ARIMA - integrated ARMA

ARIMA Models in R

David Stoffer

Professor of Statistics at the University of Pittsburgh

Identifying ARIMA

- A time series exhibits ARIMA behavior if the differenced data has ARMA behavior

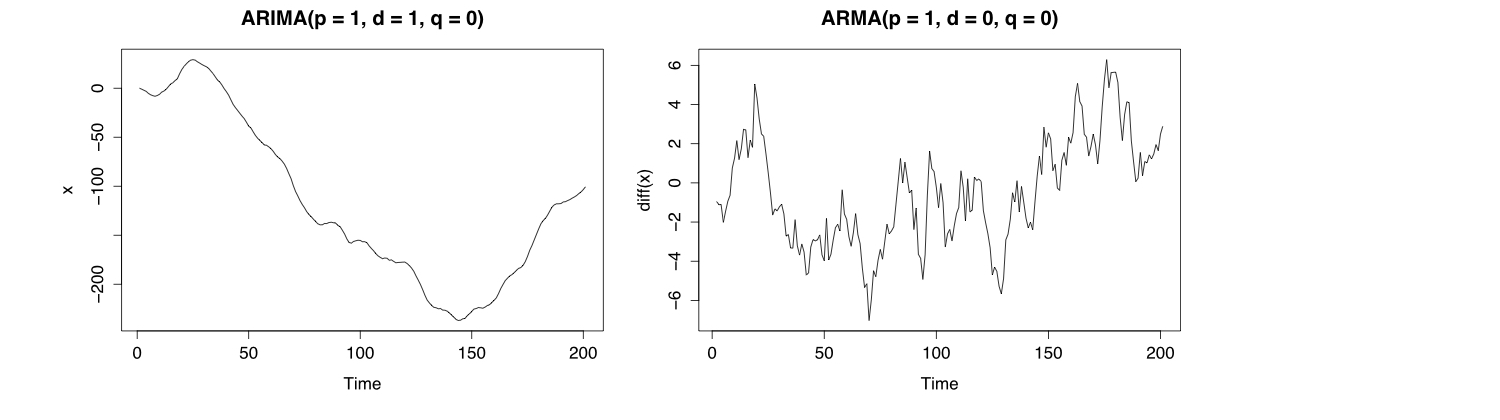

# Simulation ARIMA(p = 1, d = 1, q = 0)

x <- arima.sim(list(order = c(1, 1, 0), ar = .9), n = 200)

plot(x, main = "ARIMA(p = 1, d = 1, q = 0)")

plot(diff(x), main = "ARMA(p = 1, d = 0, q = 0)")

