On premium payments and retirement plans

Life Insurance Products Valuation in R

Katrien Antonio, Ph.D.

Professor, KU Leuven and University of Amsterdam

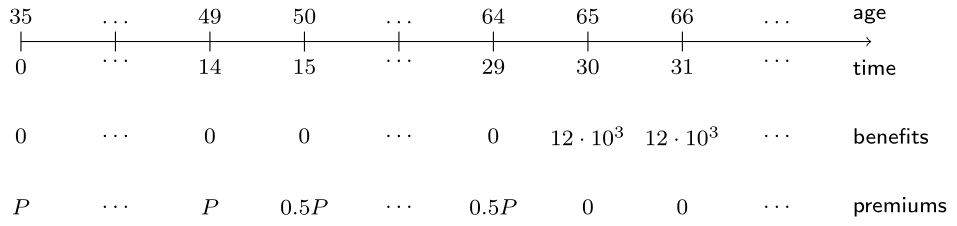

Mrs. Incredible's retirement plan

Mrs. Incredible's retirement plan pictured

Life Insurance Products Valuation in R

Katrien Antonio, Ph.D.

Professor, KU Leuven and University of Amsterdam