Dynamic covariance in portfolio optimization

GARCH Models in Python

Chelsea Yang

Data Science Instructor

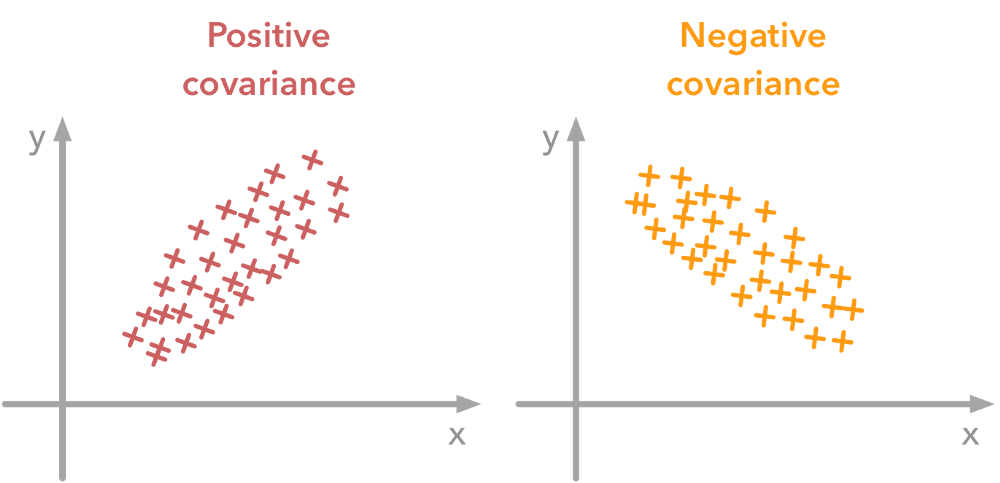

What is covariance

- Describe the relationship between movement of two variables

- Positive covariance: move together

- Negative covariance; move in the opposite directions