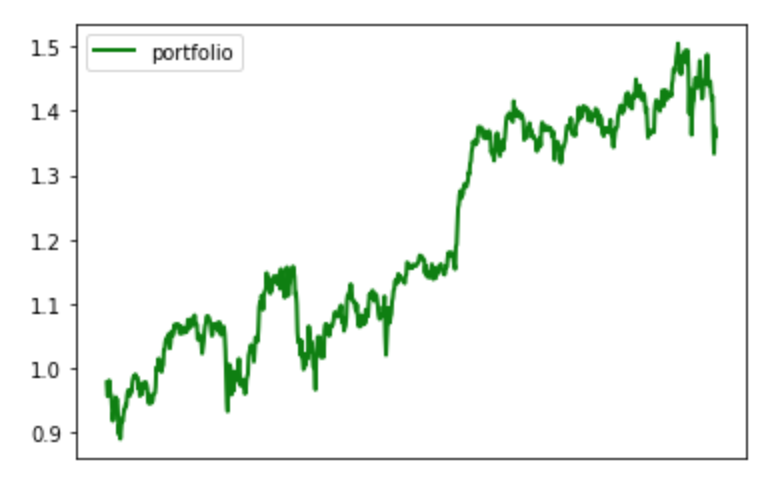

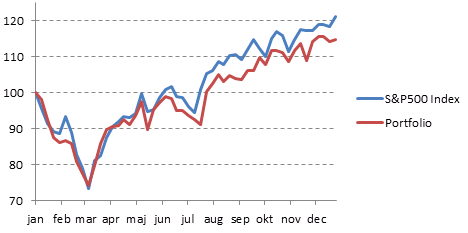

Portfolio returns

Introduction to Portfolio Analysis in Python

Charlotte Werger

Data Scientist

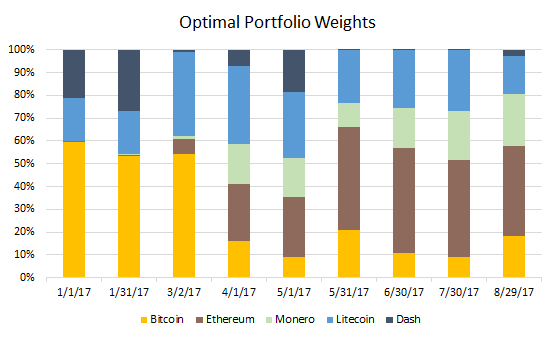

What are portfolio weights?

- Weight is the percentage composition of a particular asset in a portfolio

- All weights together have to sum up to 100%

- Weights and diversification (few large investments versus many small investments)

Calculating portfolio weights

$$

- Calculate by dividing the value of a security by total value of the portfolio

- Equal weighted portfolio, or market cap weighted portfolio

- Weights determine your investment strategy, and can be set to optimize risk and expected return

Portfolio returns

Changes in value over time

$ Return_t = \frac{V_t - V_{t-1}}{V_{t-1}} $

Cumulative return plot