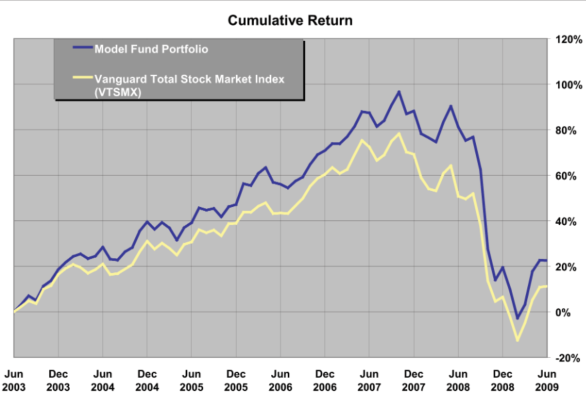

Comparing against a benchmark

Introduction to Portfolio Analysis in Python

Charlotte Werger

Data Scientist

Active investing against a benchmark

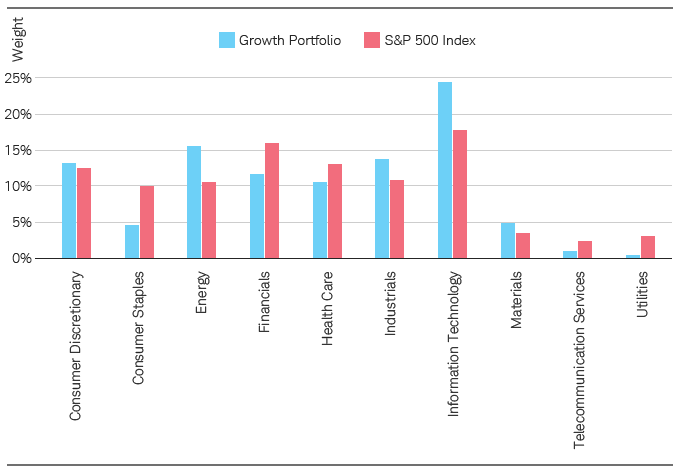

Active weights

1 Source: Schwab Center for Financial Research.

Introduction to Portfolio Analysis in Python

Charlotte Werger

Data Scientist