First things first

ARIMA Models in R

David Stoffer

Professor of Statistics at the University of Pittsburgh

About Me

About Me

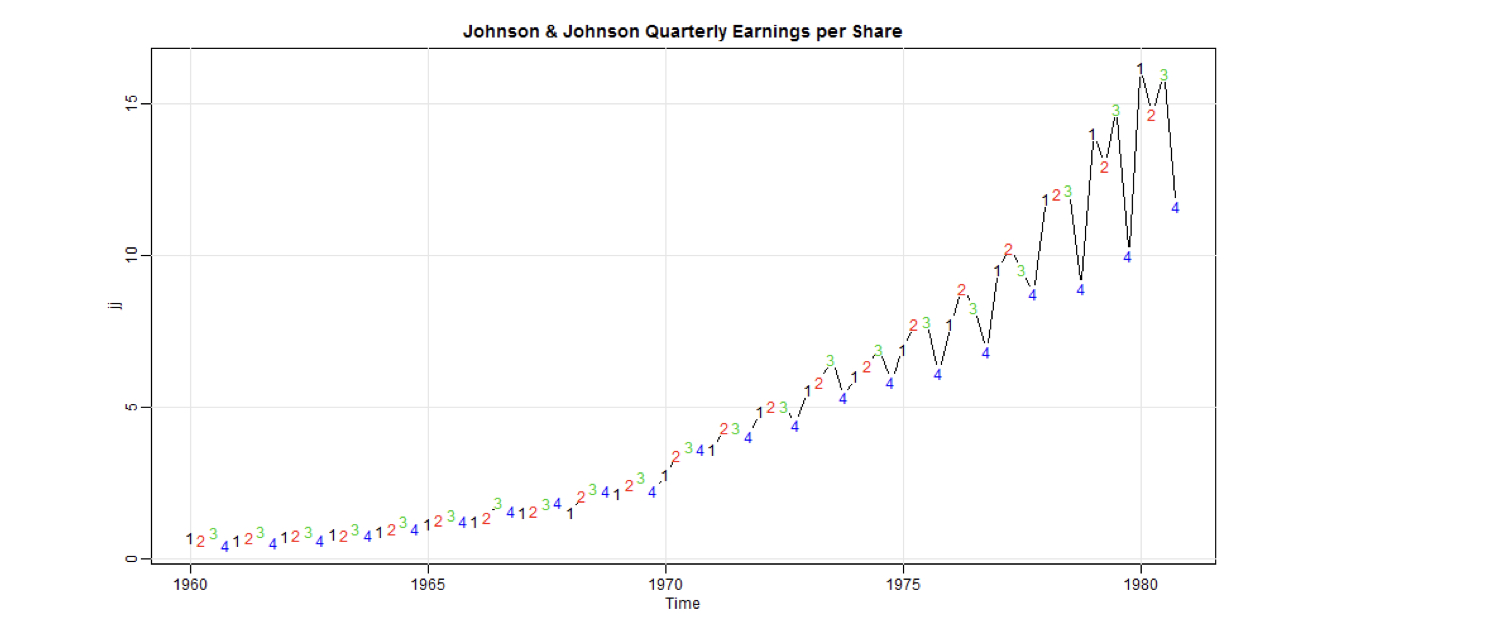

Time Series Data - I

library(astsa)

plot(jj, main = "Johnson & Johnson Quarterly Earnings per Share", type = "c")

text(jj, labels = 1:4, col = 1:4)

