Reward metrics

Financial Analytics in Google Sheets

David Ardia

Professor in Quantitative Methods for Finance

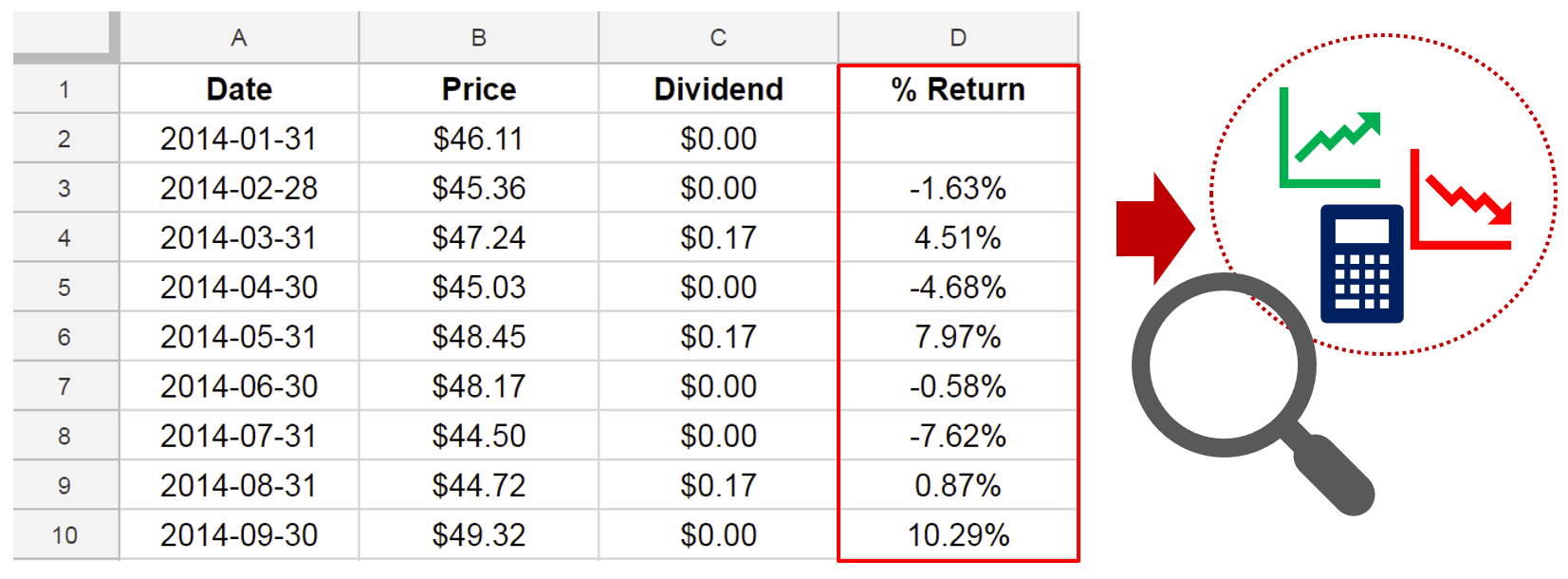

Return on investment

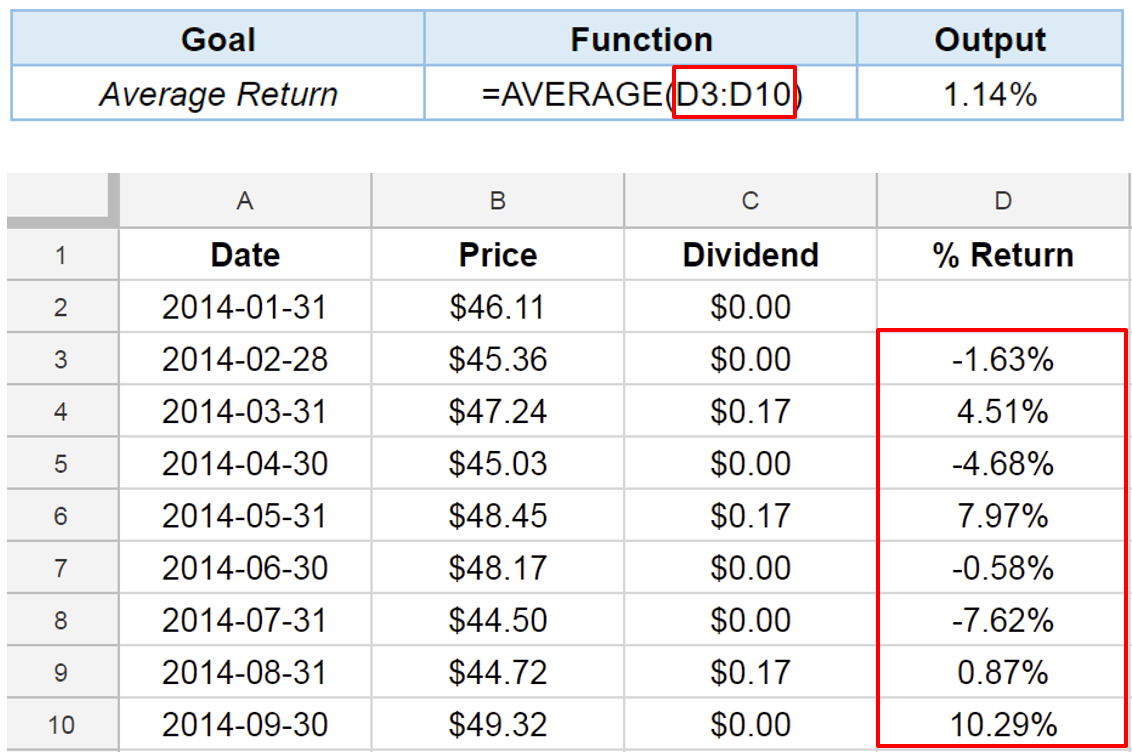

Average return

Function AVERAGE()

