Measuring Risk

Quantitative Risk Management in Python

Jamsheed Shorish

CEO, Shorish Research

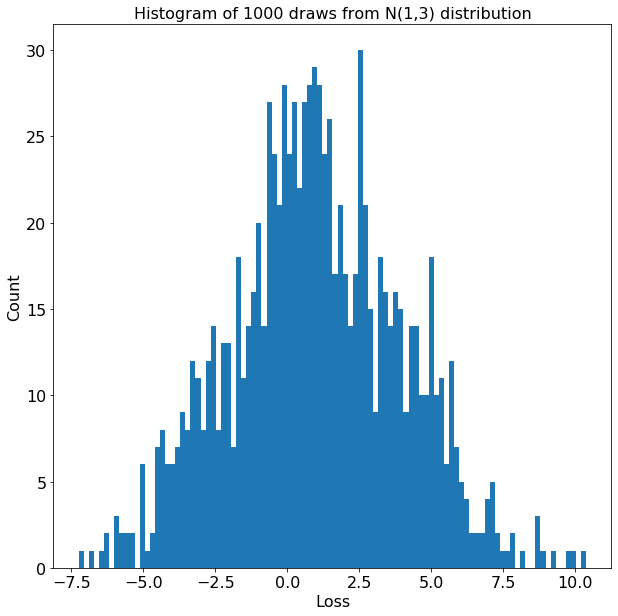

The Loss Distribution

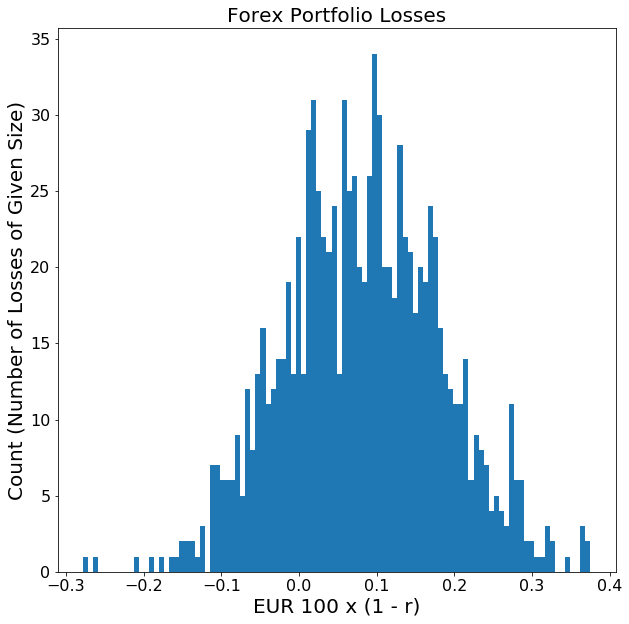

- Forex Example:

- Portfolio value in U.S. dollars is USD 100

- Risk factor =

/

/  exchange rate

exchange rate - Portfolio value in EURO if 1 = 1 : USD 100 x EUR 1 / USD 1 = EUR 100.

- Portfolio value in EURO if r = 1 : = USD 100 x EUR r / 1 USD = EUR 100 x r

- Loss = EUR 100 - EUR 100 x r = EUR 100 x (1 - r)

- Loss distribution: Random realizations of r => distribution of portfolio losses in the future