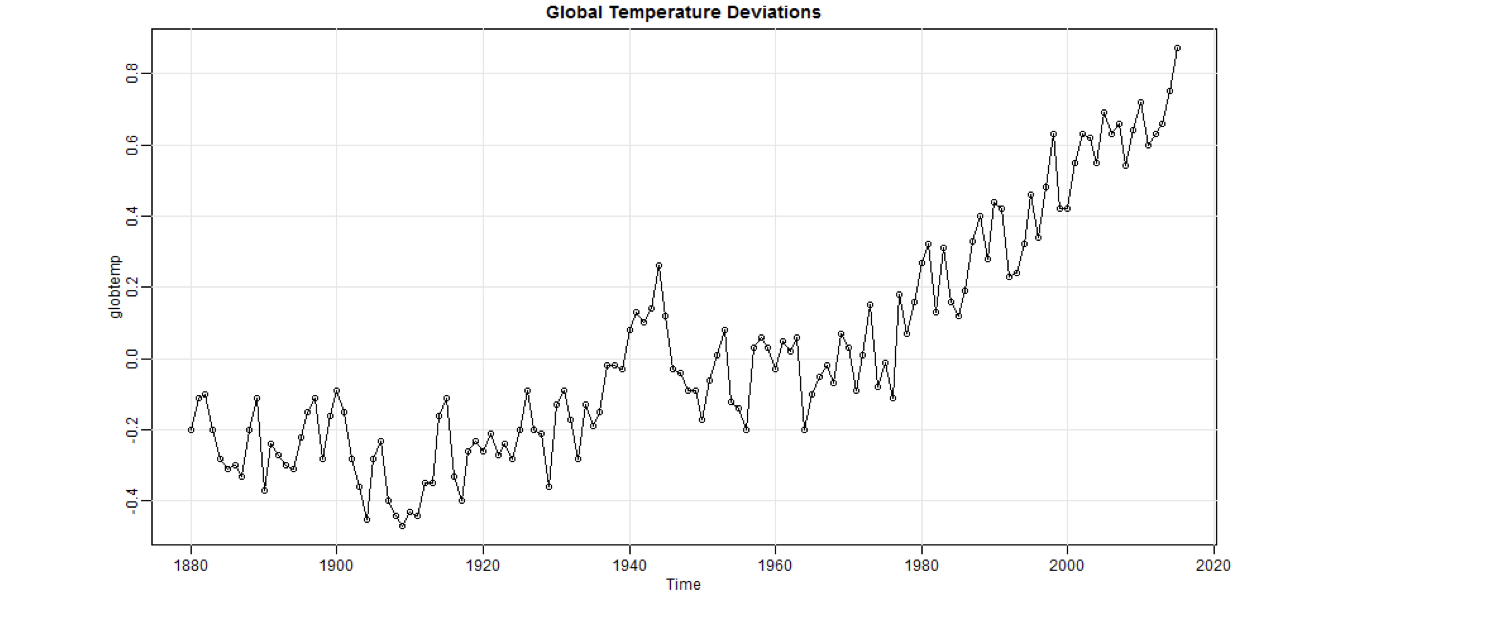

Time Series Data - II

library(astsa)

plot(globtemp, main = "Global Temperature Deviations", type= "o")

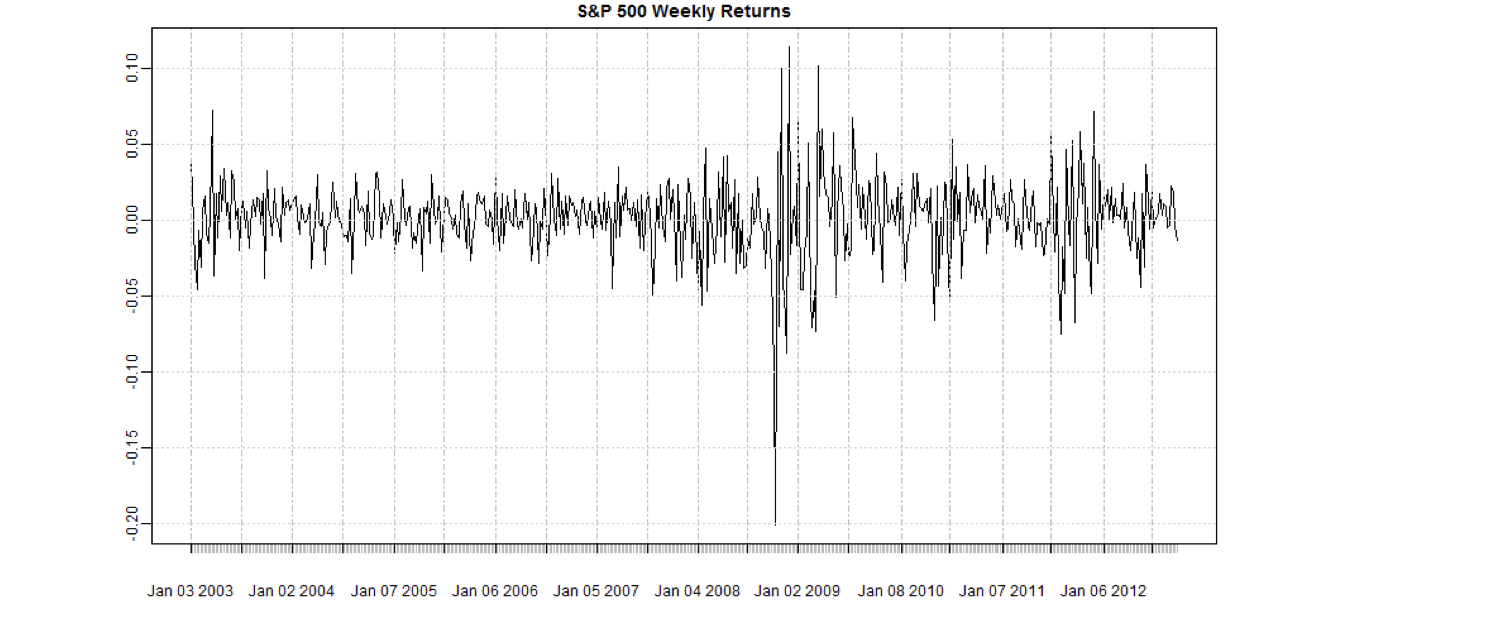

Time Series Data - III

library(xts)

plot(sp500w, main = "S&P 500 Weekly Returns")