Factor models

Introduction to Portfolio Analysis in Python

Charlotte Werger

Data Scientist

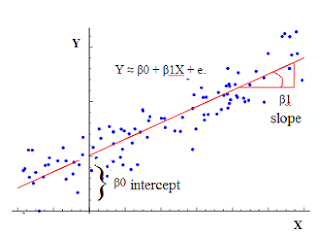

Regression model refresher

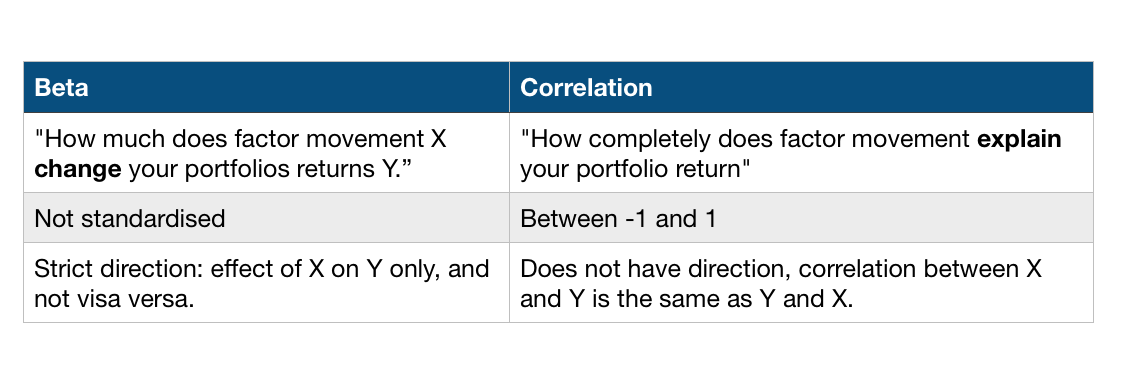

Difference between beta and correlation

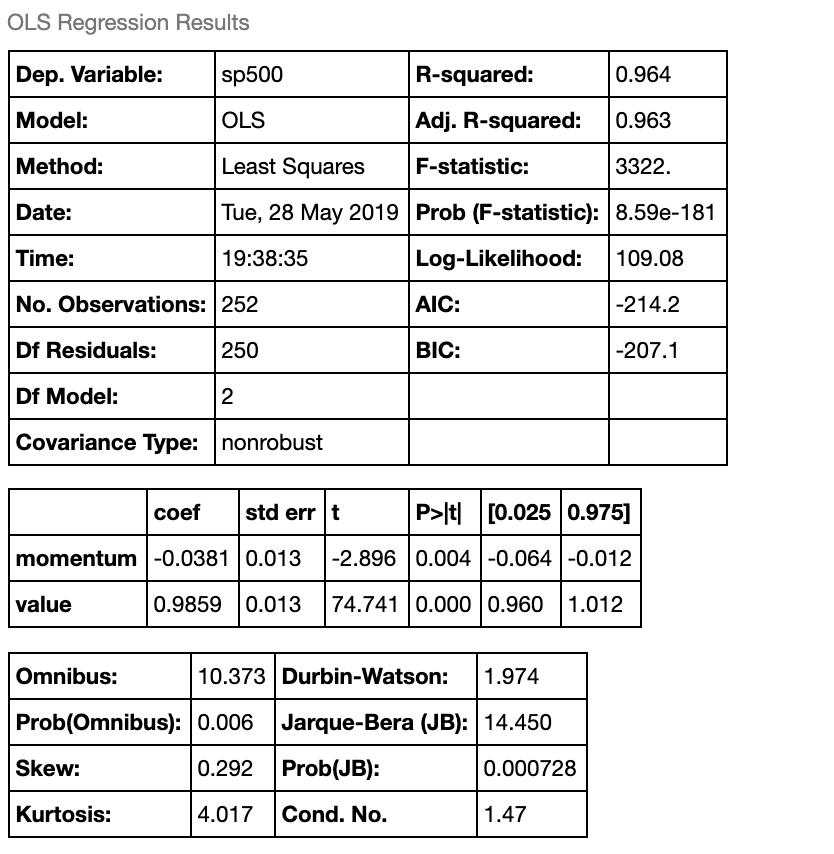

The regression summary output

# Print out the summary statistics

model.summary()

Introduction to Portfolio Analysis in Python

Charlotte Werger

Data Scientist

# Print out the summary statistics

model.summary()