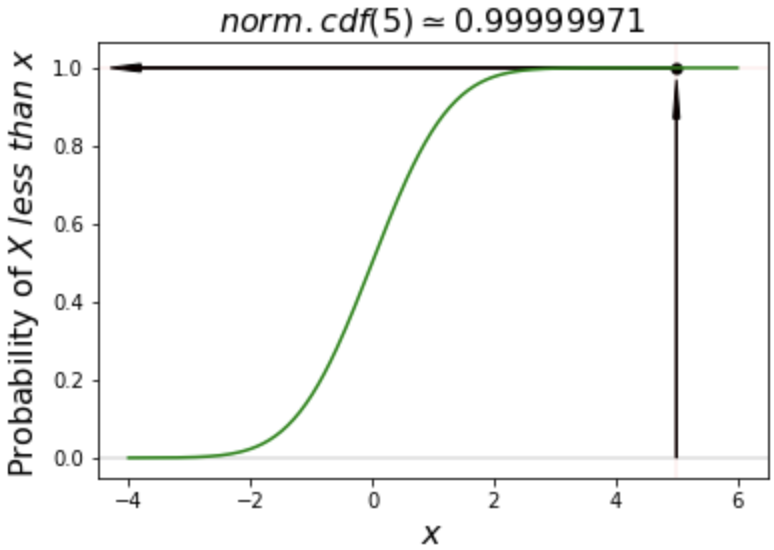

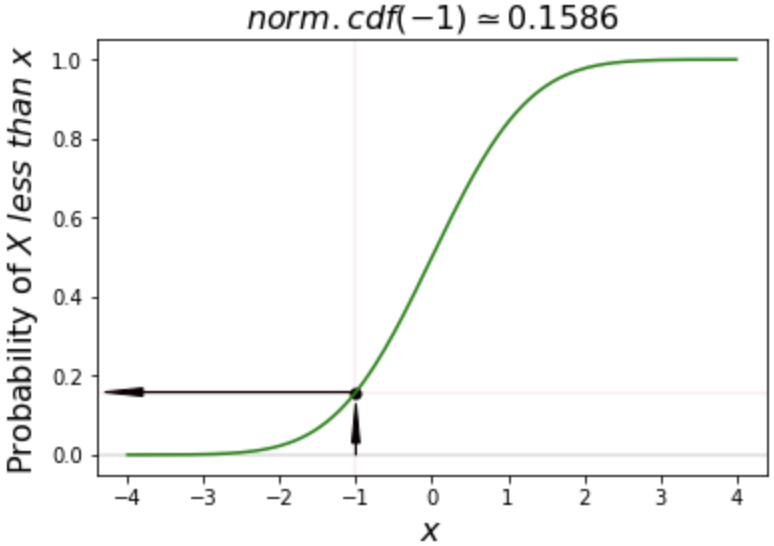

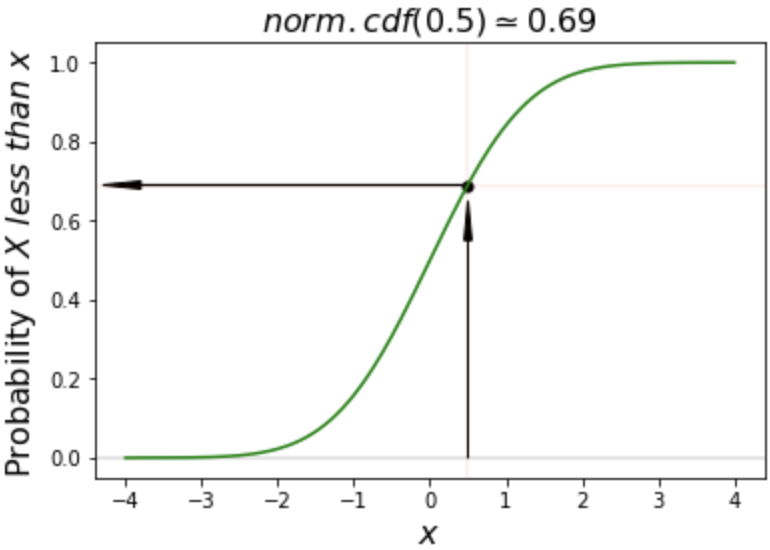

Cumulative distribution function examples

# Calculate cdf of -1

norm.cdf(-1)

