Alternative portfolio optimization

Introduction to Portfolio Analysis in Python

Charlotte Werger

Data Scientist

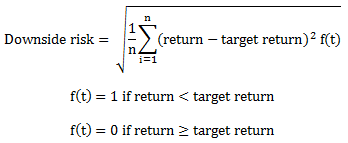

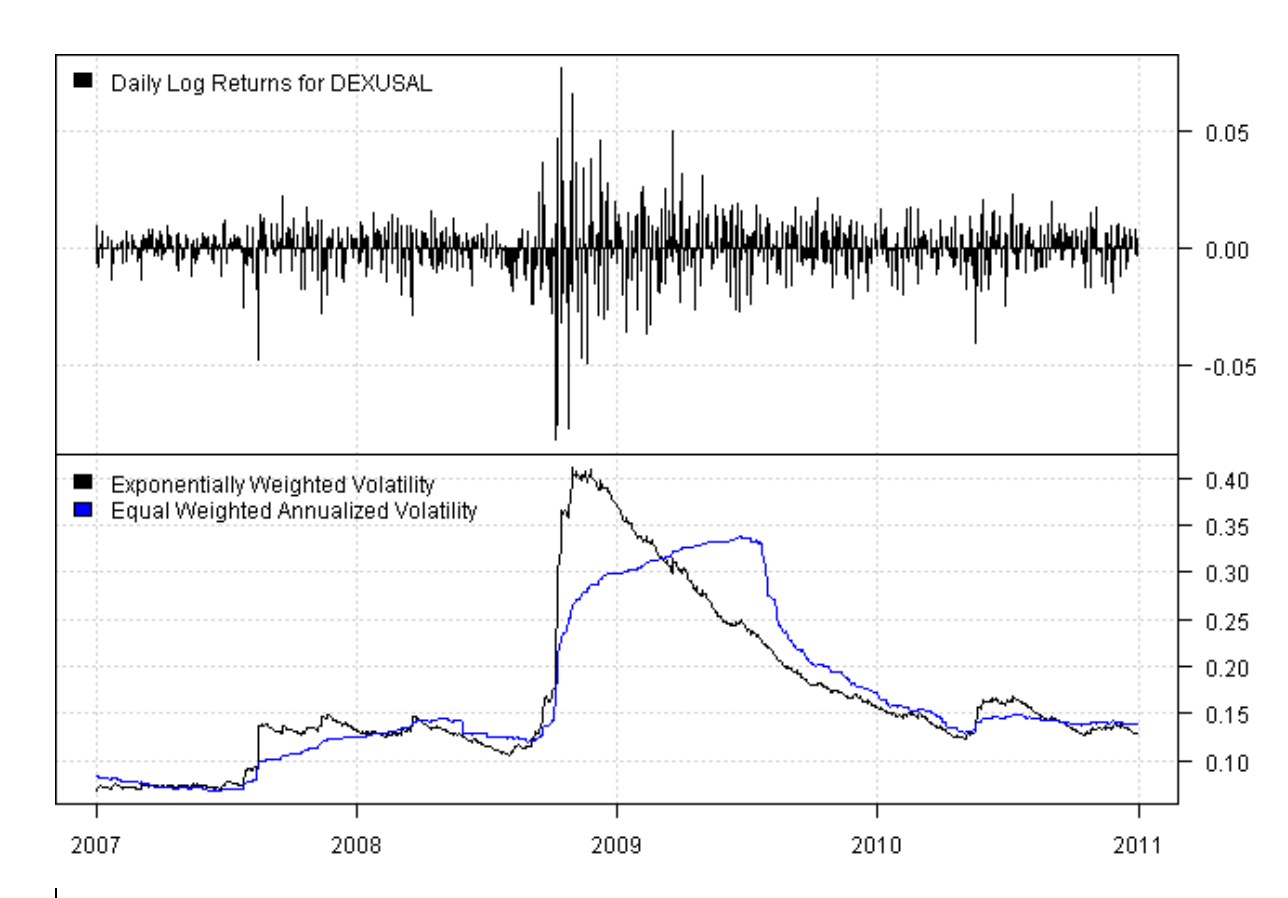

Expected risk and return based on historic data

