Risk-adjusted metrics

Financial Analytics in Google Sheets

David Ardia

Professor in Quantitative Methods for Finance

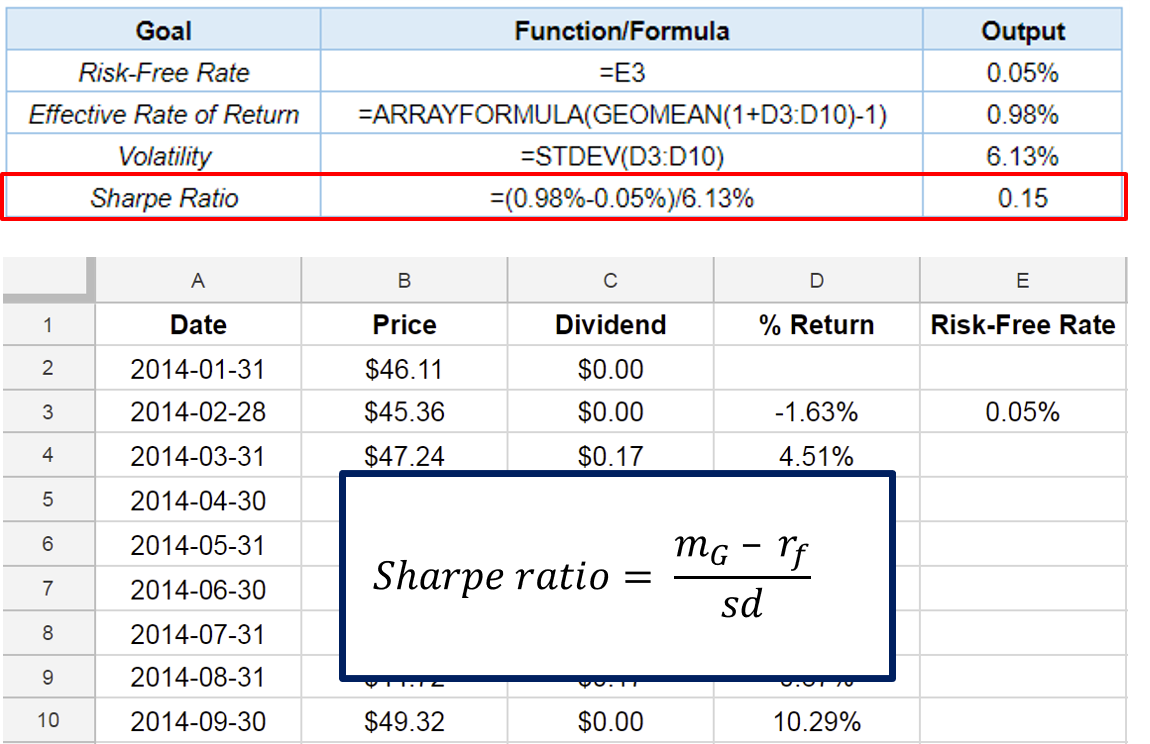

Sharpe ratio with Google Sheets

Volatility and Sharpe ratio

- High volatility penalizes the Sharpe ratio

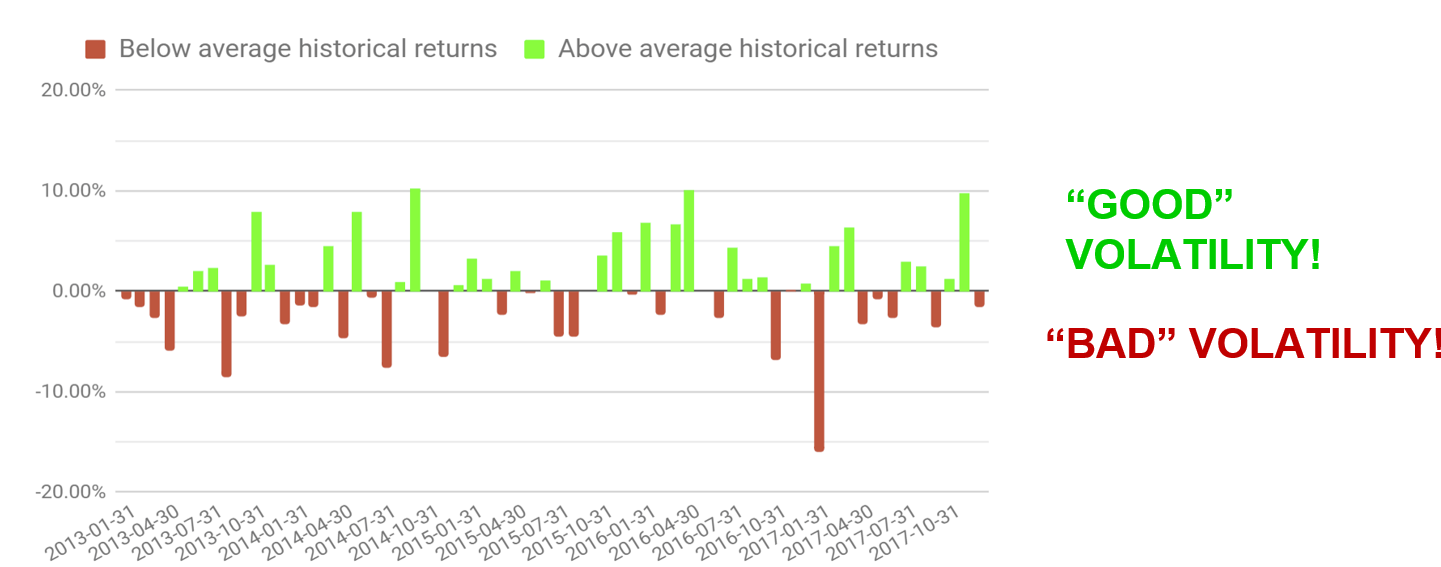

- Is volatility bad for investors?

