Modern portfolio theory

Introduction to Portfolio Analysis in Python

Charlotte Werger

Data Scientist

Creating optimal portfolios

What is Portfolio Optimization?

Meet Harry Markowitz

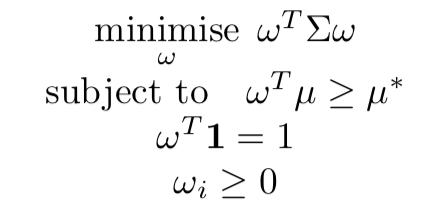

The optimization problem: finding optimal weights

$$

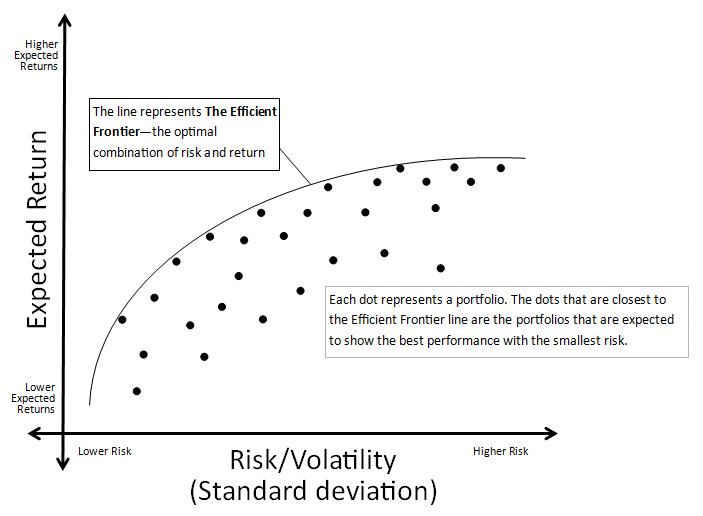

Varying target returns leads to the Efficient Frontier