Optimization backtest

Intermediate Portfolio Analysis in R

Ross Bennett

Instructor

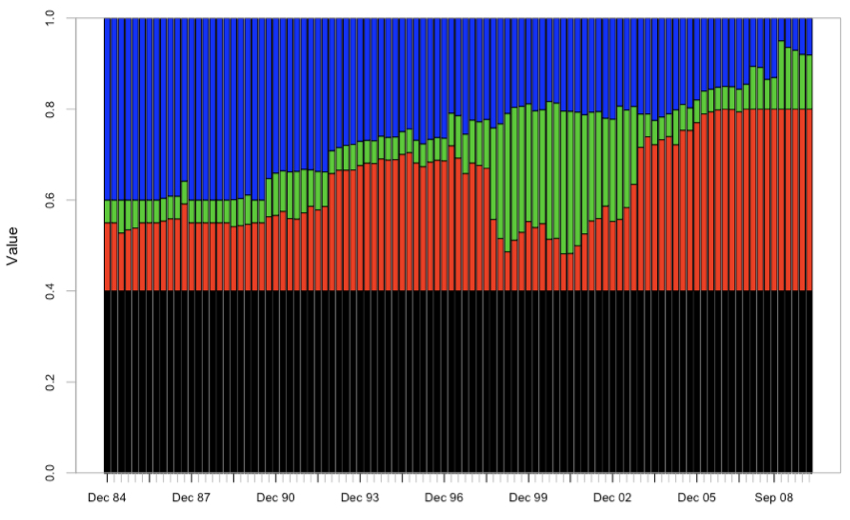

Optimization backtest: analysis

# Chart the optimal weights

chart.Weights(opt_base)

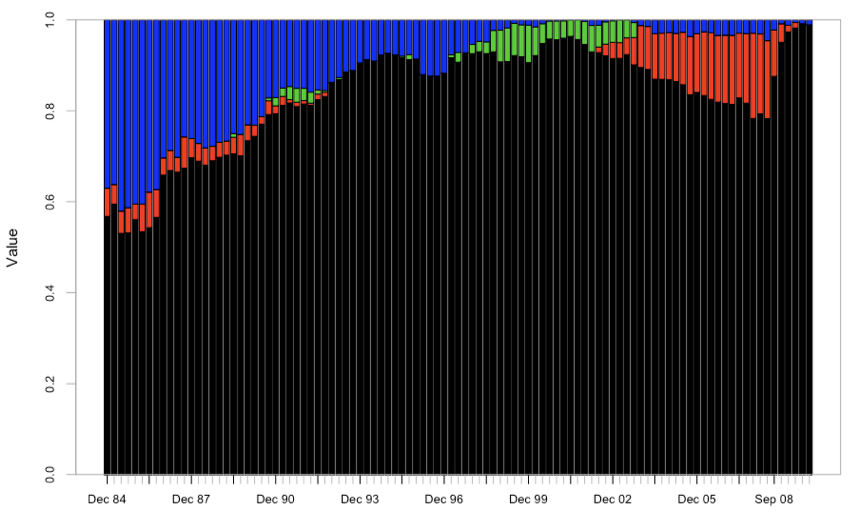

Optimization backtest: refine constraints

Optimization backtest: analysis refined constraints

# Chart the optimal weights

chart.Weights(opt_box)