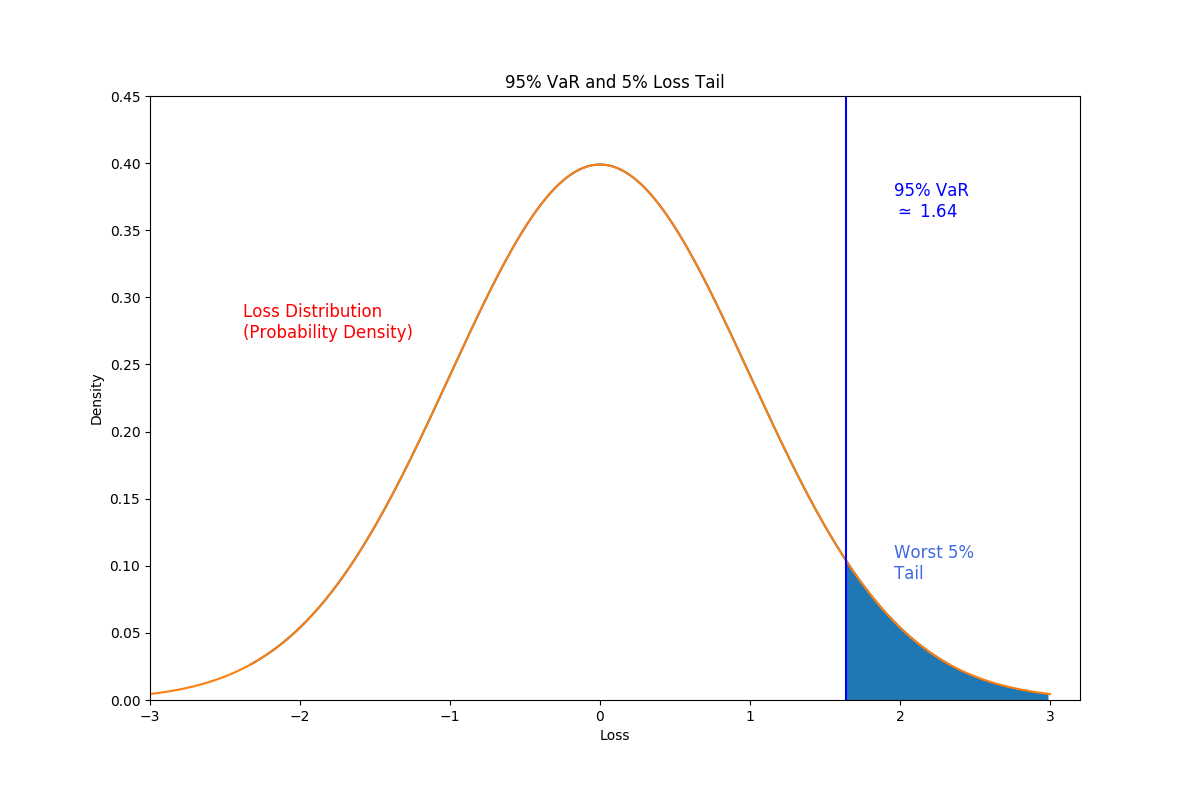

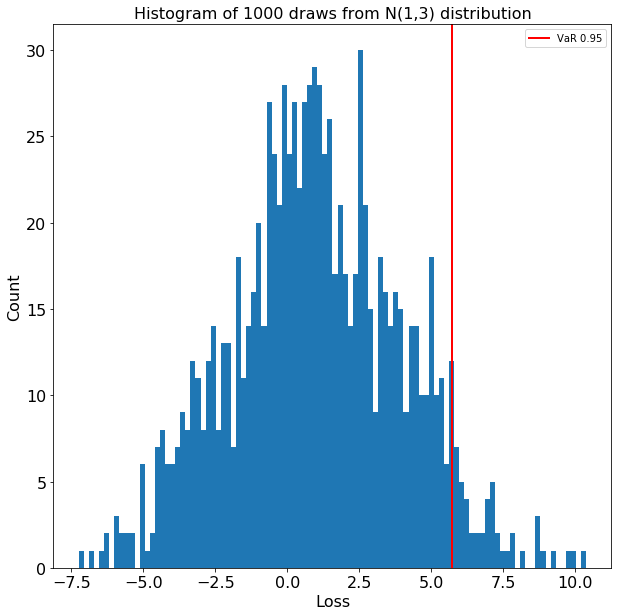

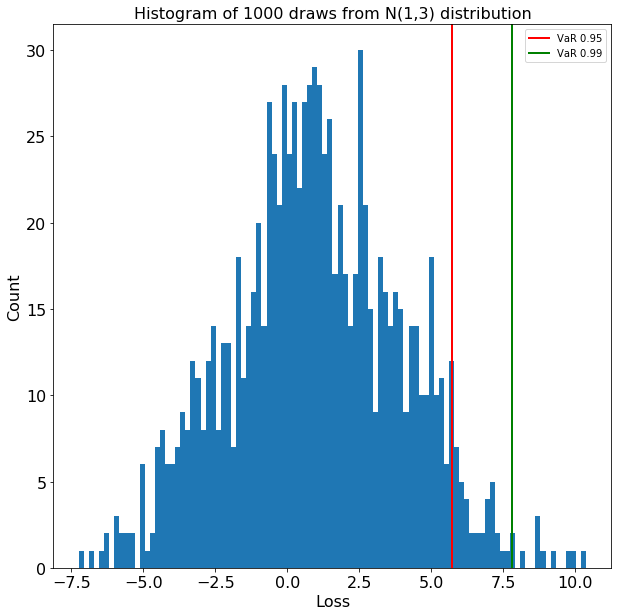

Value at Risk (VaR)

