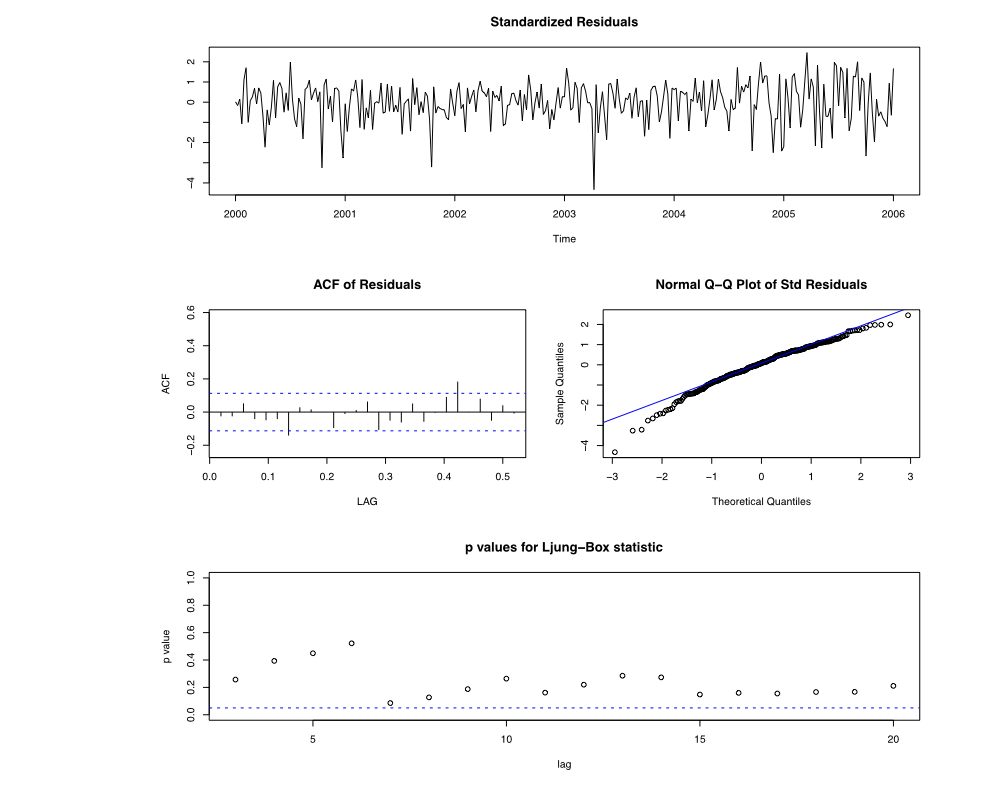

ARIMA diagnostics

ARIMA Models in R

David Stoffer

Professor of Statistics at the University of Pittsburgh

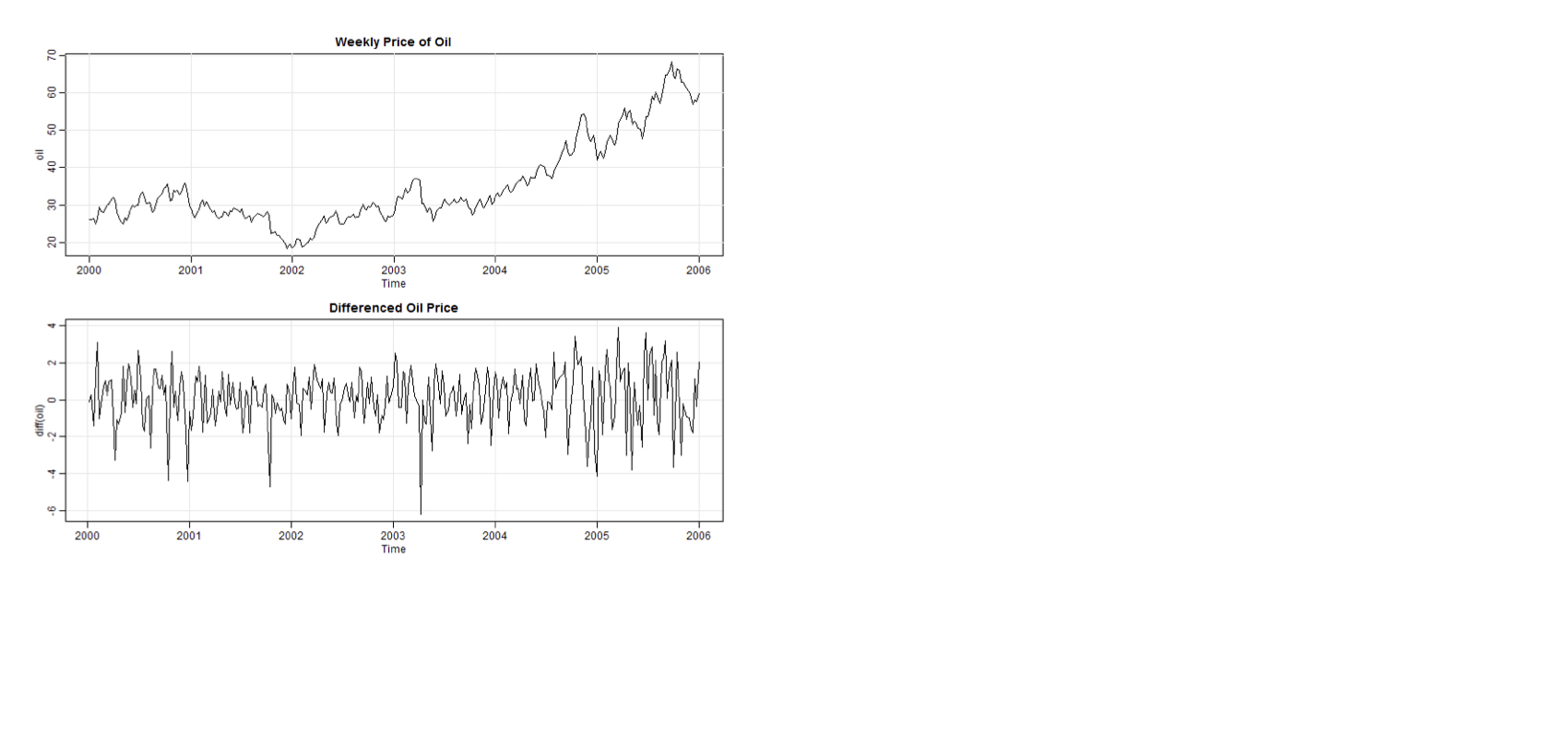

Weekly Oil Prices ARIMA(1, 1, 1)?

