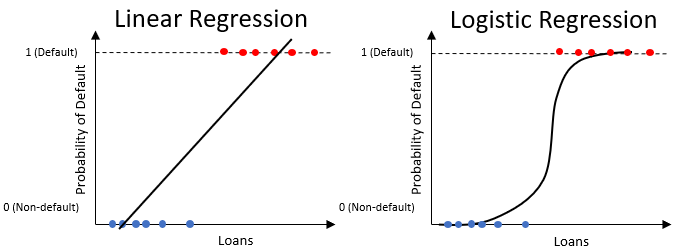

Logistic regression for probability of default

Credit Risk Modeling in Python

Michael Crabtree

Data Scientist, Ford Motor Company

Predicting probabilities

- Probabilities of default as an outcome from machine learning

- Learn from data in columns (features)

- Classification models (default, non-default)

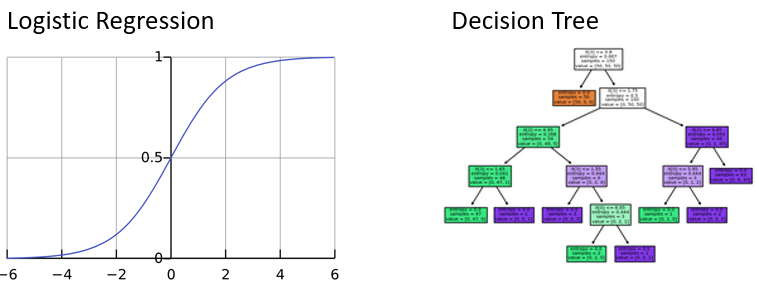

- Two most common models:

- Logistic regression

- Decision tree

Logistic regression

- Similar to the linear regression, but only produces values between

0and1