Measuring risk of a portfolio

Introduction to Portfolio Analysis in Python

Charlotte Werger

Data Scientist

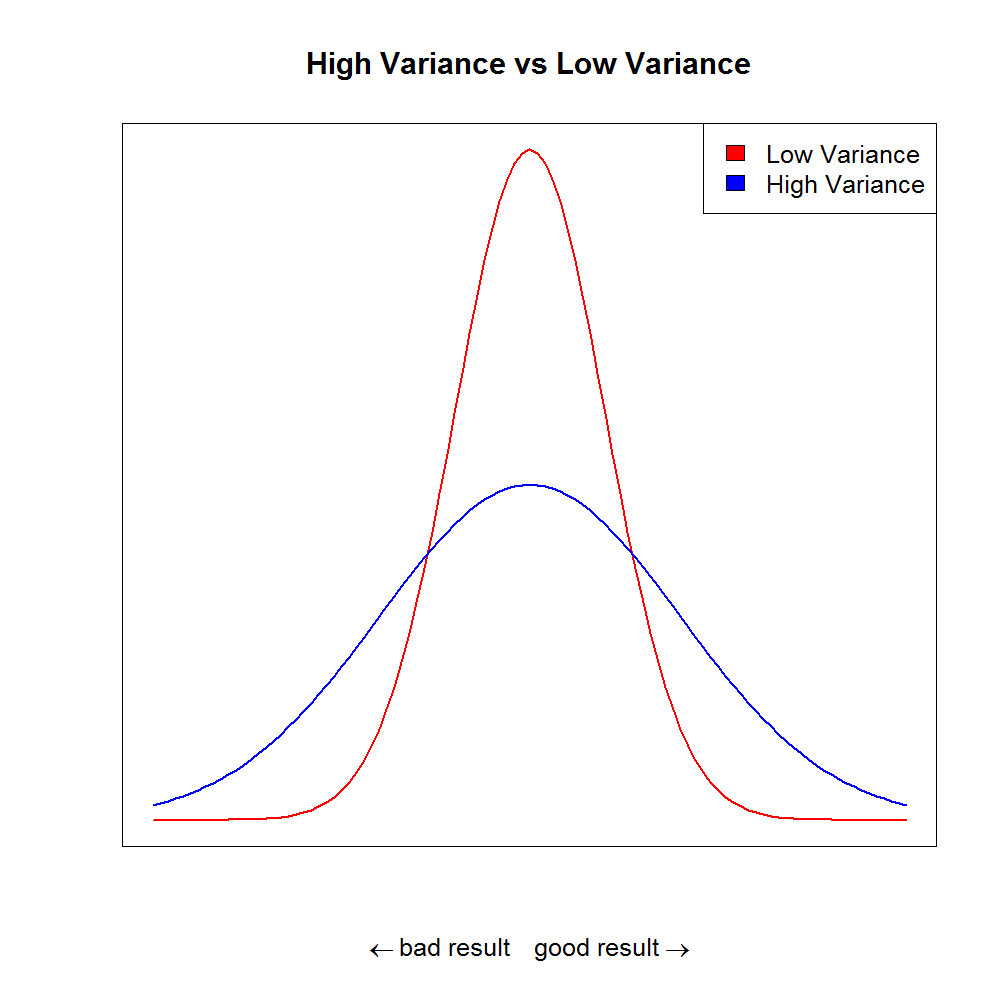

Risk of a portfolio

- Investing is risky: individual assets will go up or down

- Expected return is a random variable

- Returns spread around the mean is measured by the variance $\sigma^2$ and is a common measure of volatility

- $\sigma^2 = \frac{\sum\limits_{i=1}^N (X -\mu)^2}{N}$

Variance

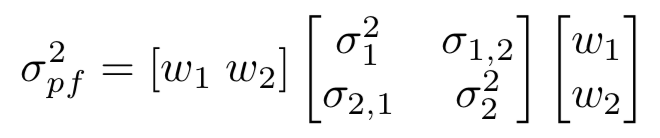

Calculating portfolio variance

$$

- $\rho_{1,2} \sigma_1 \sigma_2$ is called the covariance between asset 1 and 2

- The covariance can also be written as $ \sigma_{1,2} $

- This let's us write:

Re-writing the portfolio variance shorter

- This can be re-written in matrix notation, which you can use more easily in code:

In words, what we need to calculate in python is:

Portfolio variance = Weights transposed x (Covariance matrix x Weights)