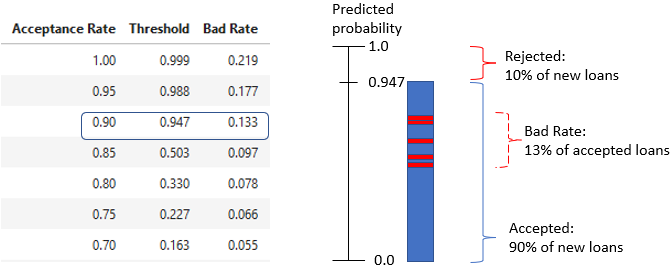

Credit strategy and minimum expected loss

Credit Risk Modeling in Python

Michael Crabtree

Data Scientist, Ford Motor Company

Strategy table interpretation

strat_df = pd.DataFrame(zip(accept_rates, thresholds, bad_rates),

columns = ['Acceptance Rate','Threshold','Bad Rate'])

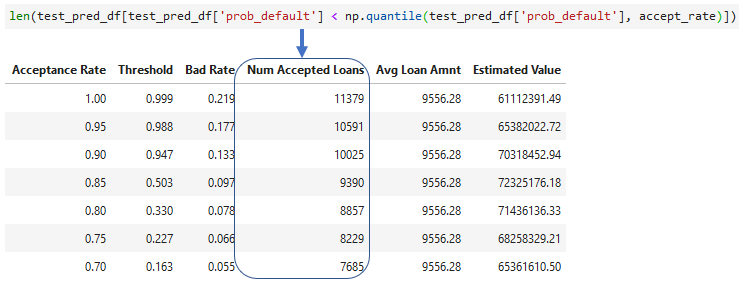

Adding accepted loans

- The number of loans accepted for each acceptance rate

- Can use

len()or.count()

- Can use

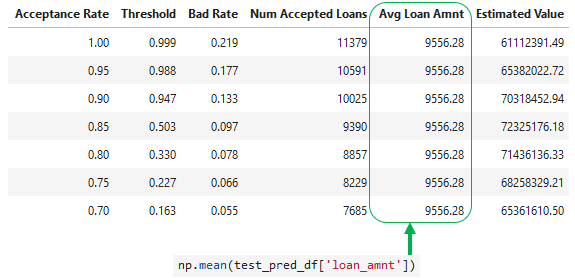

Adding average loan amount

- Average

loan_amntfrom the test set data

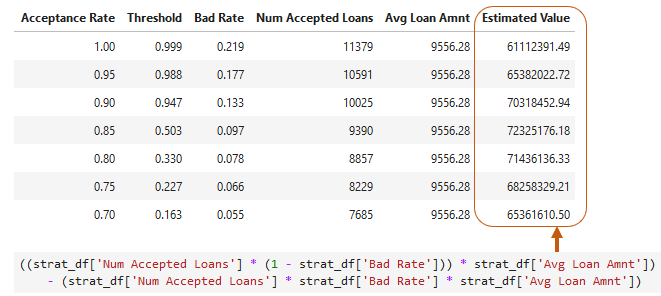

Estimating portfolio value

- Average value of accepted loan non-defaults minus average value of accepted defaults

- Assumes each default is a loss of the

loan_amnt

Total expected loss

- How much we expect to lose on the defaults in our portfolio

# Probability of default (PD)

test_pred_df['prob_default']

# Exposure at default = loan amount (EAD)

test_pred_df['loan_amnt']

# Loss given default = 1.0 for total loss (LGD)

test_pred_df['loss_given_default']