Why do we need GARCH models

GARCH Models in Python

Chelsea Yang

Data Science Instructor

What is volatility

- Describe the dispersion of financial asset returns over time

- Often computed as the standard deviation or variance of price returns

- The higher the volatility, the riskier a financial asset

The challenge of volatility modeling

Heteroskedasticity:

- In ancient Greek: "different" (hetero) + "dispersion" (skedasis)

- A time series demonstrates varying volatility systematically over time

Detect heteroskedasticity

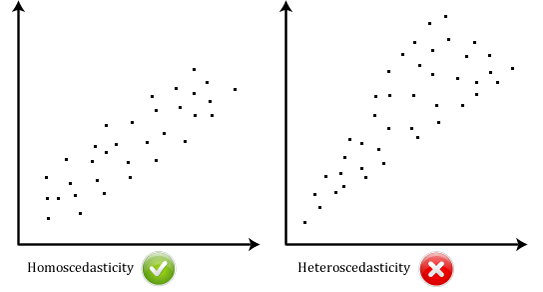

Homoskedasticity vs Heteroskedasticity

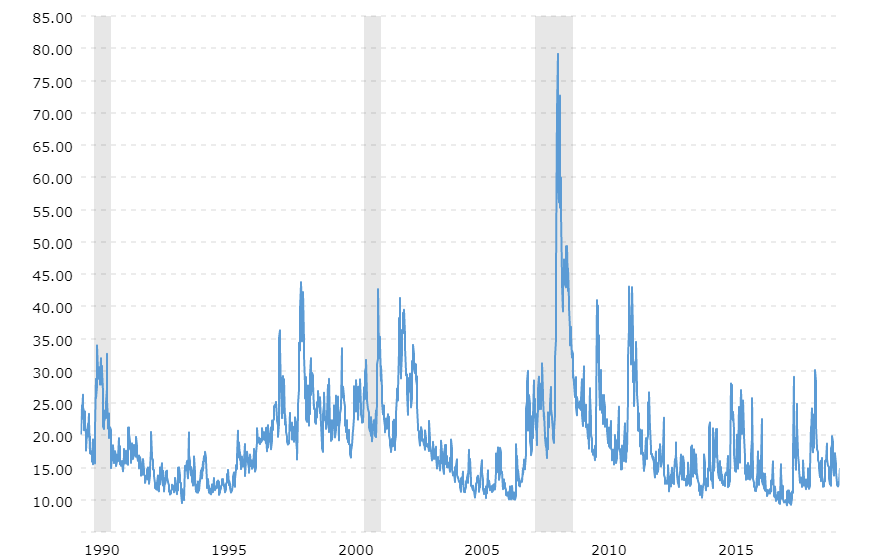

Volatility clustering

VIX historical prices: