Stationarity and nonstationarity

ARIMA Models in R

David Stoffer

Professor of Statistics at the University of Pittsburgh

Stationarity

A time series is stationary when it is "stable", meaning:

- the mean is constant over time (no trend)

- the correlation structure remains constant over time

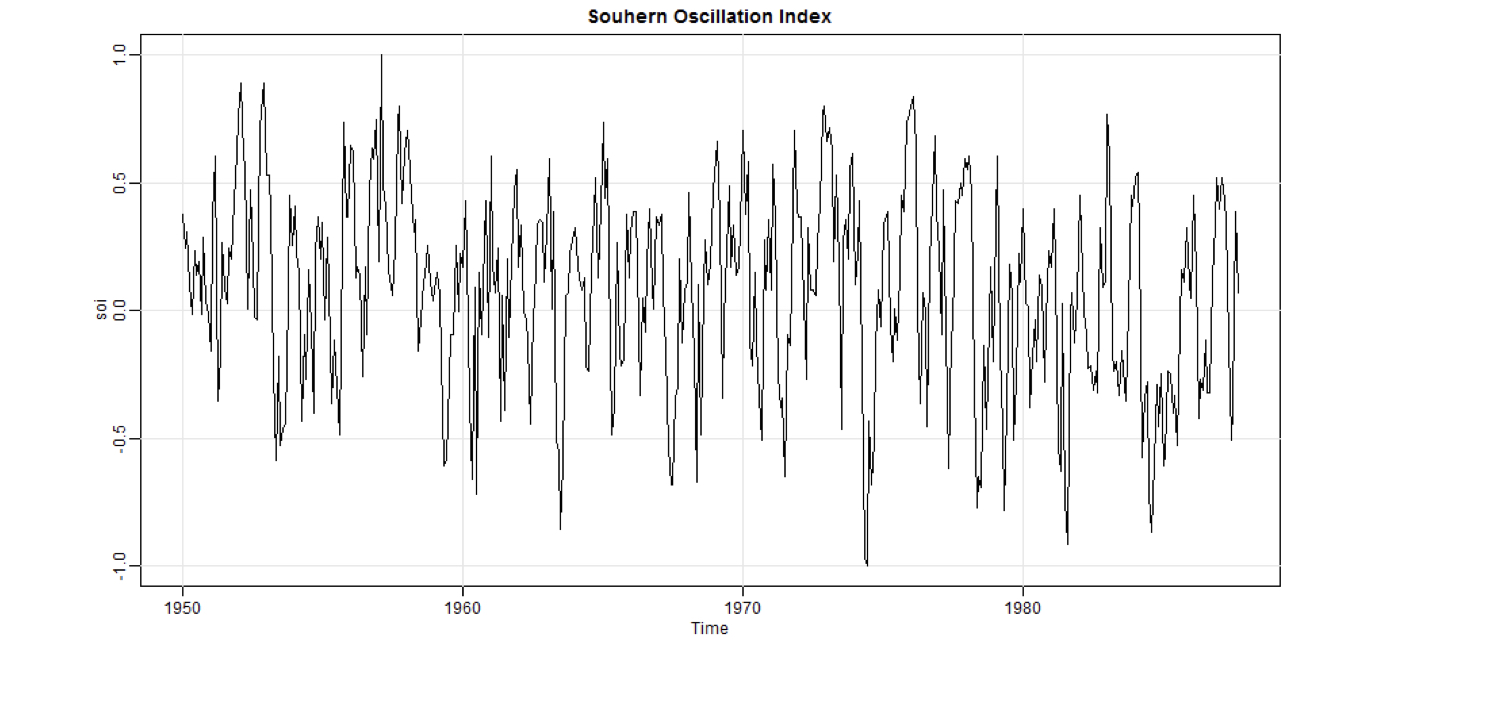

Southern Oscillation Index

Reasonable to assume stationary, but perhaps some slight trend.