$$

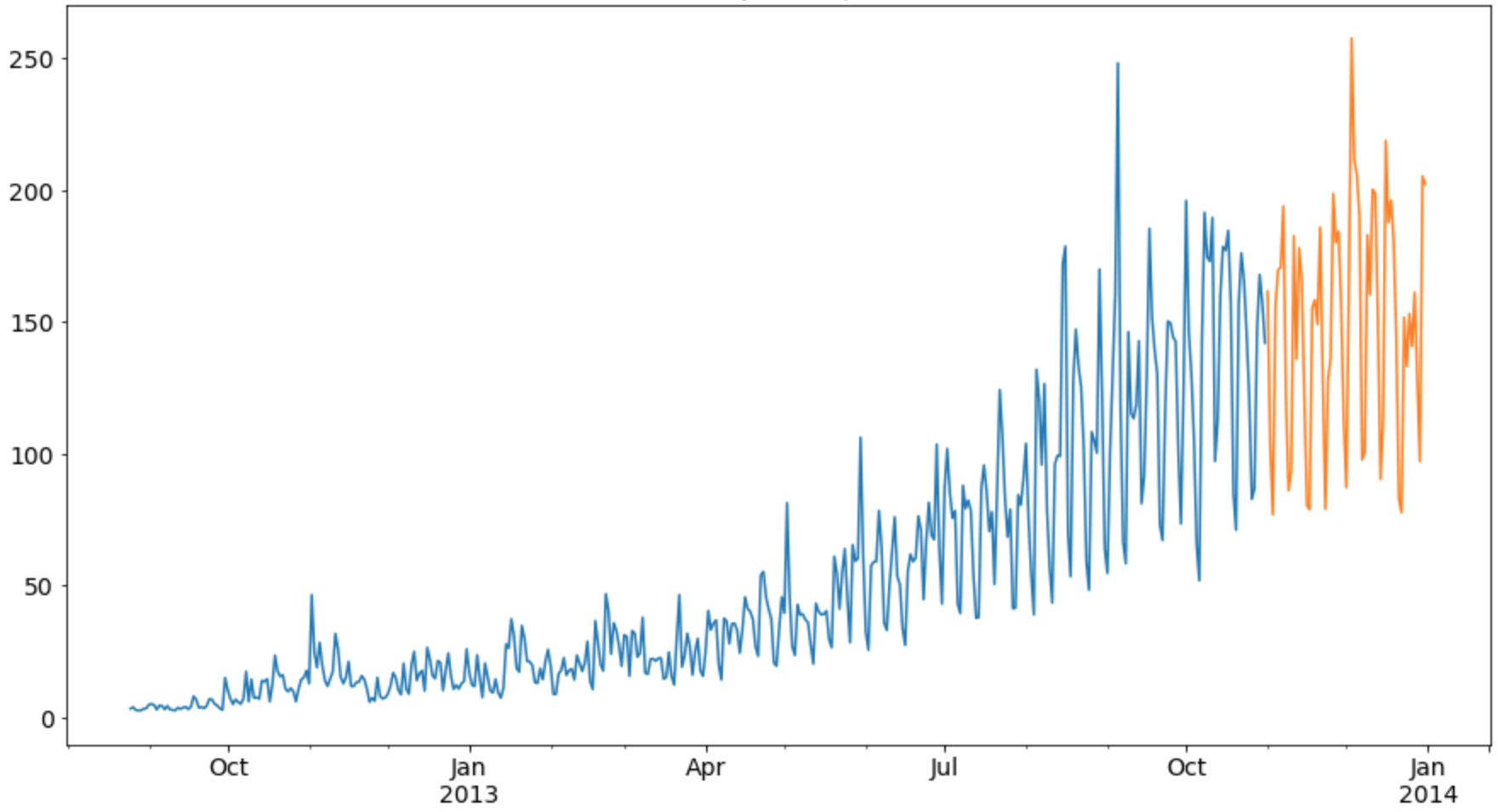

Historic data

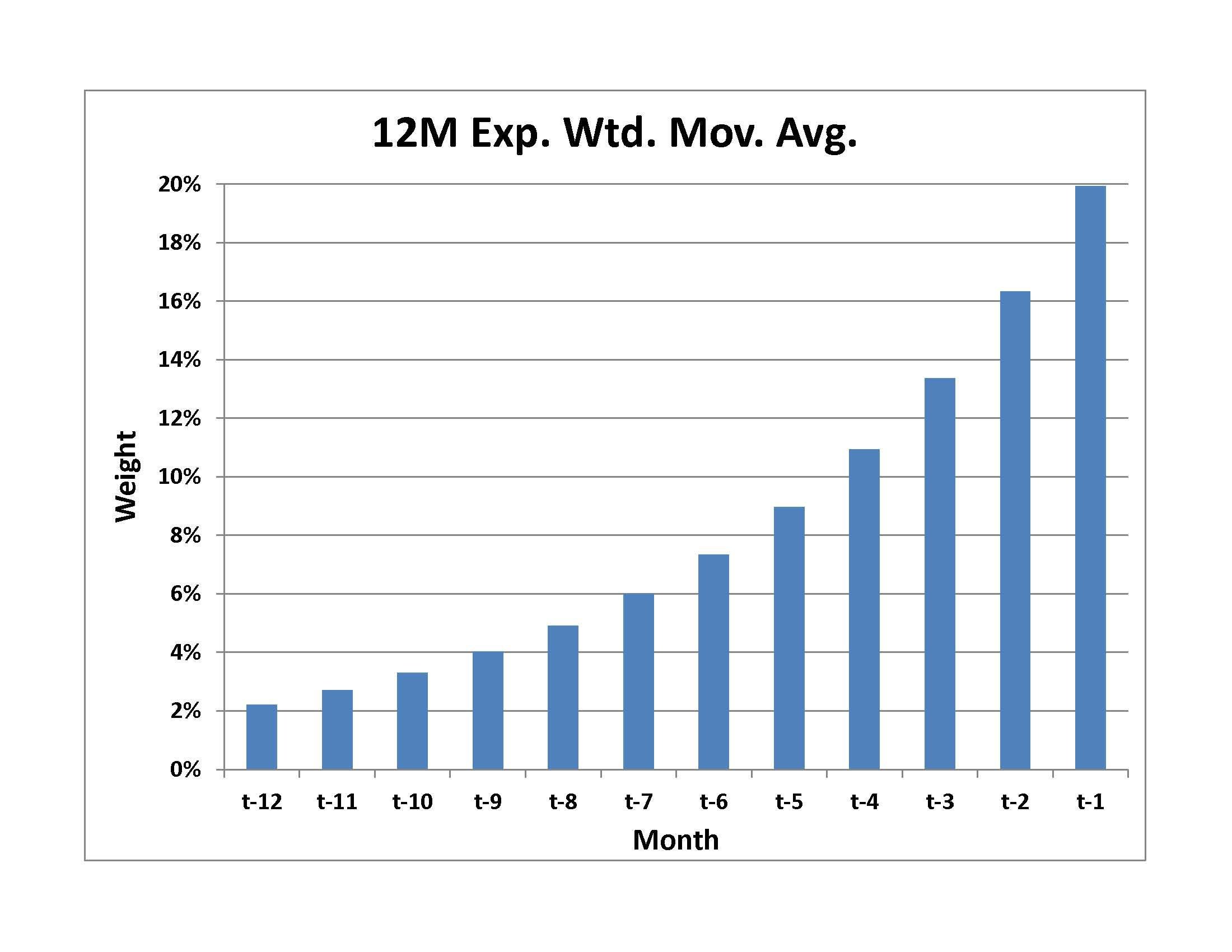

Exponentially weighted returns

Exponentially weighted covariance

$$

1 Source: https://systematicinvestor.github.io/Exponentially-Weighted-Volatility-RCPP

Using downside risk in the optimization

$ $

- Remember the Sortino ratio: it uses the variance of negative returns only

- PyPortfolioOpt allows you to use semicovariance in the optimization, this is a measure for downside risk:

$ $