Weekly Oil Prices ARIMA(1, 1, 1)?

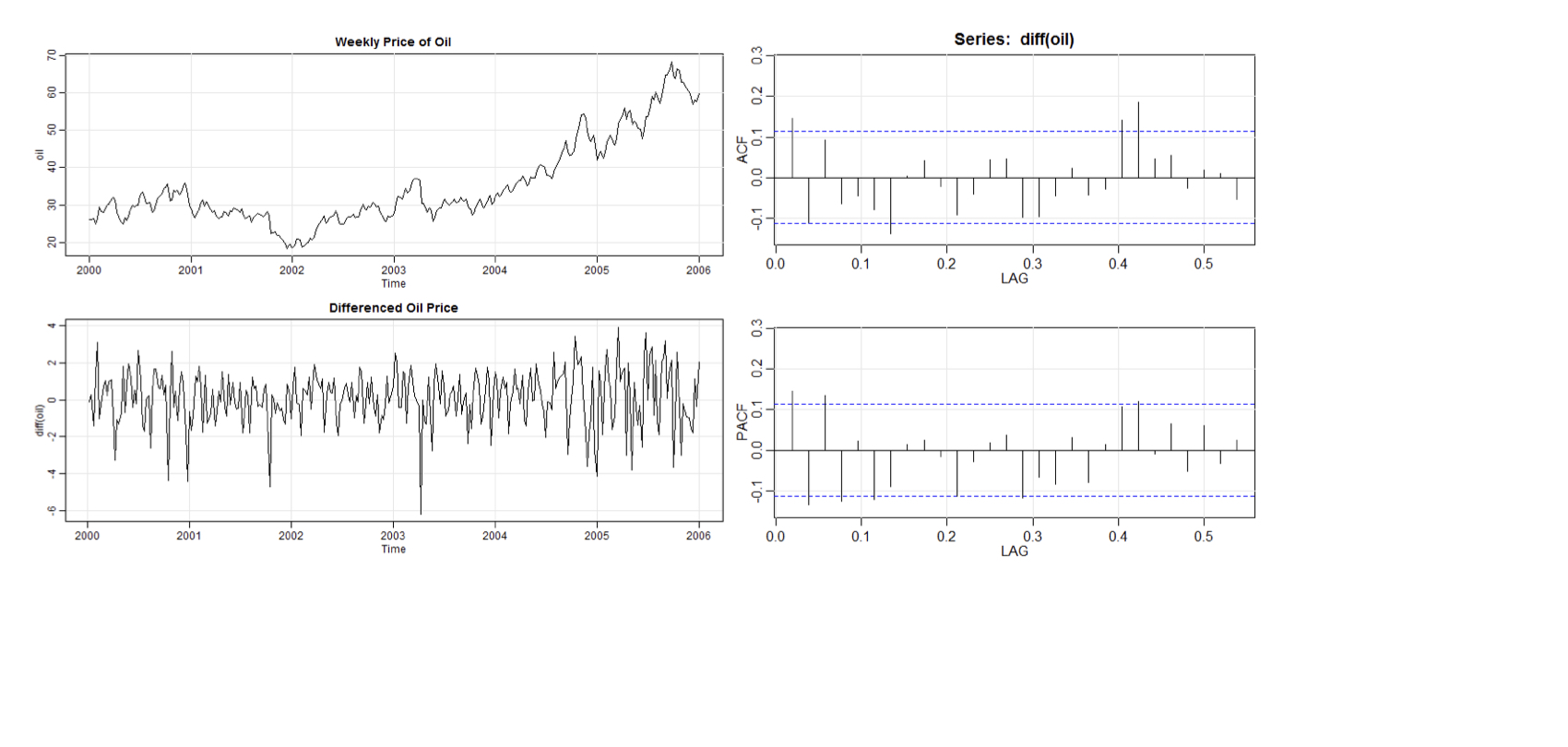

Weekly Oil Prices ARIMA(1, 1, 1)!

ARIMA Models in R

David Stoffer

Professor of Statistics at the University of Pittsburgh