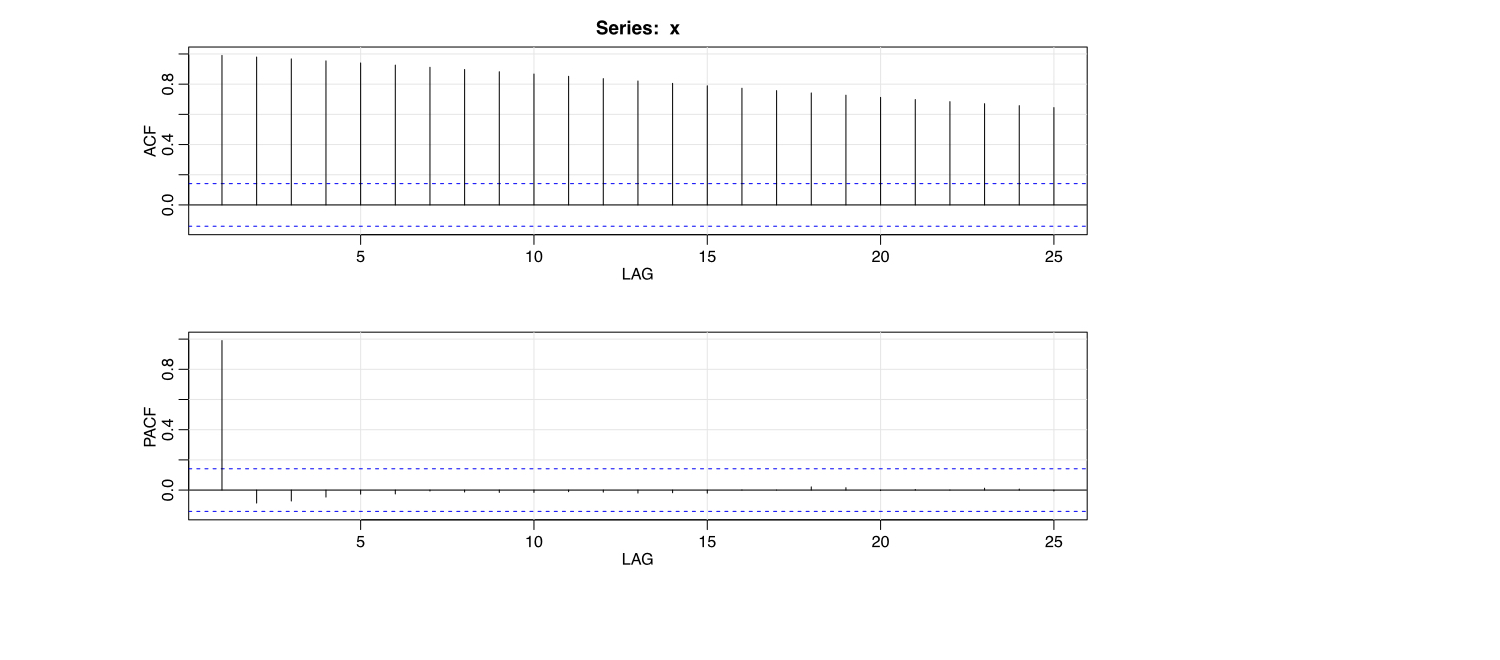

ACF and PCF of an Integrated ARMA

x <- arima.sim(list(order = c(1, 1, 0), ar = .9), n = 200)

acf2(x)