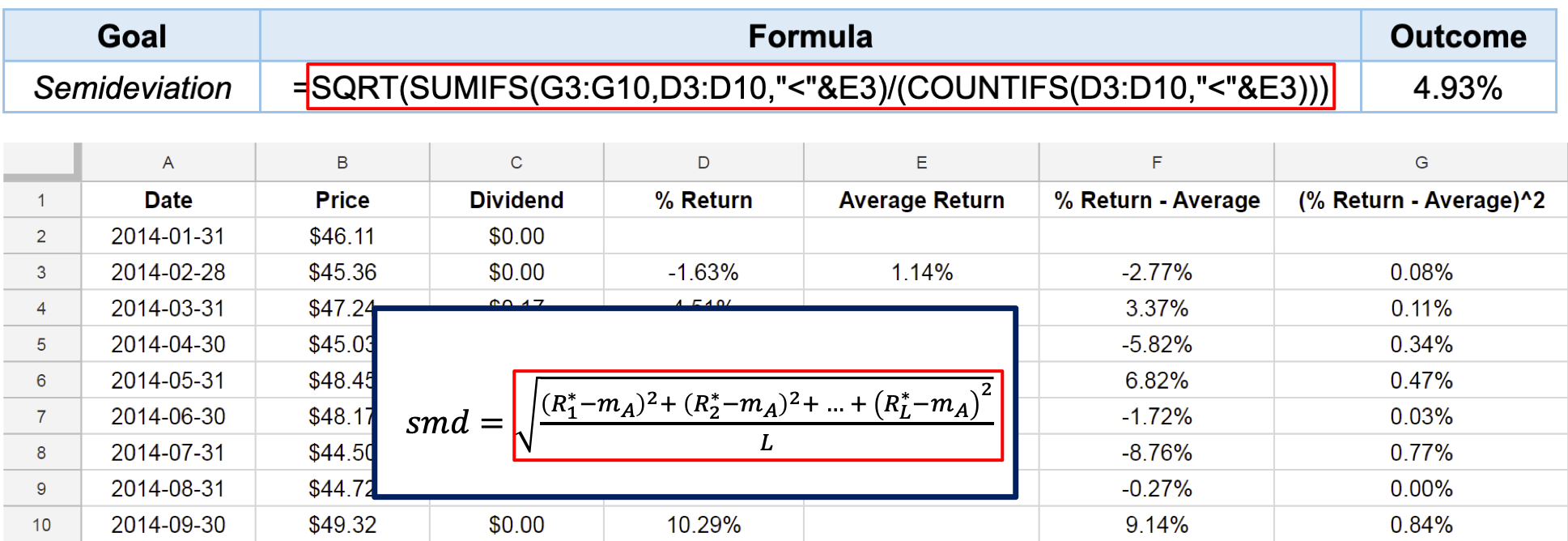

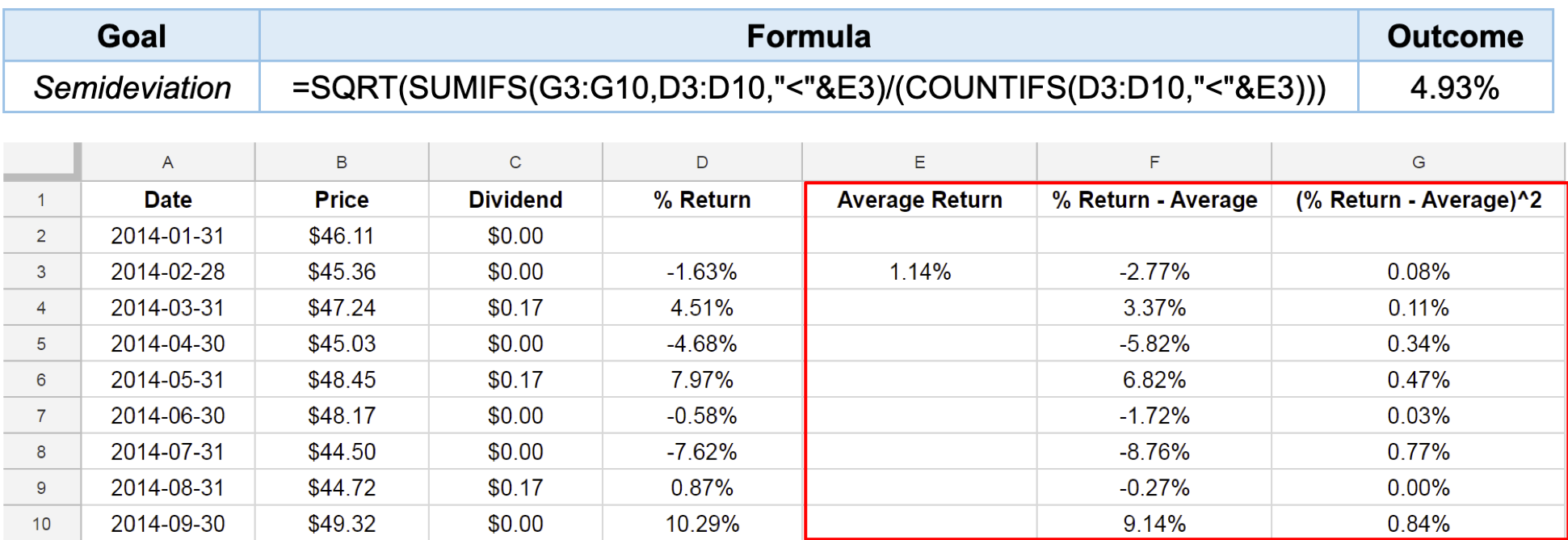

