GARCH rolling window forecast

GARCH Models in Python

Chelsea Yang

Data Science Instructor

Rolling window for out-of-sample forecast

An exciting part of financial modeling: predict the unknown

Rolling window forecast: repeatedly perform model fitting and forecast as time rolls forward

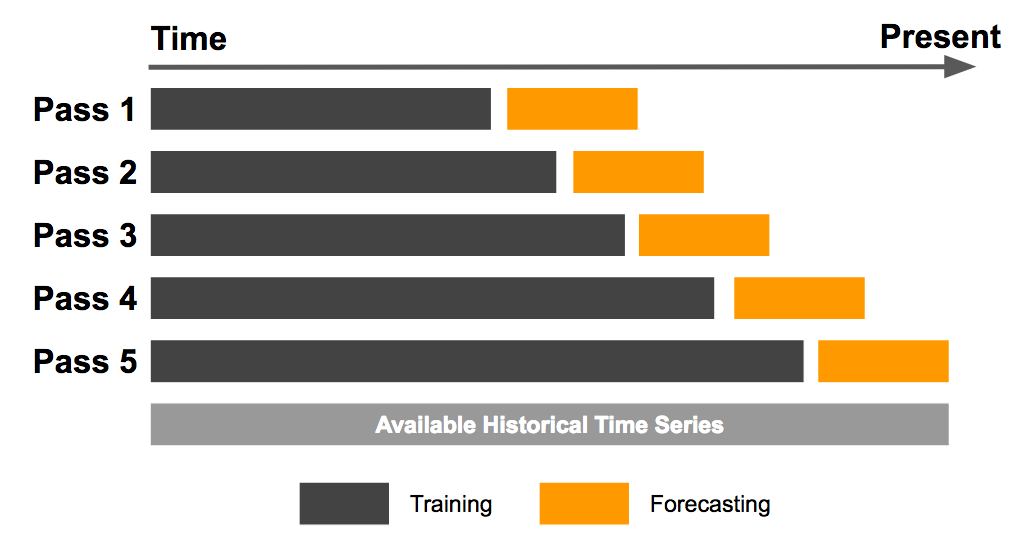

Expanding window forecast

Continuously add new data points to the sample

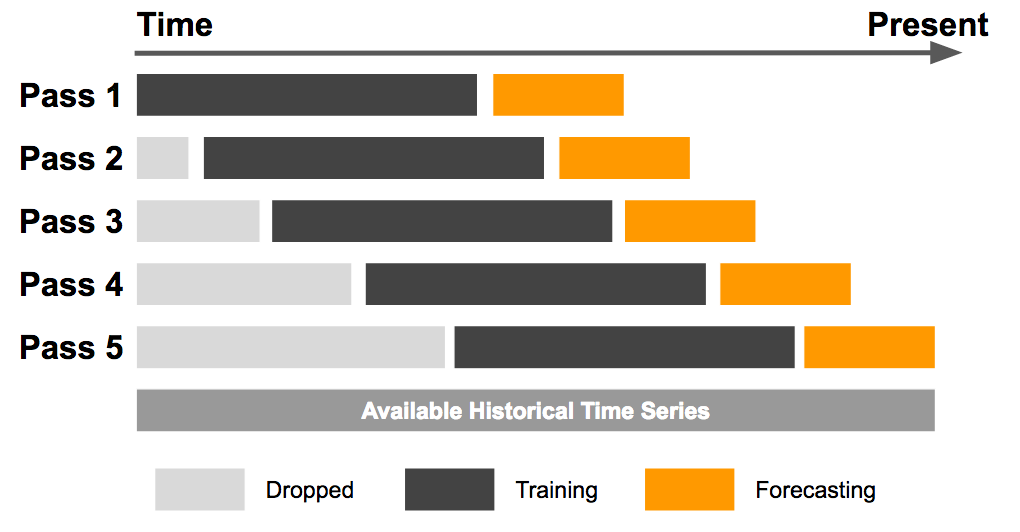

Fixed rolling window forecast

New data points are added while old ones are dropped from the sample

How to determine window size

Usually determined on a case-by-case basis

Too wide window size: include obsolete data that may lead to higher variance

Too narrow window size: exclude relevant data that may lead to higher bias

The optimal window size: trade-off to balance bias and variance