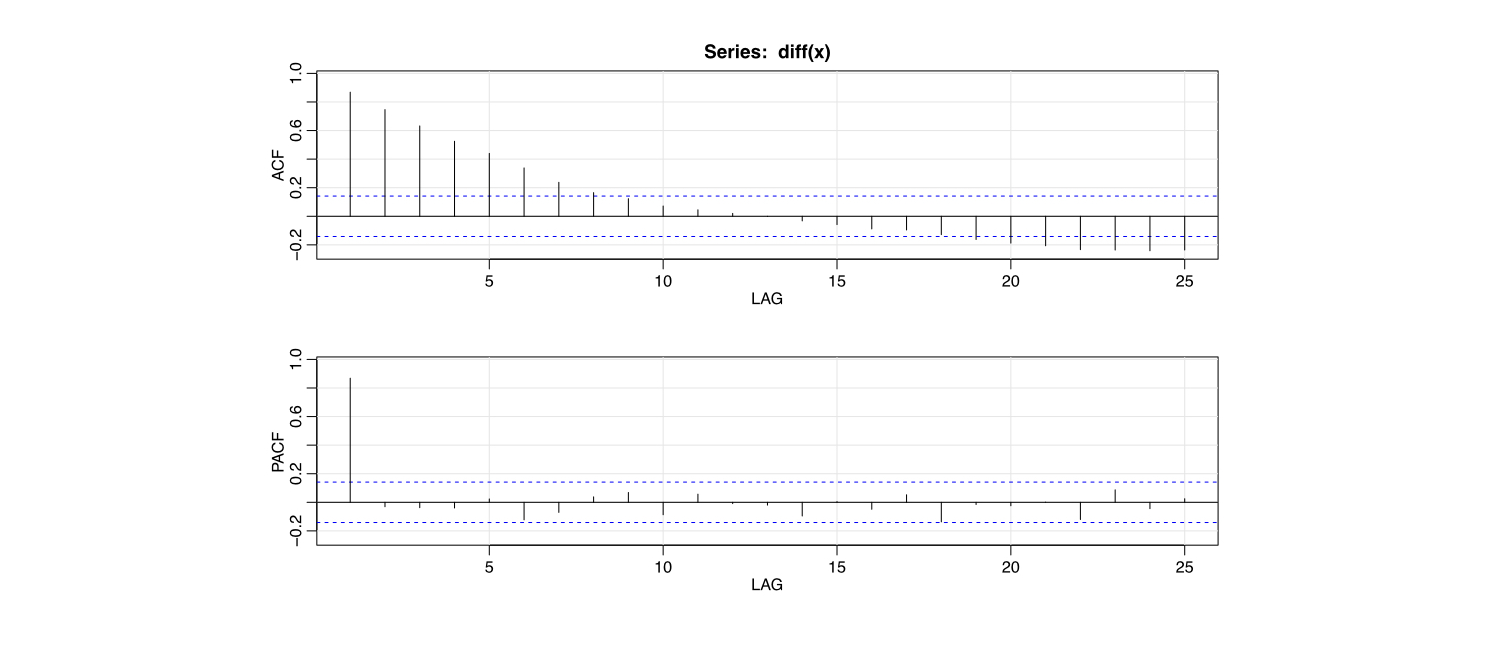

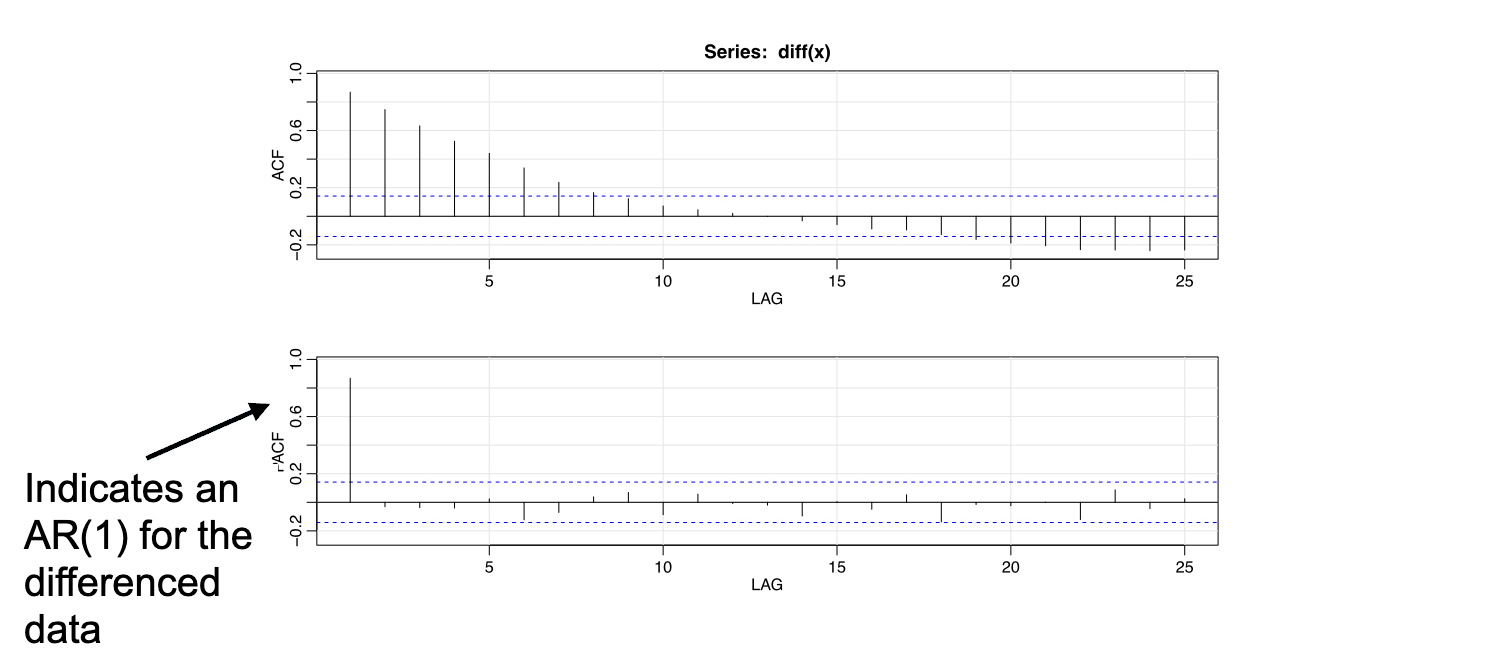

ACF and PCF of a Differenced ARIMA

x <- arima.sim(list(order = c(1, 1, 0), ar = .9), n = 200)

acf2(diff(x))