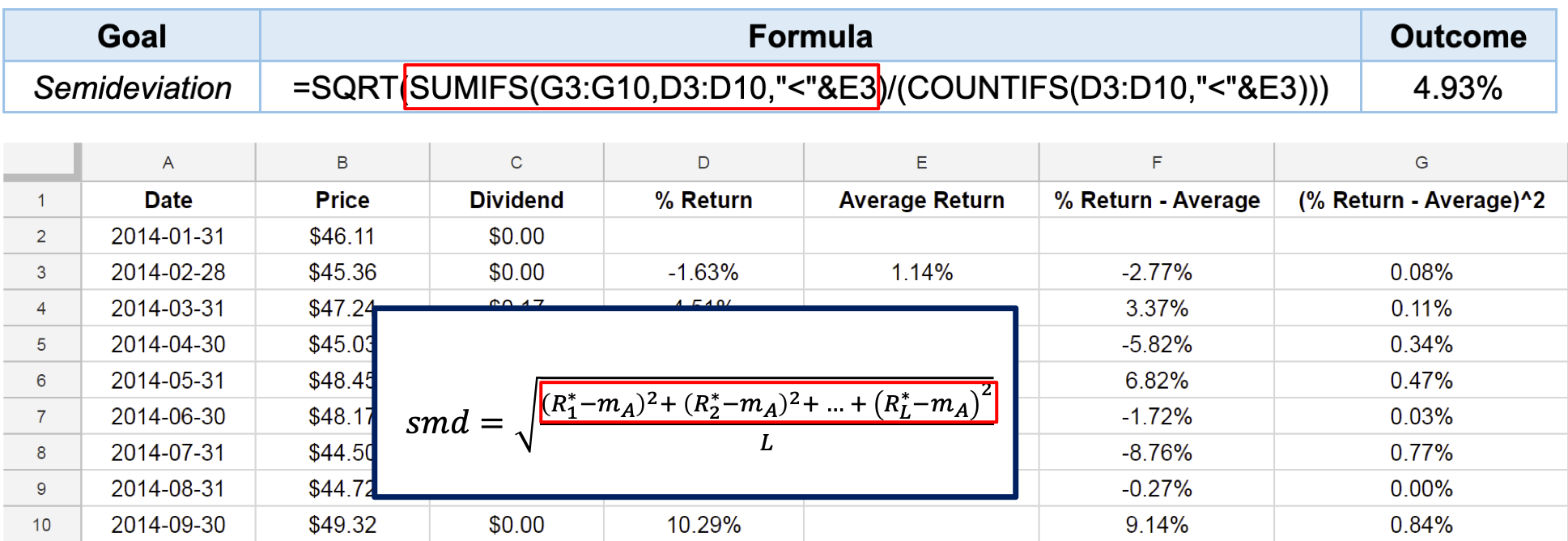

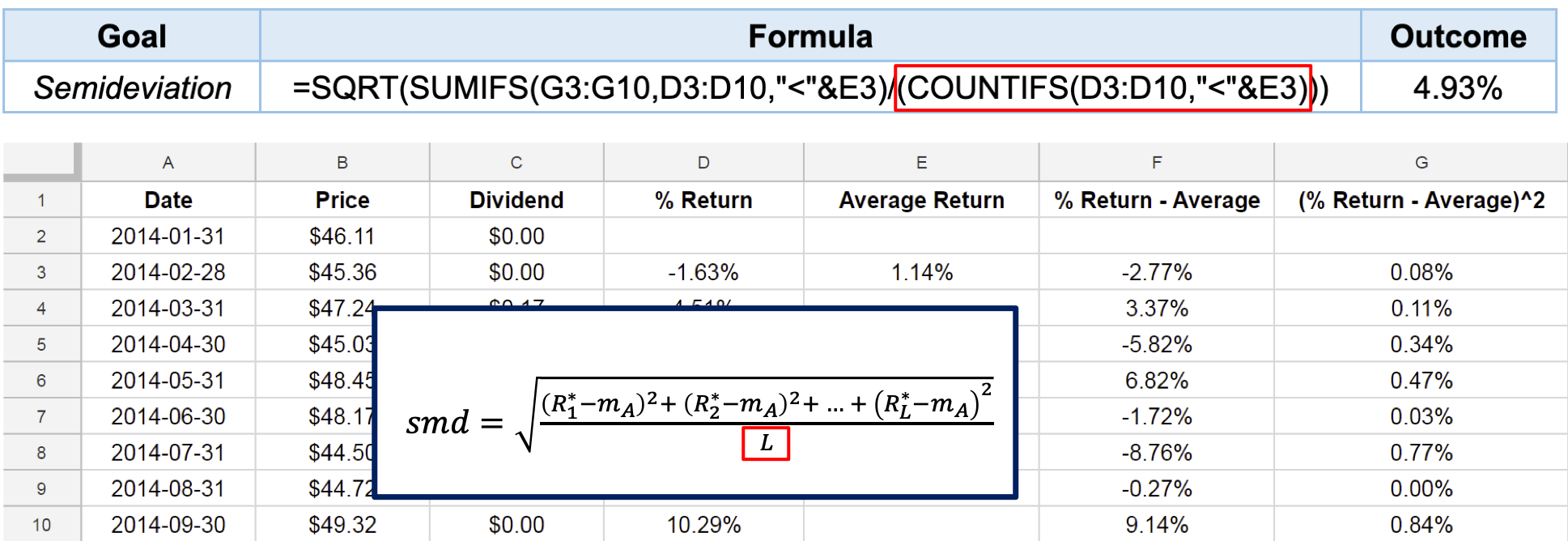

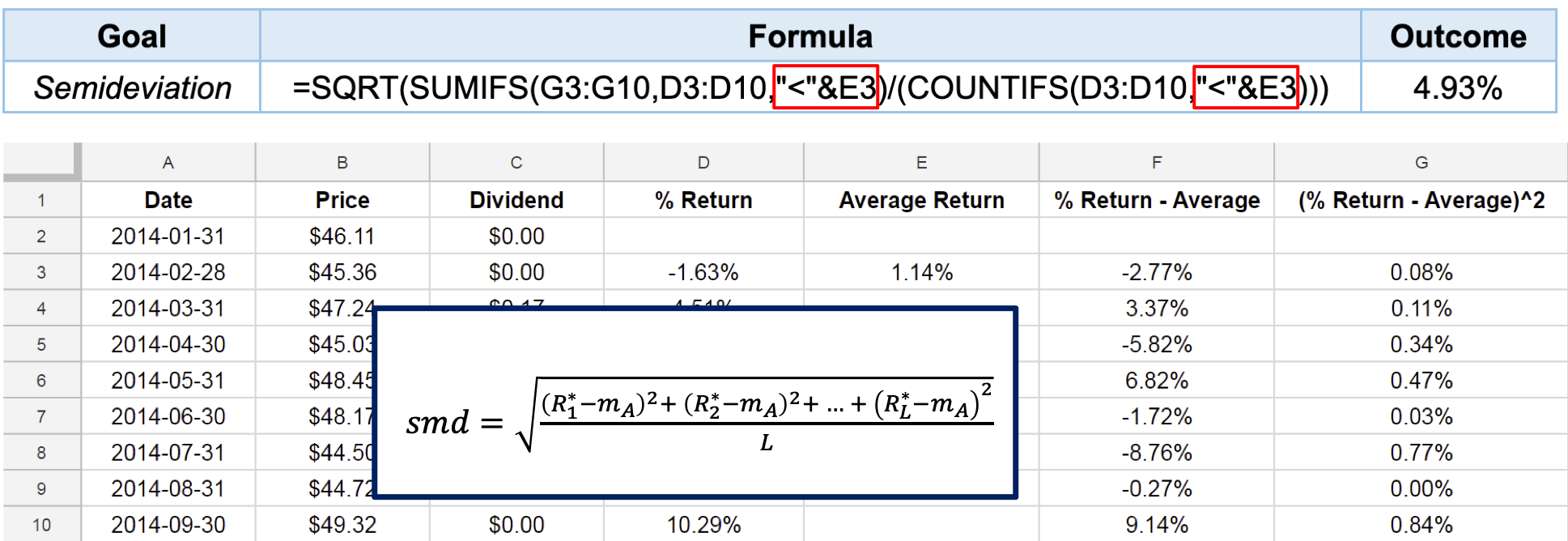

Semideviation with Google Sheets

Semideviation with Google Sheets

Semideviation with Google Sheets

Semideviation with Google Sheets

Semideviation with Google Sheets