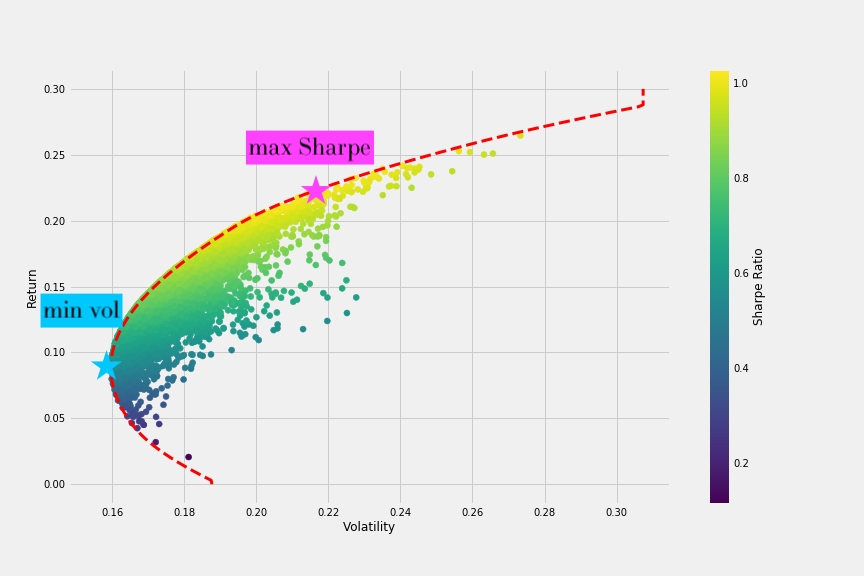

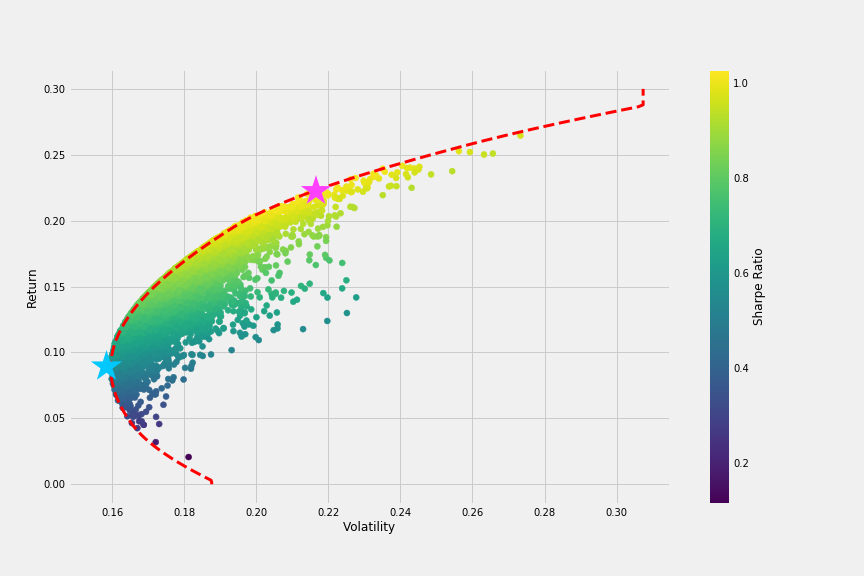

Maximum Sharpe vs. minimum volatility

Introduction to Portfolio Analysis in Python

Charlotte Werger

Data Scientist

Remember the Efficient Frontier?

$$

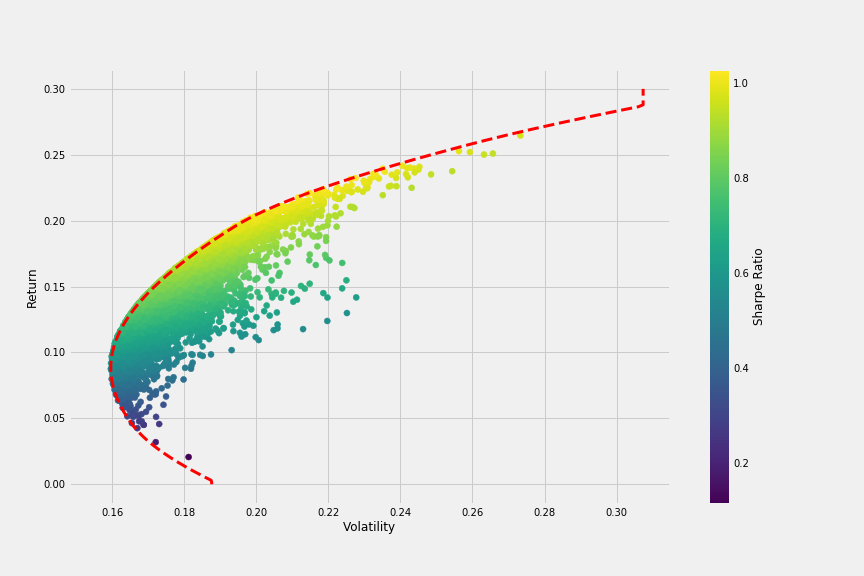

Adjusting PyPortfolioOpt optimization

Let's have another look at the Efficient Frontier

Maximum Sharpe versus Minimum Volatility