Volatility models for asymmetric shocks

GARCH Models in Python

Chelsea Yang

Data Science Instructor

Asymmetric shocks in financial data

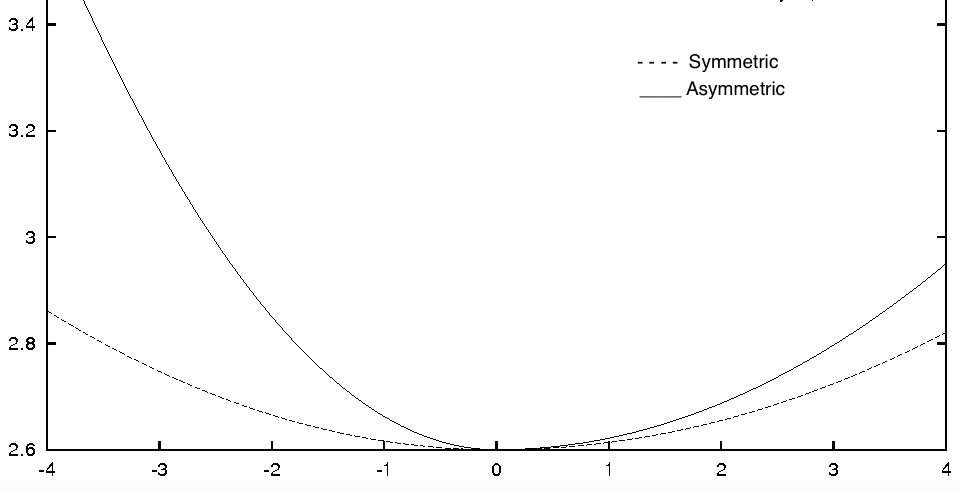

News impact curve:

Leverage effect

Debt-equity Ratio = Debt $/$ Equity

Stock price goes down, debt-equity ratio goes up

Riskier!

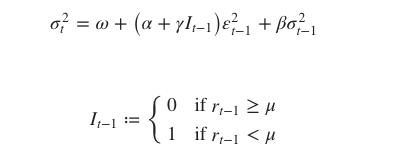

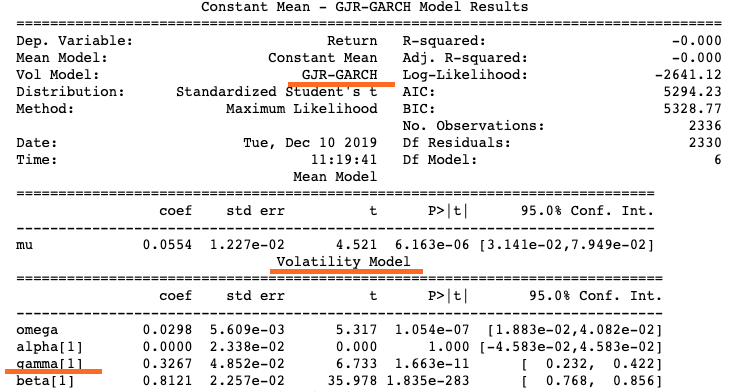

GJR-GARCH

GJR-GARCH in Python

arch_model(my_data, p = 1, q = 1, o = 1,

mean = 'constant', vol = 'GARCH')

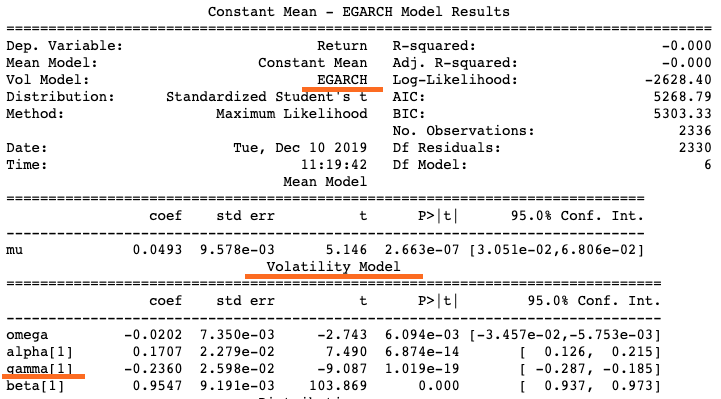

EGARCH in Python

arch_model(my_data, p = 1, q = 1, o = 1,

mean = 'constant', vol = 'EGARCH')

Which model to use

GJR-GARCH or EGARCH?

Which model is better depends on the data