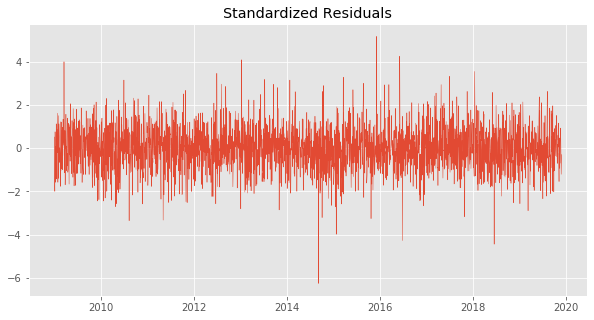

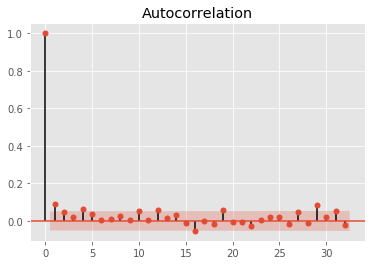

Validation of GARCH model assumptions

GARCH Models in Python

Chelsea Yang

Data Science Instructor

Visual check

ACF plot

- ACF: AutoCorrelation Function

- ACF Plot: visual representation of the autocorrelation by lags

Red area in the plot indicates the confidence level (alpha = 5%)