Parametric Estimation

Quantitative Risk Management in Python

Jamsheed Shorish

Computational Economist

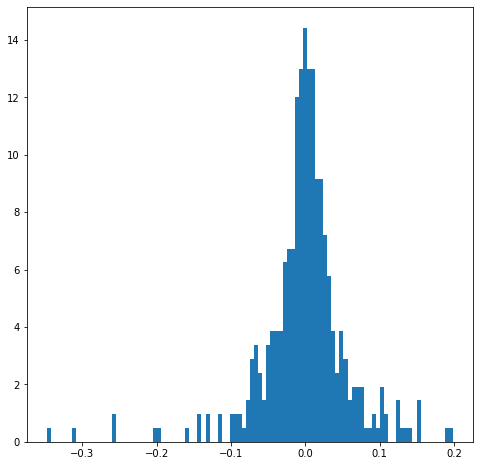

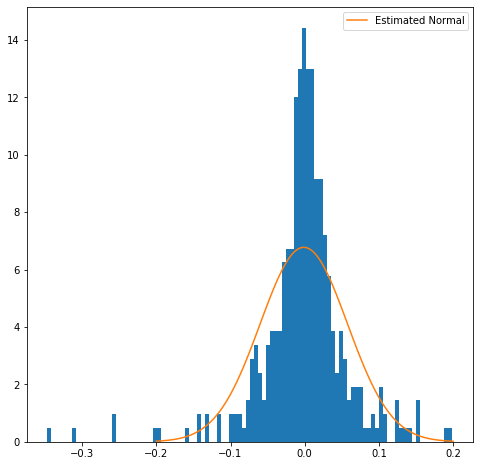

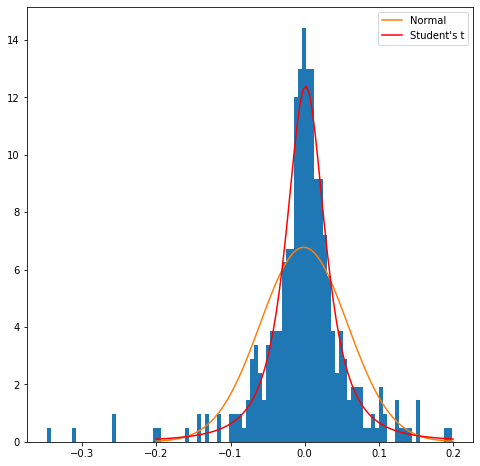

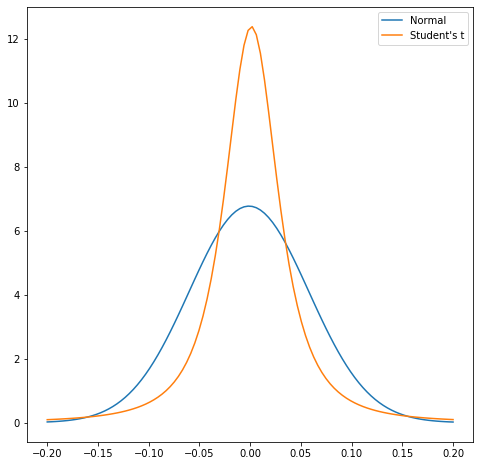

Goodness of fit

Goodness of fit

Goodness of fit

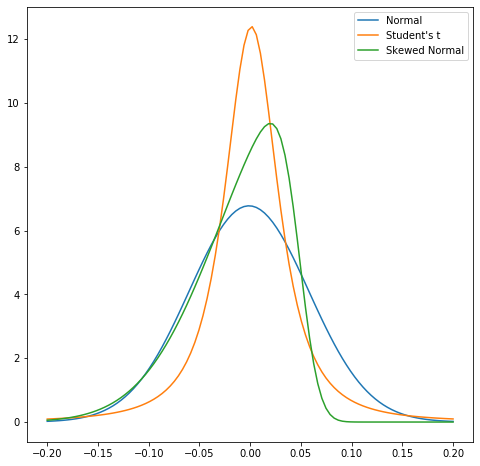

Skewness

Skewness

Skewness

Quantitative Risk Management in Python

Jamsheed Shorish

Computational Economist