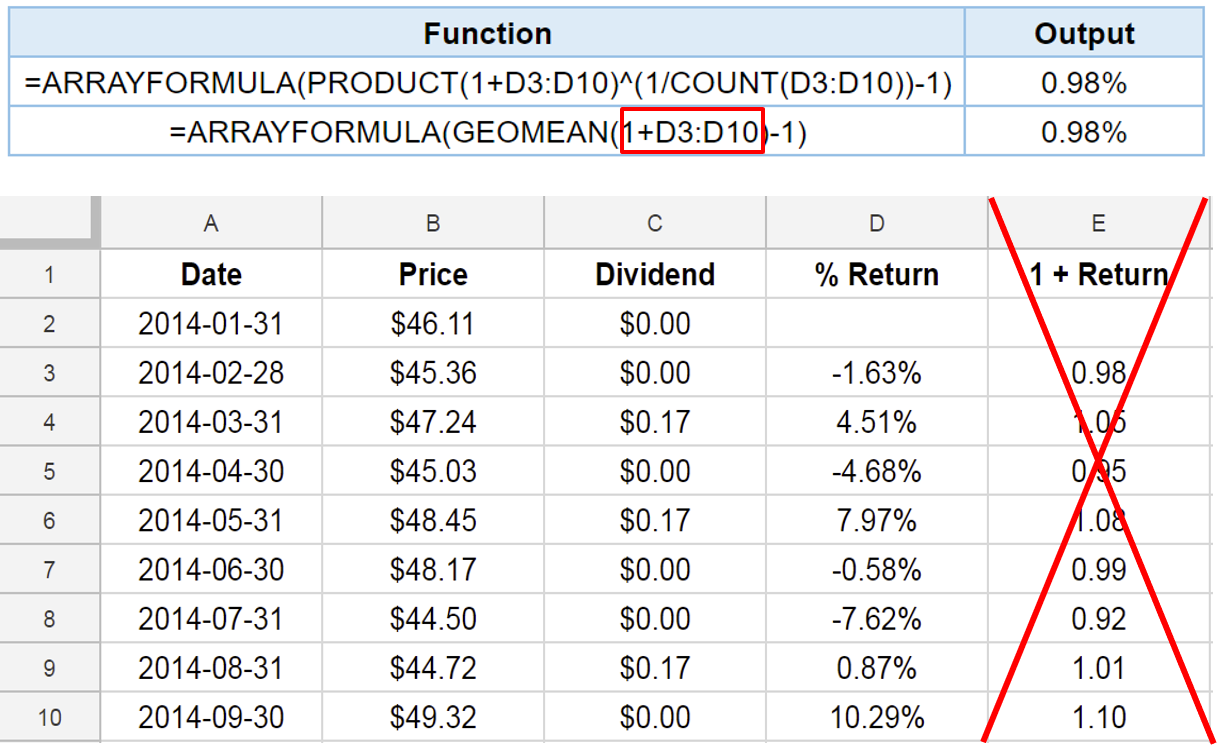

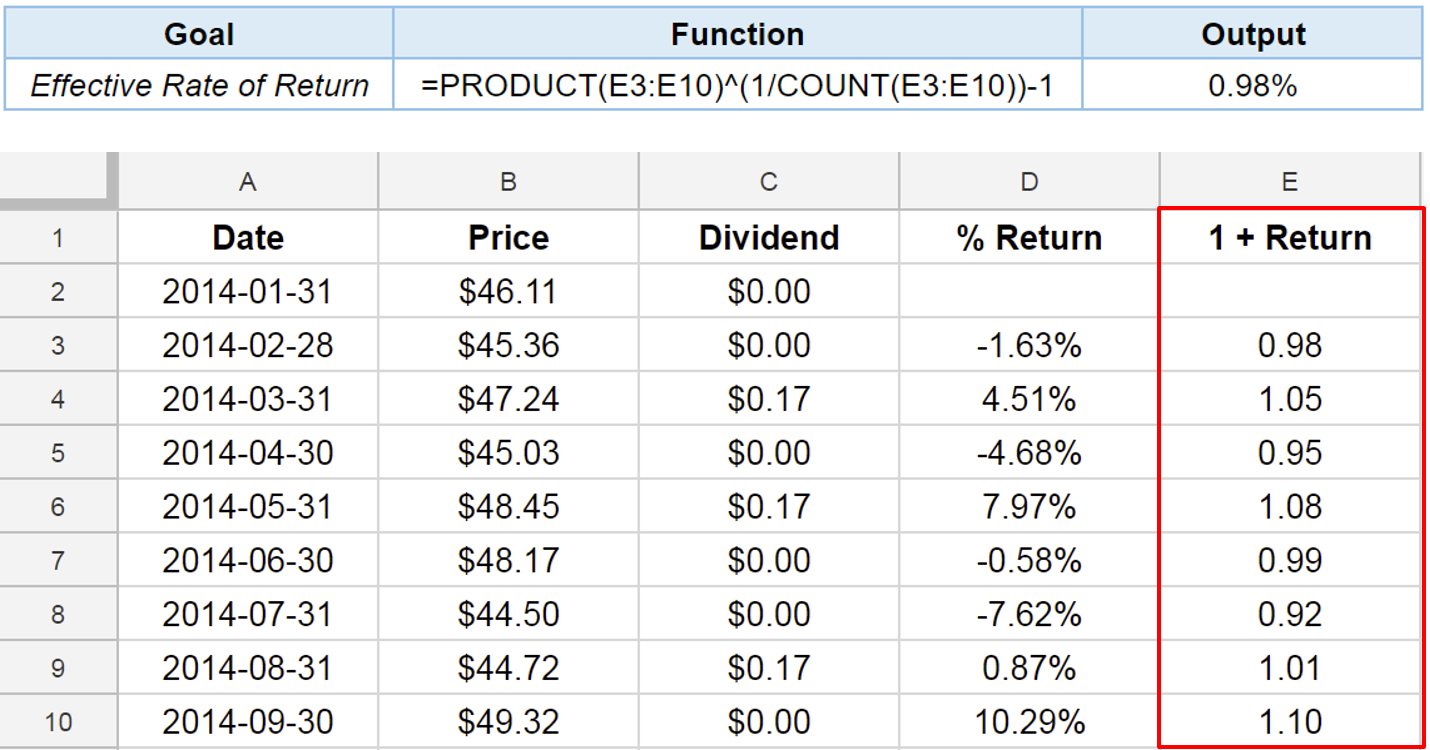

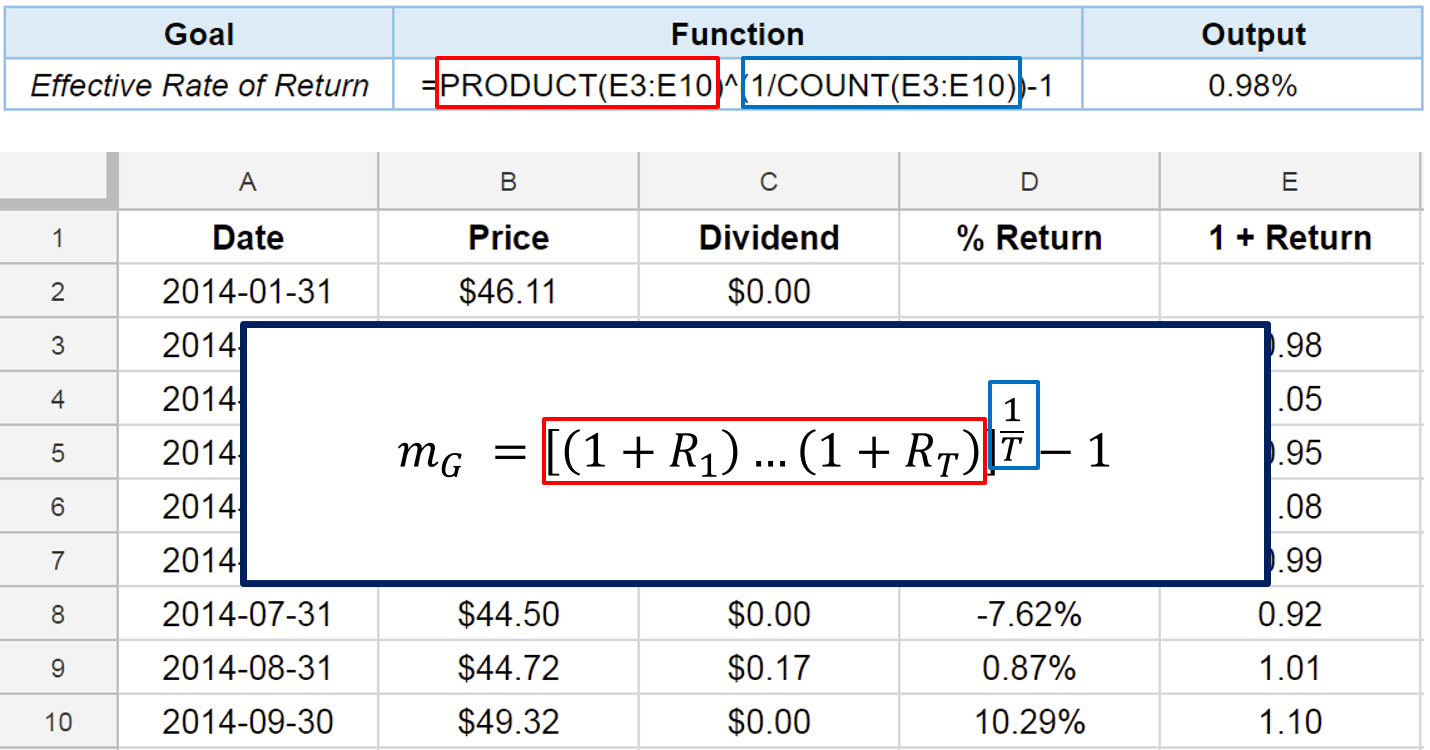

