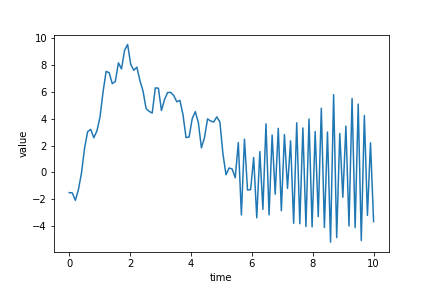

Making time series stationary

ARIMA Models in Python

James Fulton

Climate informatics researcher

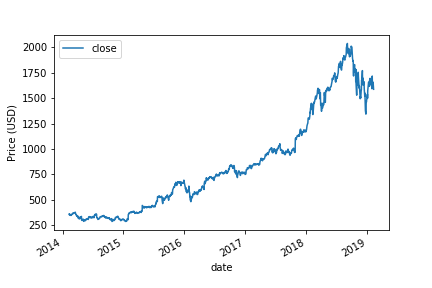

Applying the adfuller test

from statsmodels.tsa.stattools import adfuller

results = adfuller(df['close'])

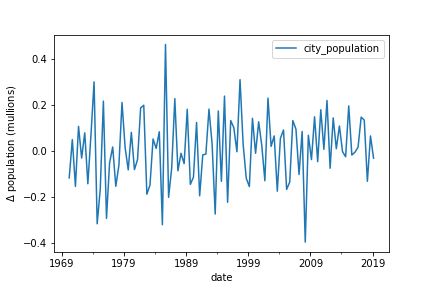

The value of plotting

Making a time series stationary

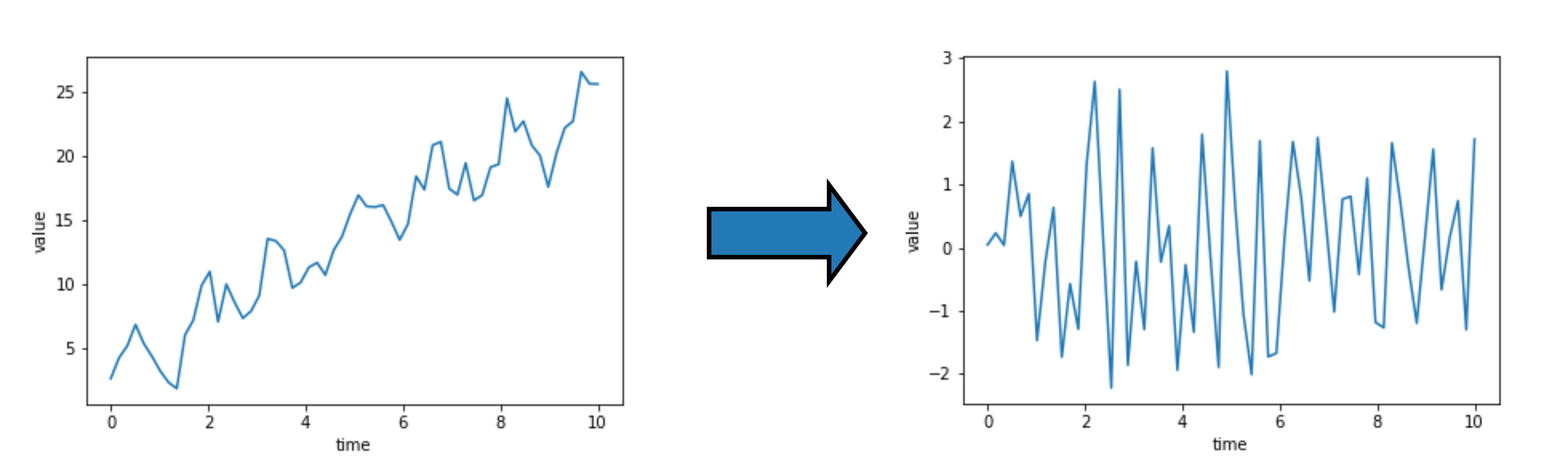

Taking the difference

Difference: $\Delta y_t = y_t - y_{t-1}$

Taking the difference