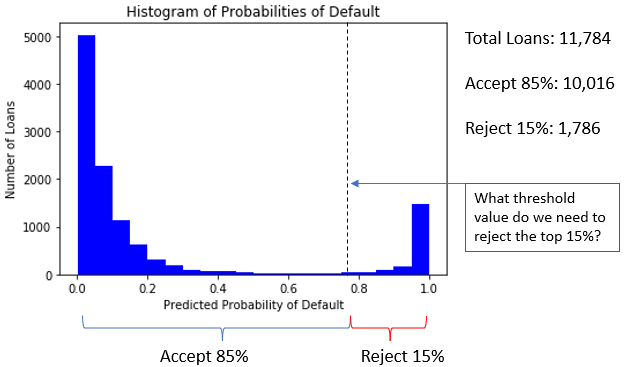

Credit acceptance rates

Credit Risk Modeling in Python

Michael Crabtree

Data Scientist, Ford Motor Company

Understanding acceptance rate

- Example: Accept 85% of loans with the lowest

prob_default

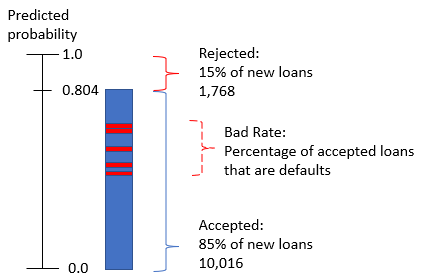

Bad Rate

- Even with a calculated threshold, some of the accepted loans will be defaults

- These are loans with

prob_defaultvalues around where our model is not well calibrated

Bad rate calculation

#Calculate the bad rate

np.sum(accepted_loans['true_loan_status']) / accepted_loans['true_loan_status'].count()

- If non-default is

0, and default is1then thesum()is the count of defaults - The

.count()of a single column is the same as the row count for the data frame