0.15865525393145707

# Calculate cdf of 0.5

norm.cdf(0.5)

0.6914624612740131

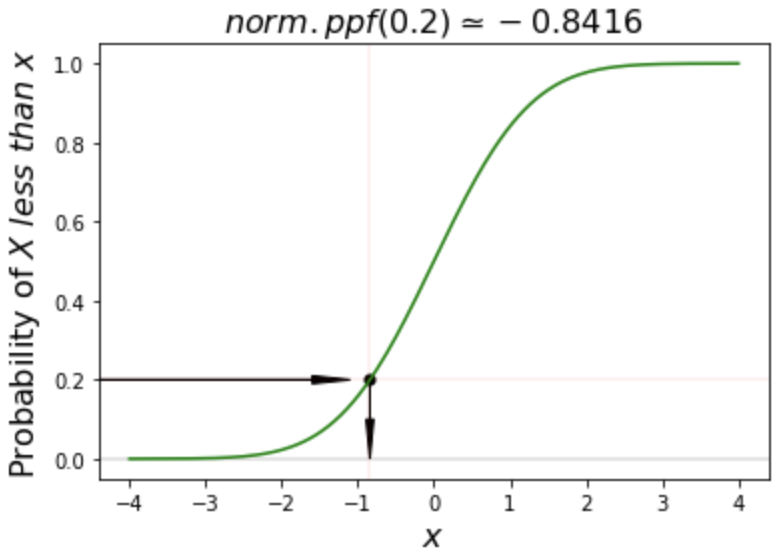

The percent point function (ppf)

# Calculate ppf of 0.2

norm.ppf(0.2)

-0.8416212335729142

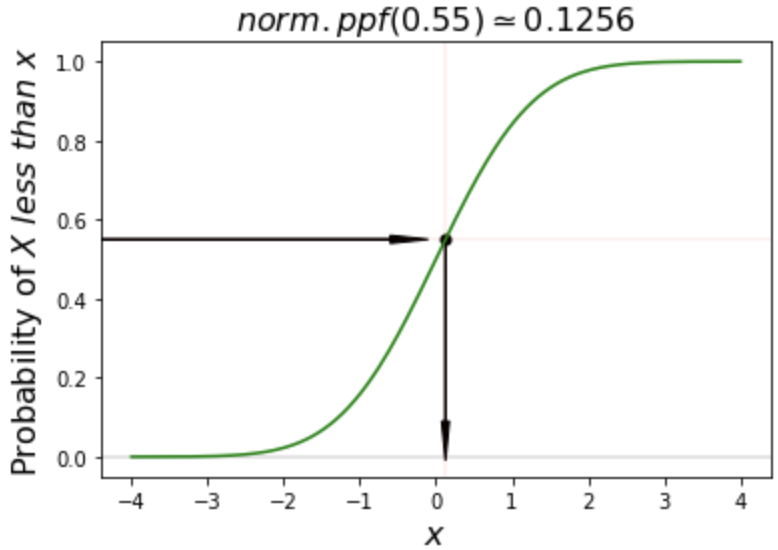

# Calculate ppf of 55%

norm.ppf(0.55)

