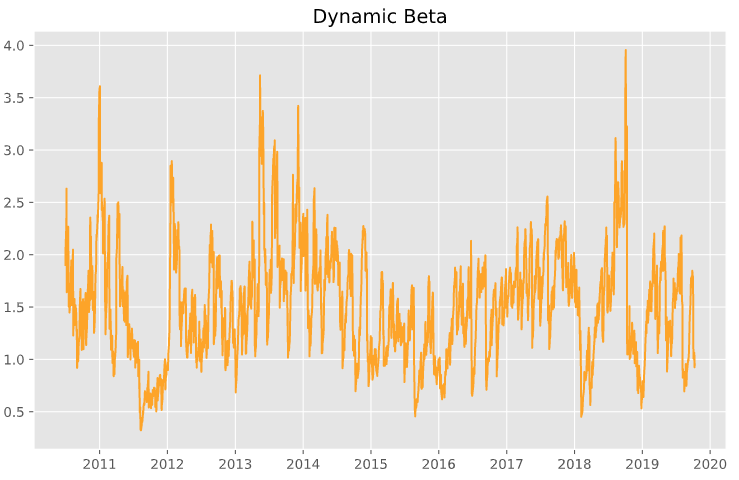

Dynamic Beta in portfolio management

GARCH Models in Python

Chelsea Yang

Data Science Instructor

Dynamic Beta with GARCH

$Beta$ = $\rho$ * $\sigma$_stock / $\sigma$__market

GARCH Models in Python

Chelsea Yang

Data Science Instructor

$Beta$ = $\rho$ * $\sigma$_stock / $\sigma$__market