The whole, temporary and deferred life insurance

Life Insurance Products Valuation in R

Katrien Antonio, Ph.D.

Professor, KU Leuven and University of Amsterdam

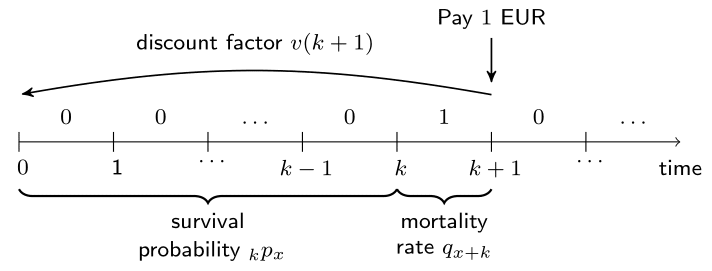

A series of one-year contracts

- What if?

- The benefit is $b_k$ EUR instead of 1 EUR?

- A series of one-year contracts instead of just one?

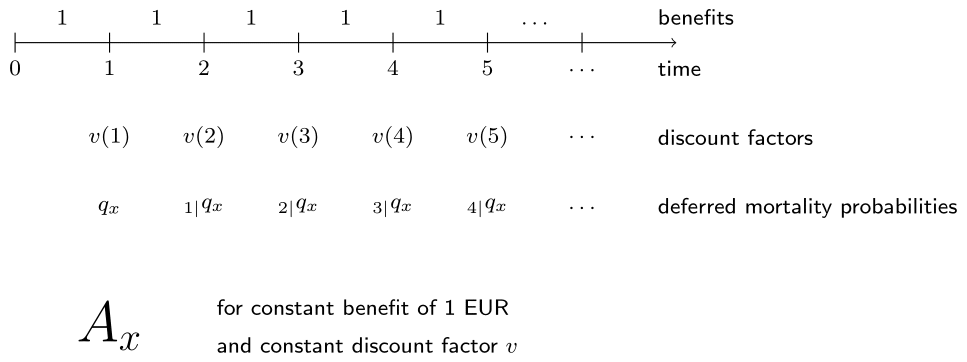

Whole life insurance

Whole life insurance: lifelong.

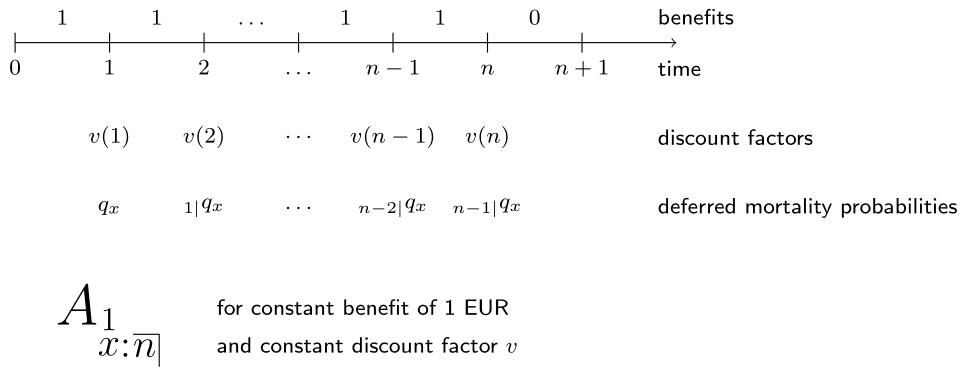

Temporary life insurance

Temporary (or: term) life insurance: maximum of $n$ years.

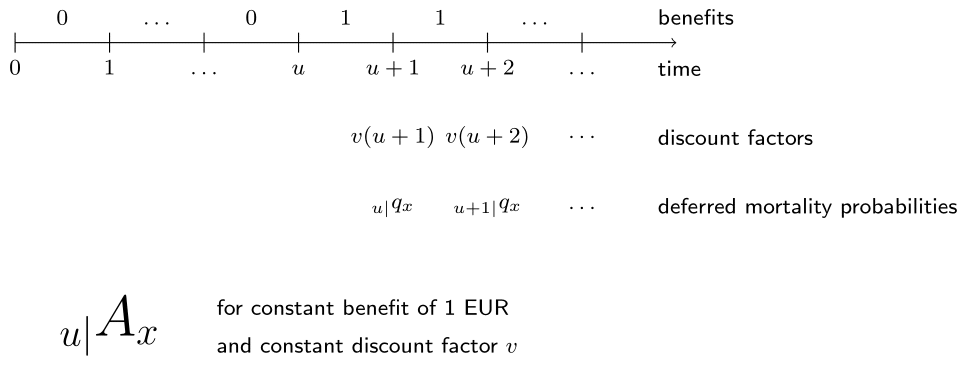

Deferred whole life insurance

Deferred whole life insurance: no payments in first $u$ years.