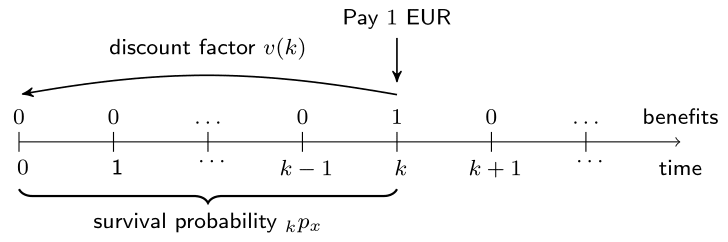

The whole, temporary and deferred life annuity

Life Insurance Products Valuation in R

Katrien Antonio, Ph.D.

Professor, KU Leuven and University of Amsterdam

A series of benefits

- What if?

- The benefit is $c_k$ EUR instead of 1 EUR?

- A series of such pure endowments instead of just one?

Life annuities in R

benefits <- c(500, 400, 300, rep(200, 5))

discount_factors <- (1 + 0.03) ^ - (0:7)

kpx <- c(1, cumprod(px[(65 + 1):(71 + 1)]))

sum(benefits * discount_factors * kpx)

1945.545

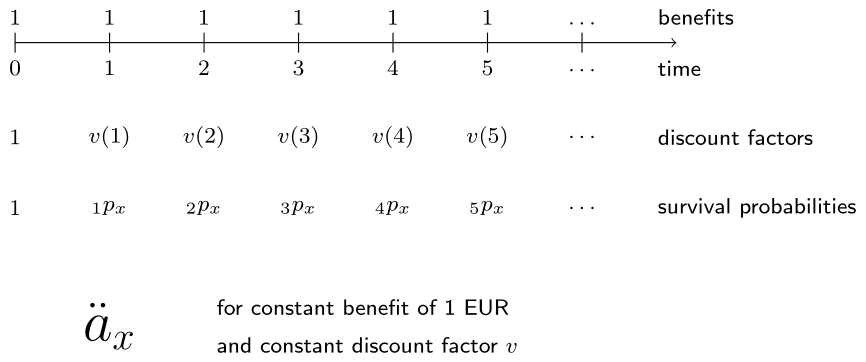

Whole life annuity due

Whole life annuity due: pay $c_k$ at beginning of year $(k+1)$.

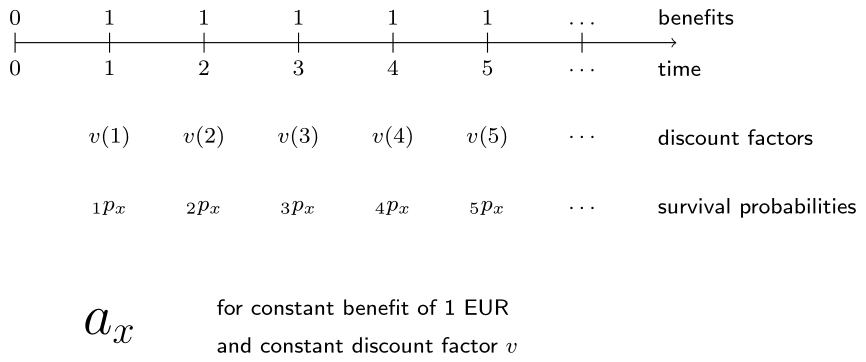

Whole life immediate annuity

Whole life immediate annuity: pay $c_k$ at end of year $(k+1)$.

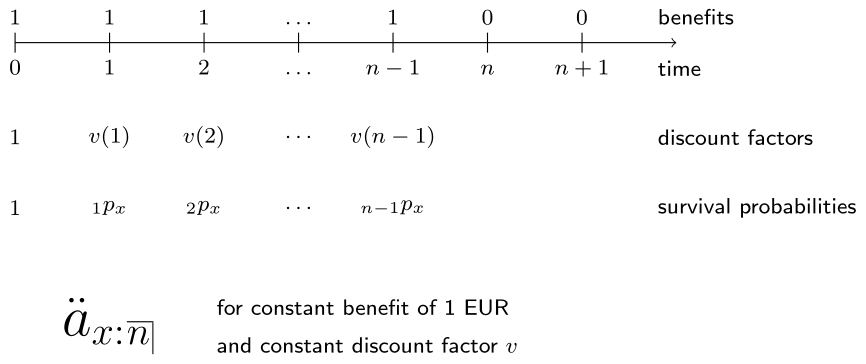

Temporary life annuity due

Temporary annuity due: maximum of $n$ years, at time $0$ until $n-1$.

Deferred whole life annuity due

Deferred whole life annuity due: no payments in first $u$ years.