Conditional Value at Risk (CVaR)

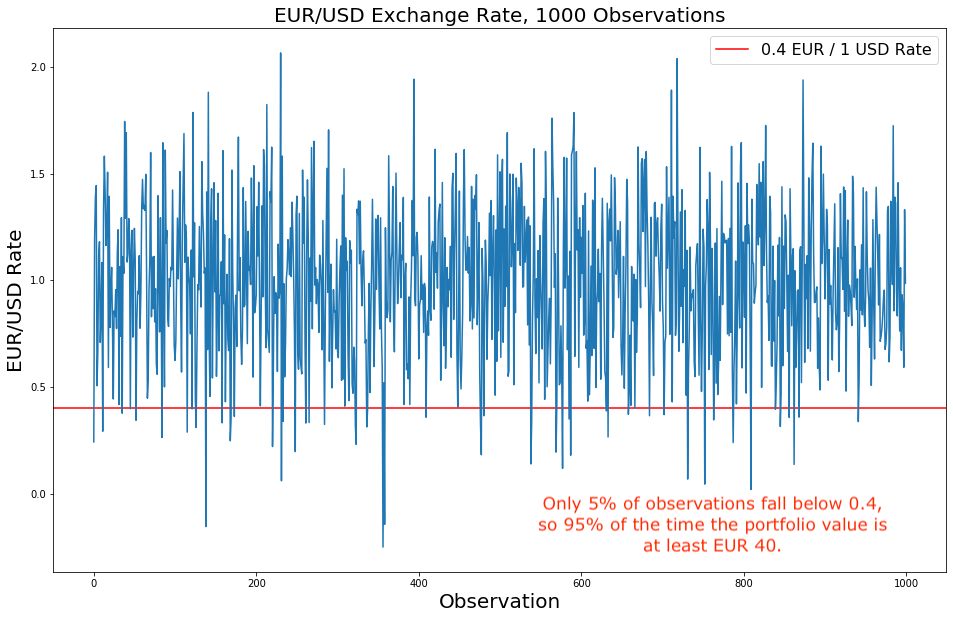

- Forex Example:

- 95% CVaR = expected loss for 5% of cases when portfolio value smaller than EUR 40

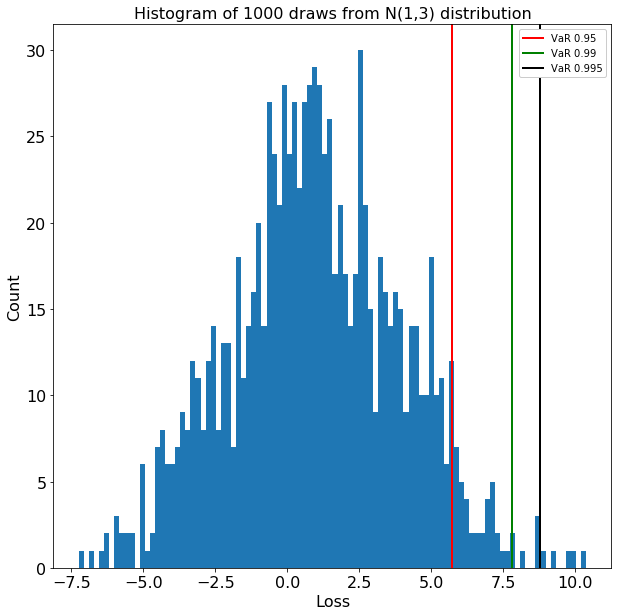

Visualizing the VaR

Visualizing the VaR

Visualizing the VaR

Visualizing the VaR