How to implement GARCH models in Python

GARCH Models in Python

Chelsea Yang

Data Science Instructor

Python "arch" package

1 Kevin Sheppard. (2019, March 28). bashtage/arch: Release 4.8.1 (Version 4.8.1). Zenodo. http://doi.org/10.5281/zenodo.2613877

Model fitting

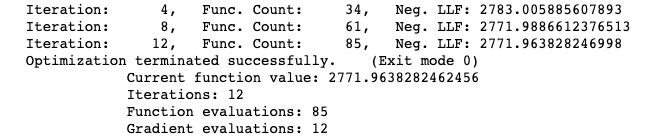

Display model fitting output after every n iterations:

gm_result = gm_model.fit(update_freq = 4)

Turn off the display:

gm_result = gm_model.fit(disp = 'off')

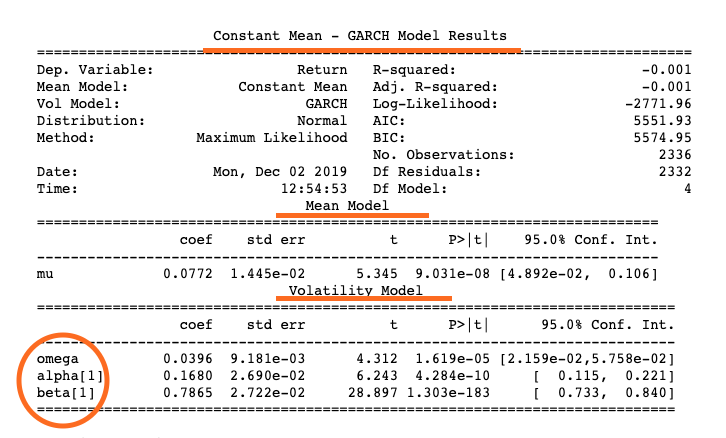

Fitted results: summary

print(gm_result.summary())

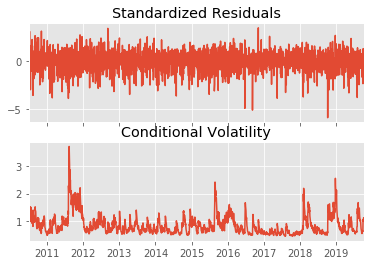

Fitted results: plots

gm_result.plot()