What are ARCH and GARCH

GARCH Models in Python

Chelsea Yang

Data Science Instructor

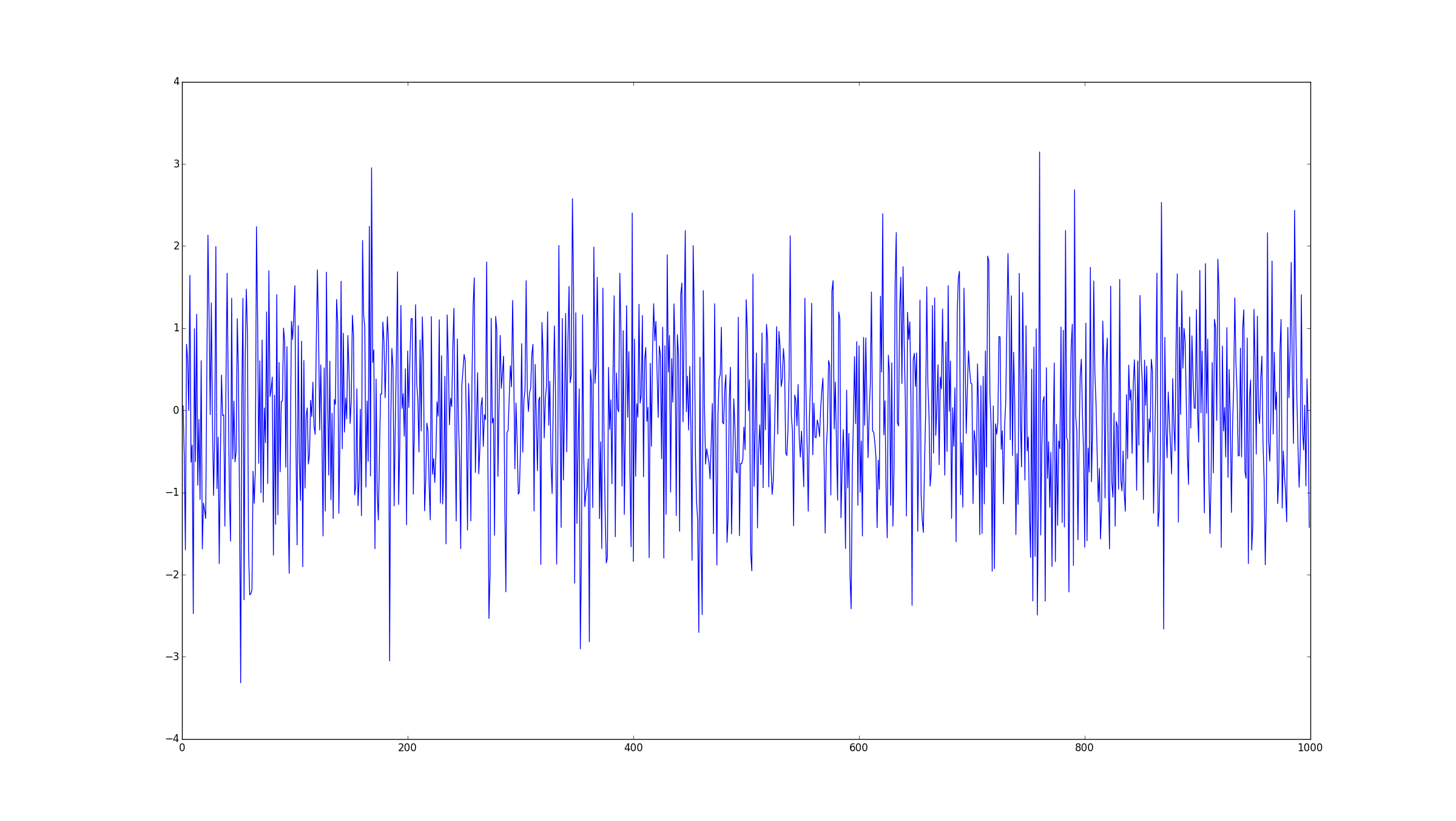

First came the ARCH

Auto Regressive Conditional Heteroskedasticity

Developed by Robert F. Engle (Nobel prize laureate 2003)

Then came the GARCH

"Generalized" ARCH

Developed by Tim Bollerslev (Robert F. Engle's student)

Related statistical terms

White noise (z): Uncorrelated random variables with a zero mean and a finite variance

Residual = predicted value - observed value

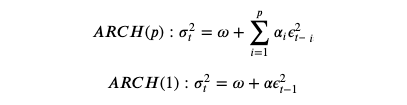

Model equations: ARCH

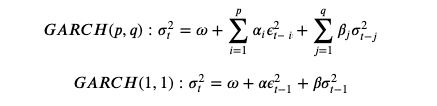

Model equations: GARCH

Model intuition

Autoregressive: predict future behavior based on past behavior

Volatility as a weighted average of past information