Southern Oscillation Index

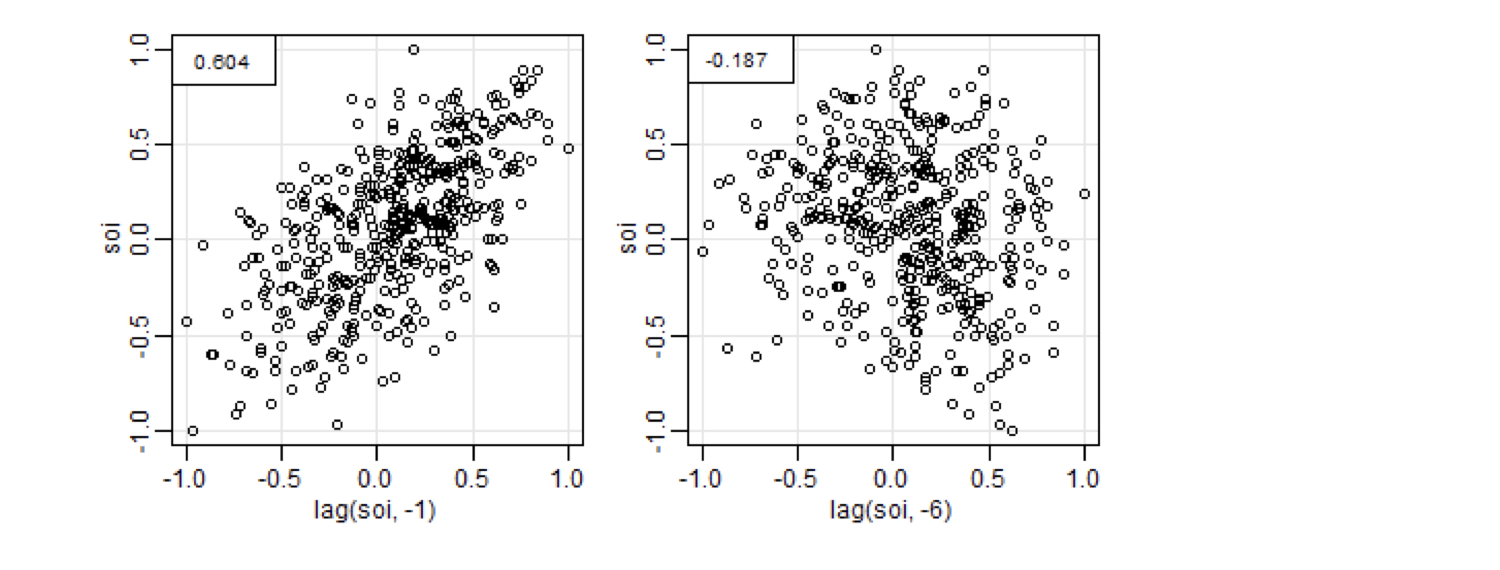

To estimate autocorrelation, compute the correlation coefficient between the time series and itself at various lags.

Here you see how to get the correlation at lag 1 and lag 6.

