Distribution assumptions

GARCH Models in Python

Chelsea Yang

Data Science Instructor

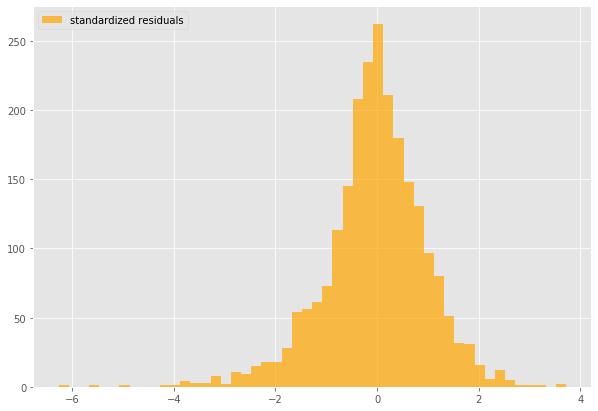

Residuals in GARCH

gm_std_resid = gm_result.resid / gm_result.conditional_volatility

plt.hist(gm_std_resid, facecolor = 'orange',label = 'standardized residuals')

Fat tails

- Higher probability to observe large (positive or negative) returns than under a normal distribution

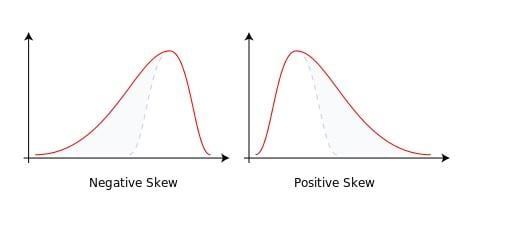

Skewness

- Measure of asymmetry of a probability distribution

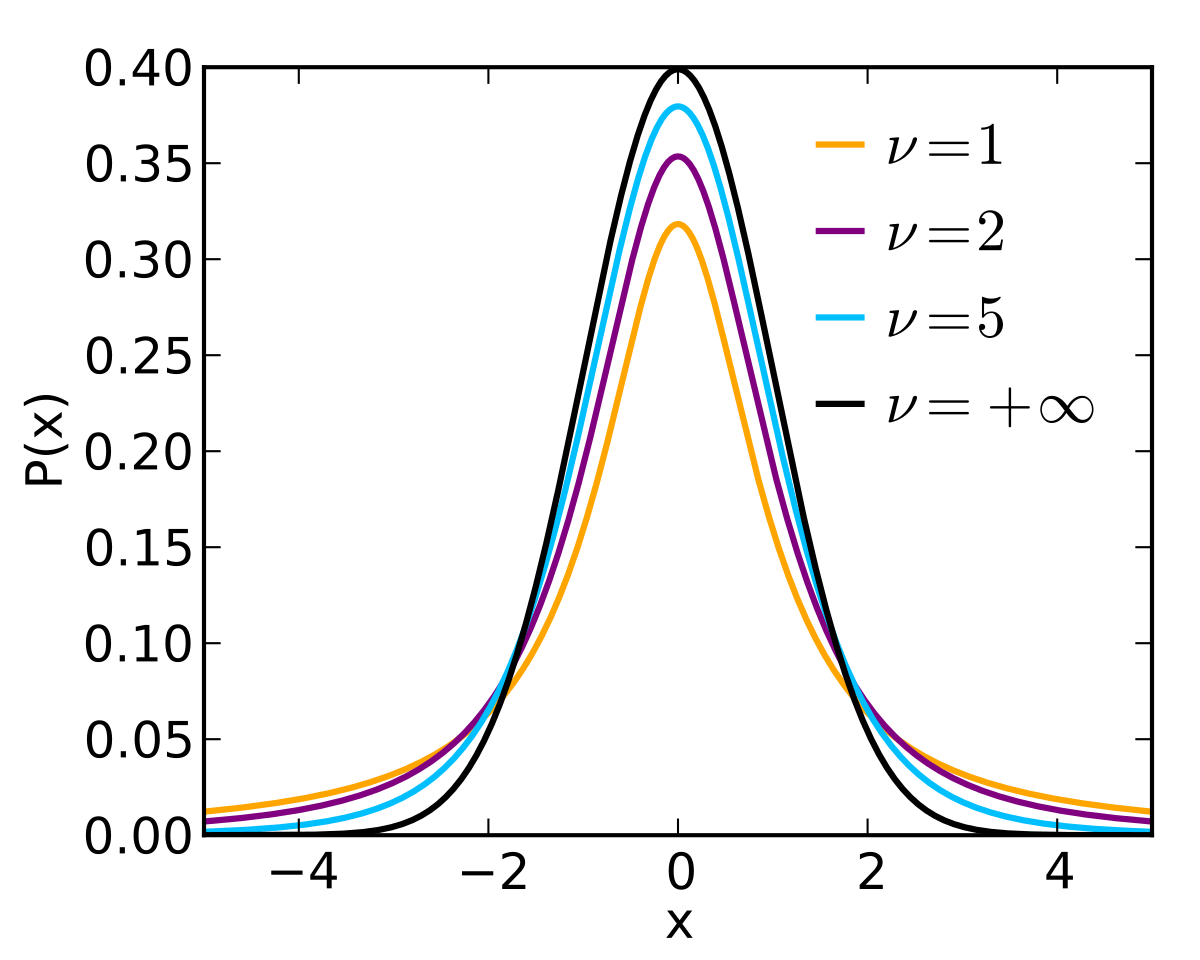

Student's t-distribution

$\nu$ parameter of a Student's t-distribution indicates its shape