0.12566134685507416

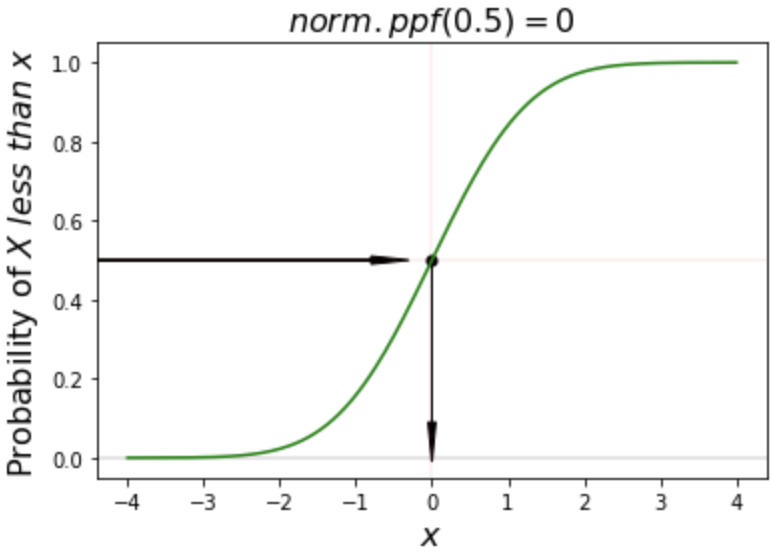

ppf() is the inverse of cdf()

# Calculate cdf of value 0

norm.cdf(0)

0.5

# Calculate ppf of probability 50%

norm.ppf(0.5)