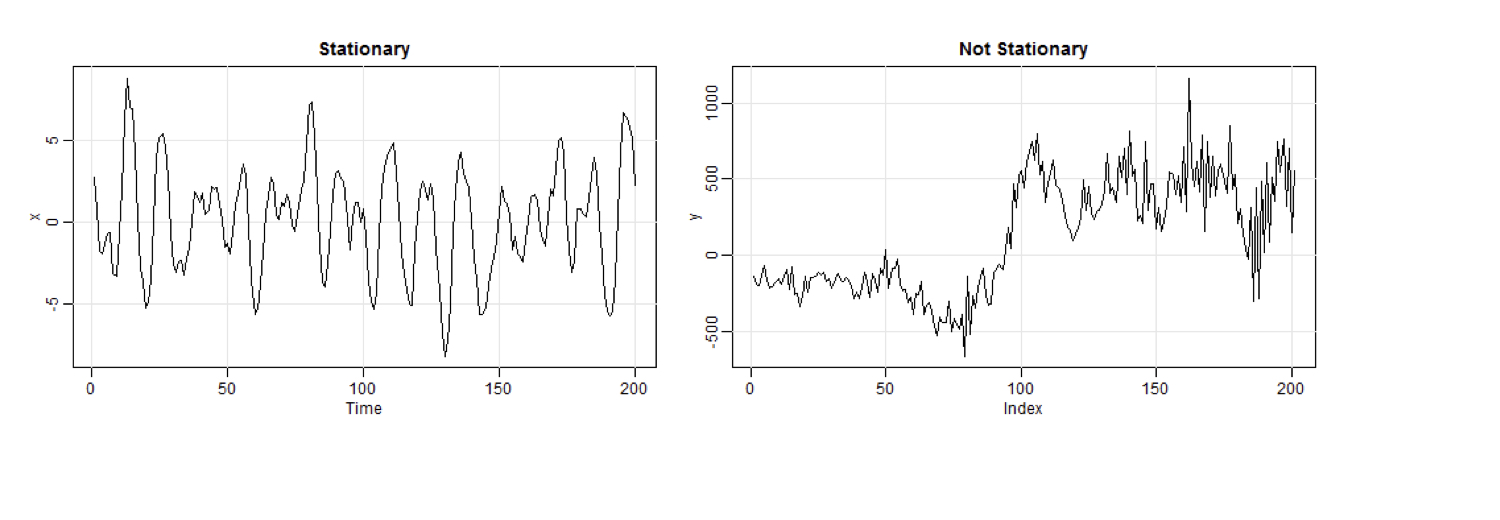

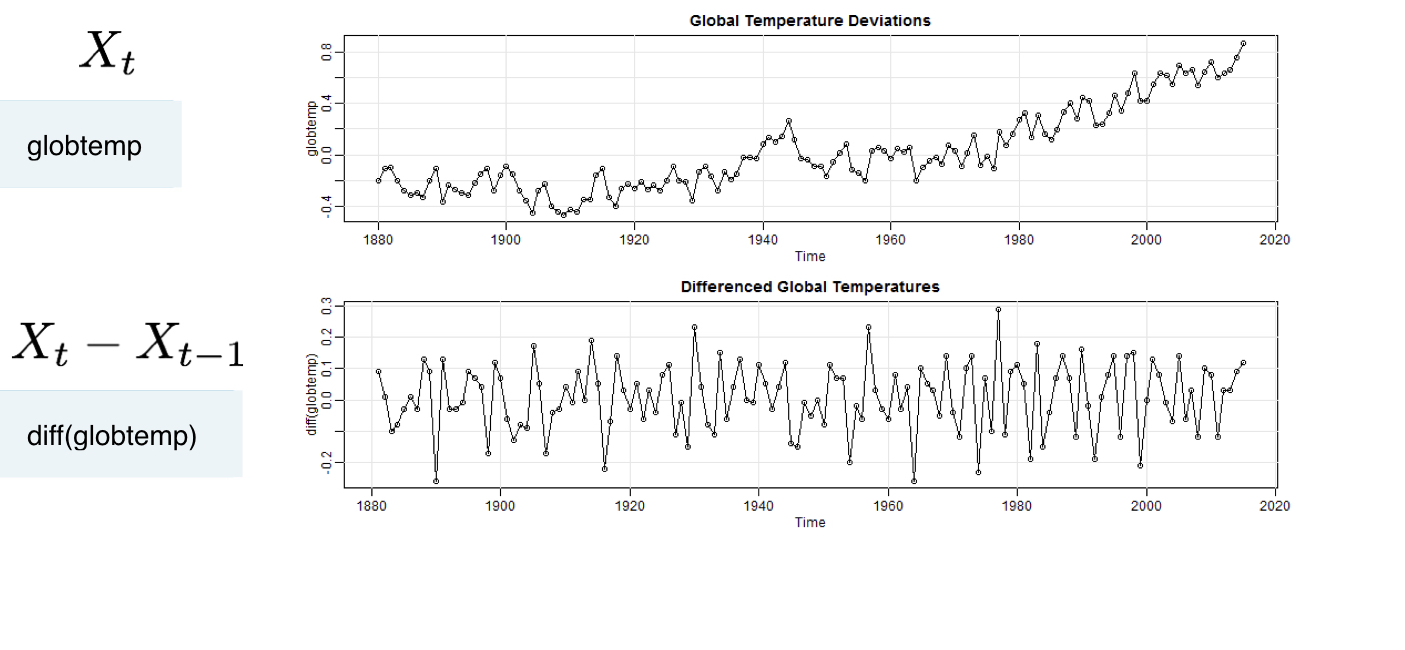

Random Walk Trend

Not stationary, but differenced data are stationary.

