Bond Valuation and Analysis in R

Clifford Ang

Senior Vice President, Compass Lexecon

$$

$$ C = \frac{P(down)+P(up)-2 \cdot P}{(P \cdot (\Delta y)^2} $$

$$\frac{\Delta P}{P} = 0.5 \cdot C \cdot (\Delta y)^2$$

$$\Delta P = 0.5 \cdot C \cdot (\Delta y)^2 \cdot P$$

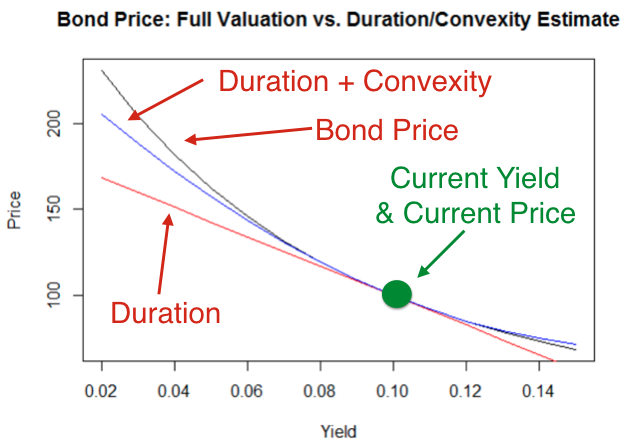

p

108.1109

(convexity <- (p_down + p_up - 2 * p) / (p * (0.01^2)))

77.56981

(convexity_pct_change <- 0.5 * convexity * 0.01 ^ 2)

0.00387849

(convexity_dollar_change <- 0.5 * convexity * 0.01 ^ 2 * p)

0.4193071

duration_dollar_change

-8.530203

convexity_dollar_change

duration_dollar_change + convexity_dollar_change

-8.110896

duration_dollar_change + convexity_dollar_change + p

100