0

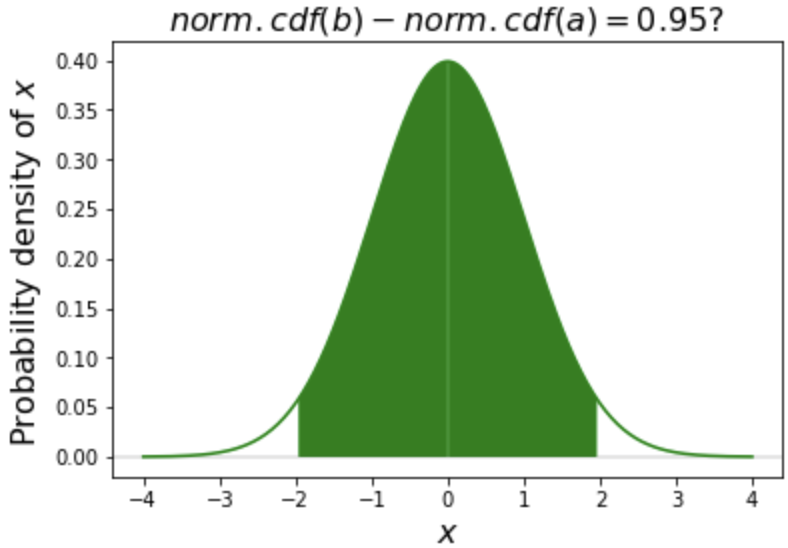

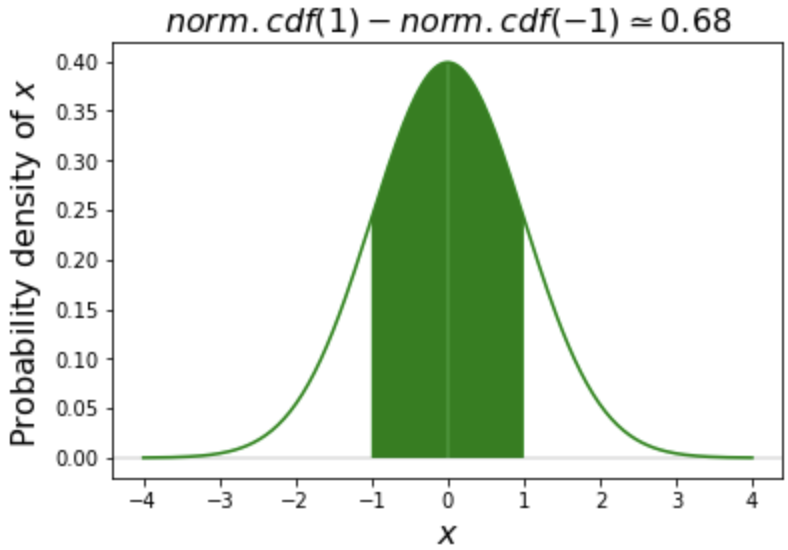

Probability between two values

$$ $$

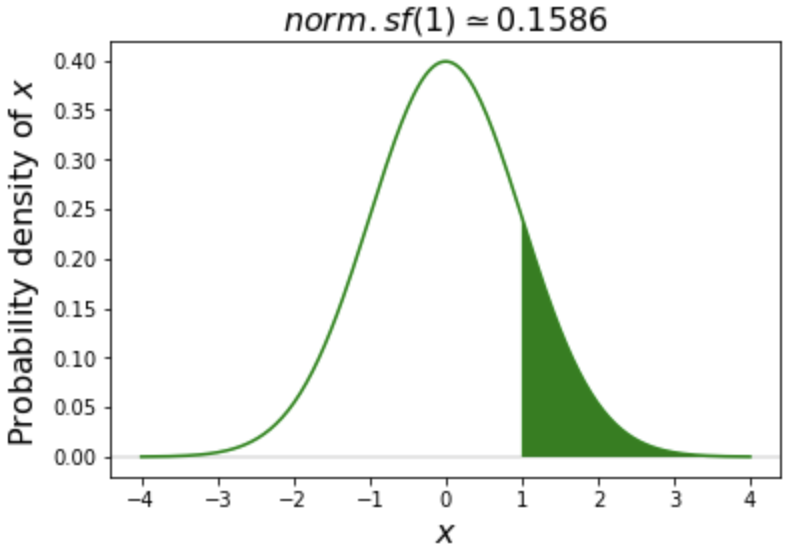

Tail probability

$$ $$

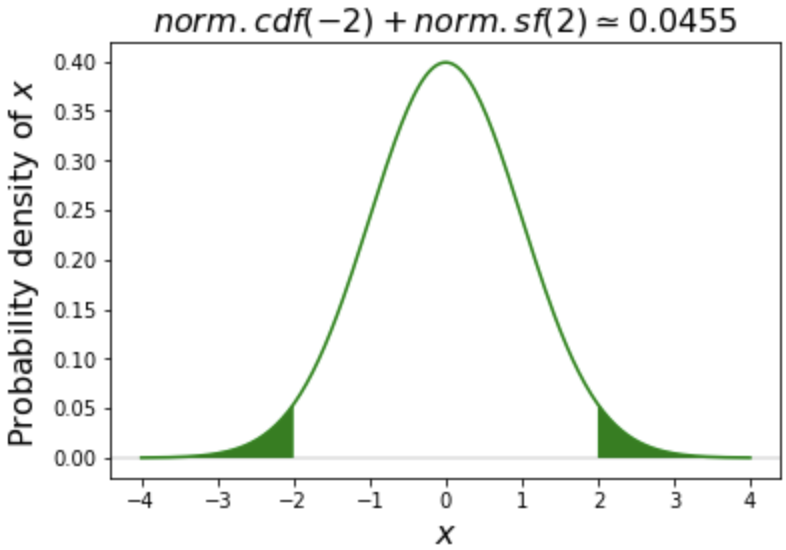

Tails

$$ $$

Tails (Cont.)

$$ $$

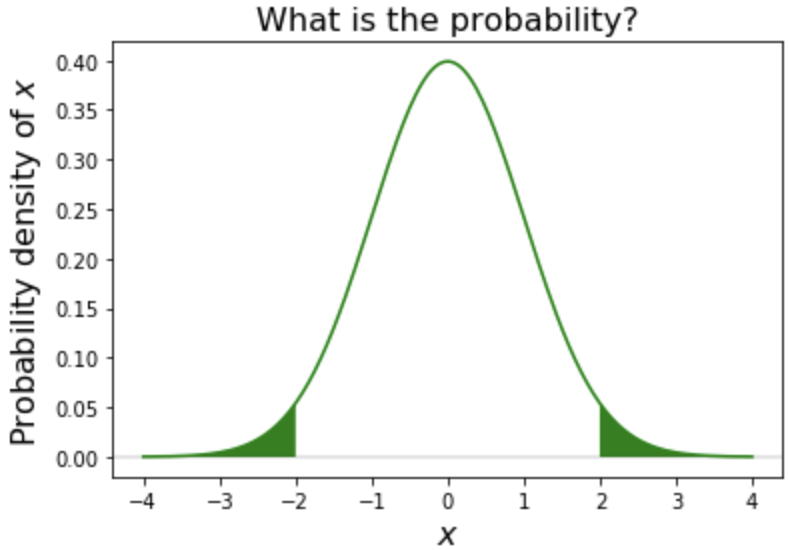

Intervals

$$ $$