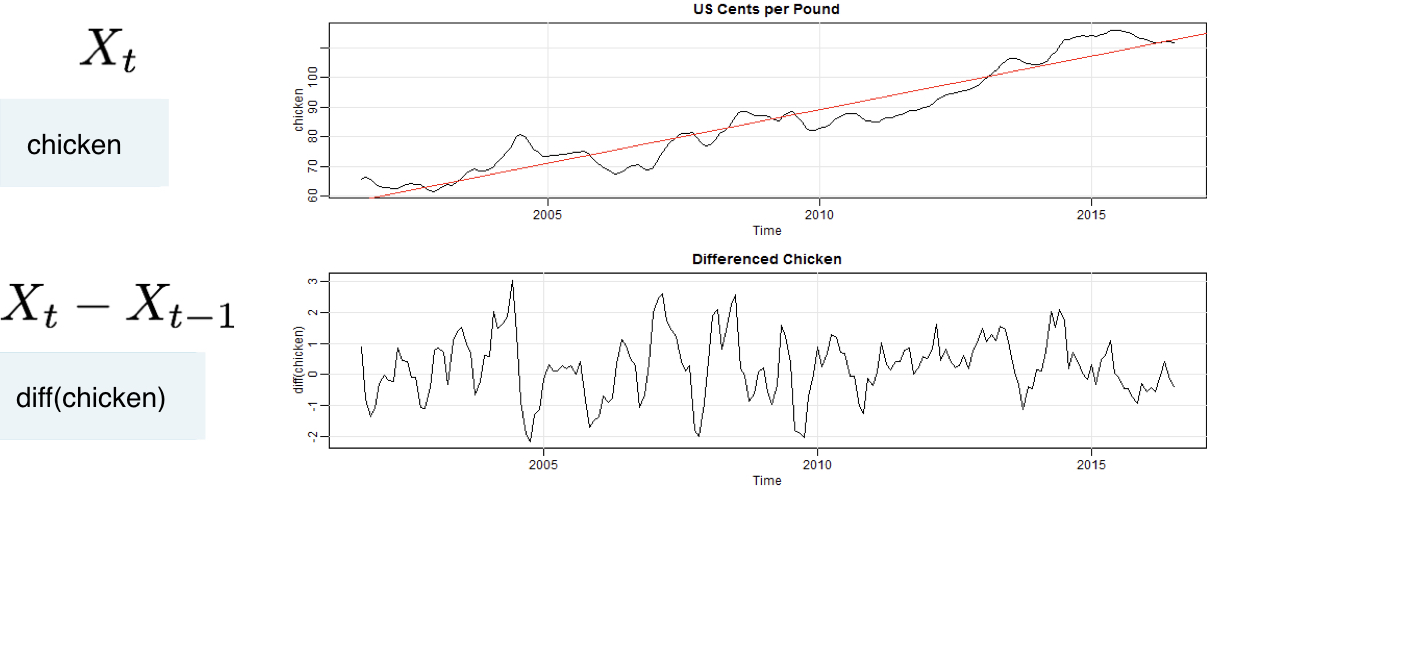

Trend Stationarity

Stationarity around a trend, differencing still works!