ACF and PCF of a Differenced ARIMA

x <- arima.sim(list(order = c(1, 1, 0), ar = .9), n = 200)

acf2(diff(x))

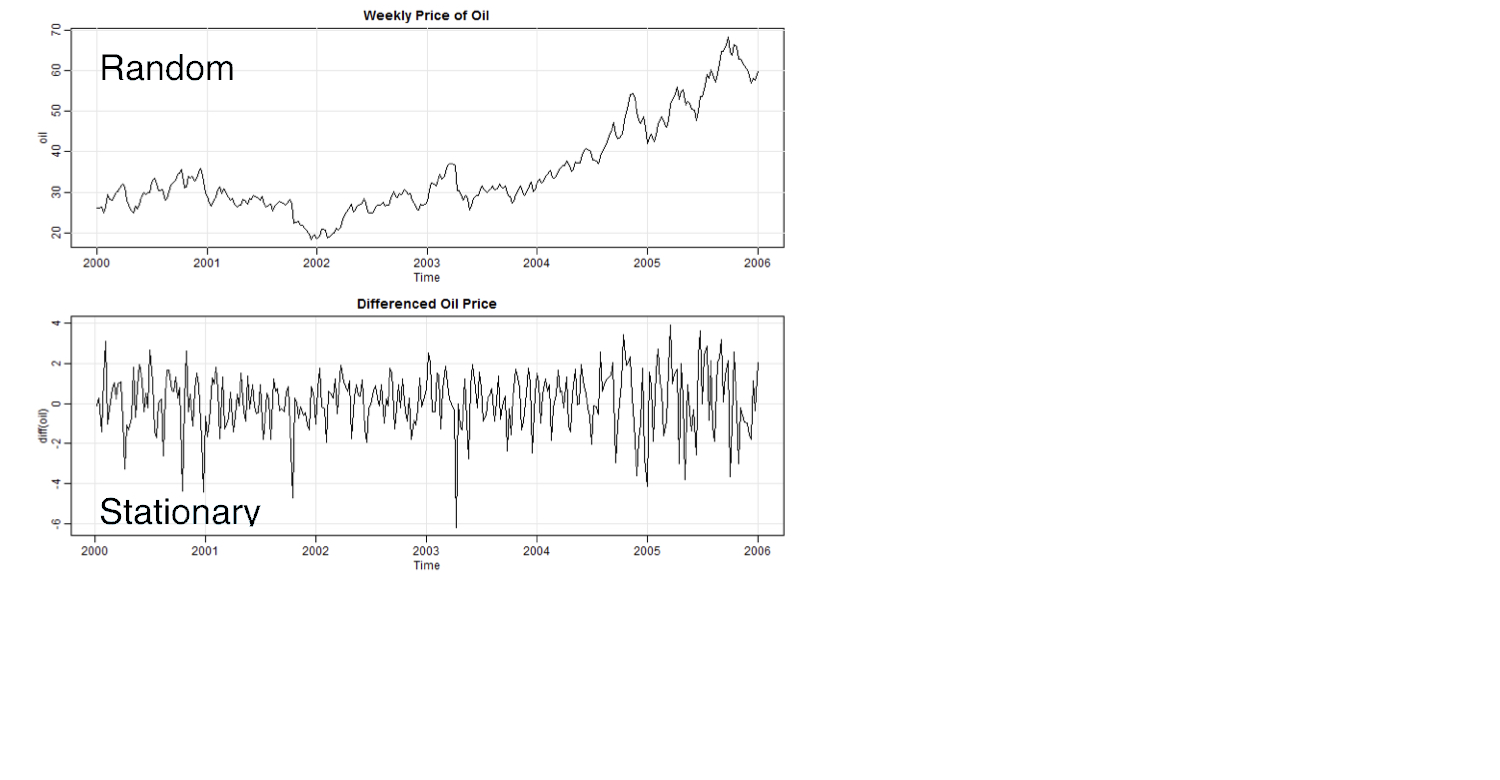

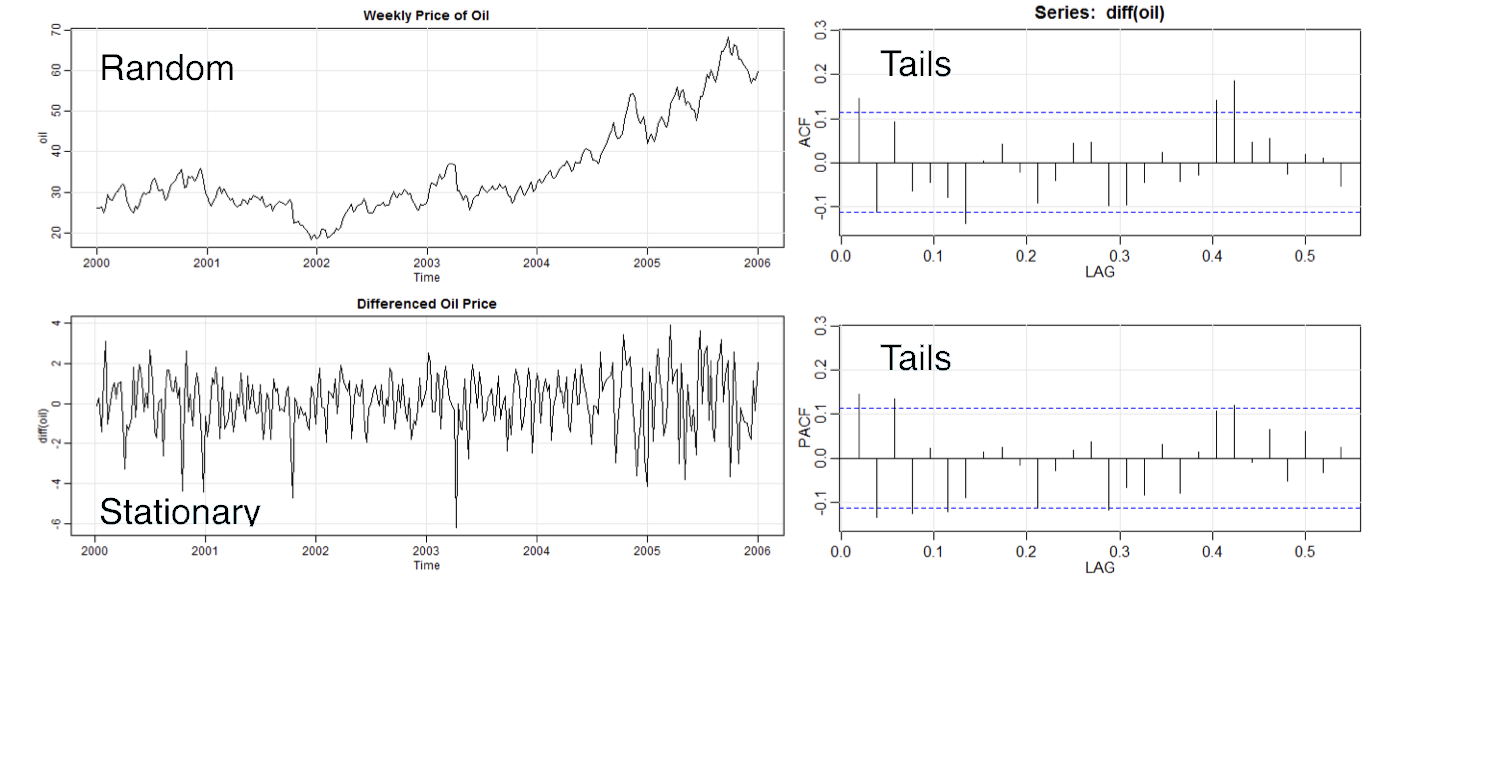

Weekly Oil Prices

Weekly Oil Prices

- Looks like

ARIMA(1, 1, 1)