Effective rate of return: first approach

Effective rate of return: first approach

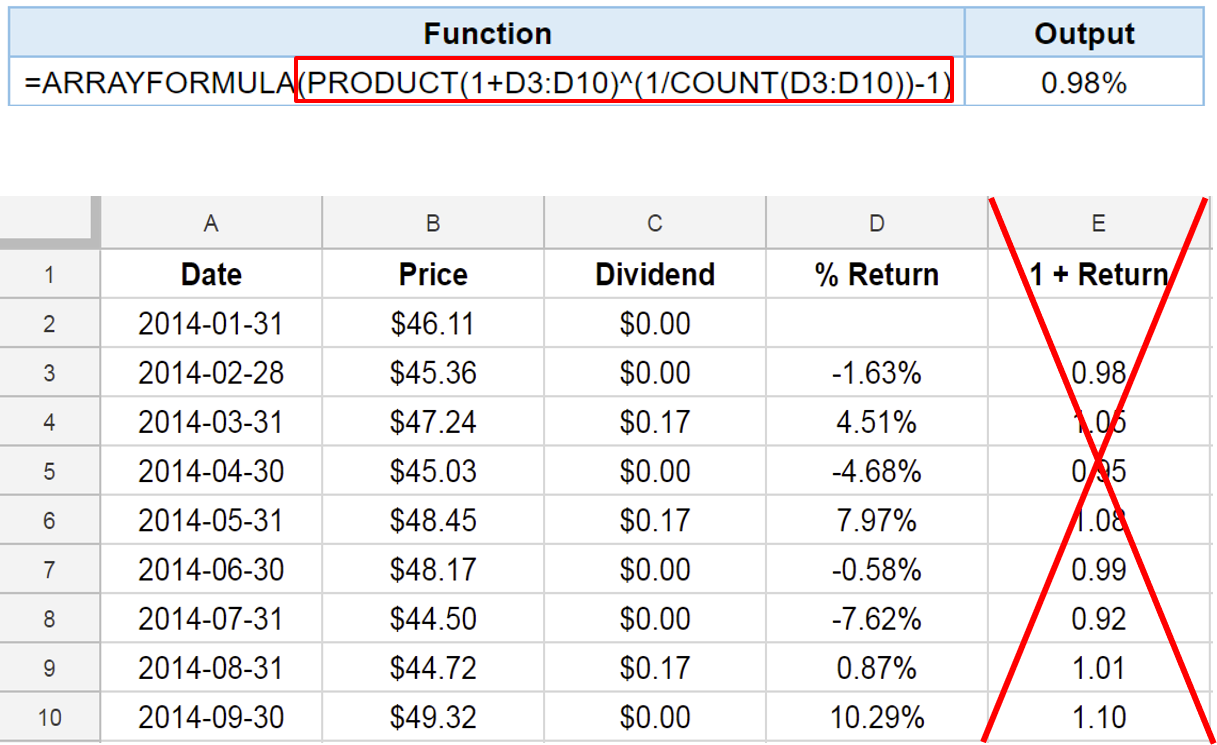

Function ARRAYFORMULA()

Functions ARRAYFORMULA() and GEOMEAN()