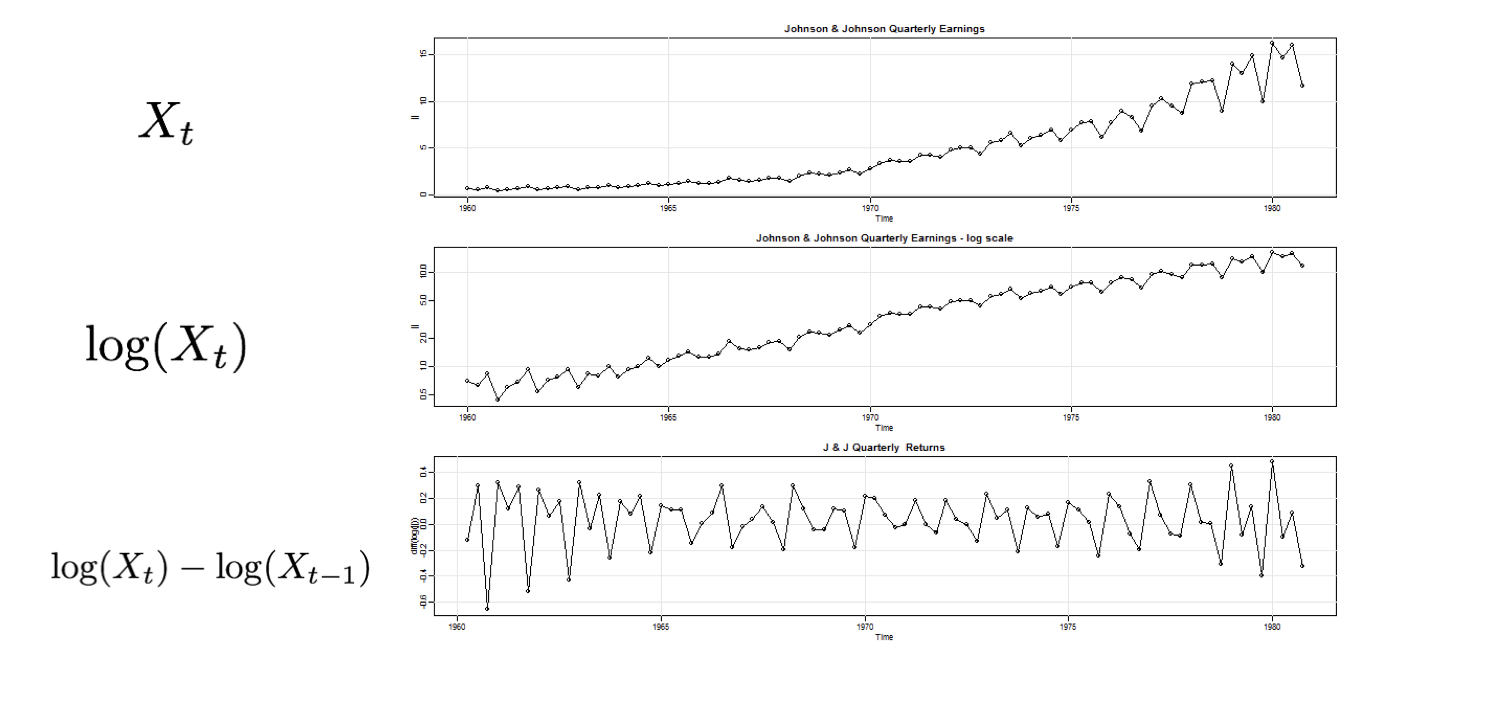

Nonstationarity in trend and variability

First log, then difference