Sharpe ratio and Sortino ratio

Financial Trading in Python

Chelsea Yang

Data Science Instructor

Risk-adjusted return

- Make performance comparable among different strategies

- A ratio that describes risk involved in obtaining the return

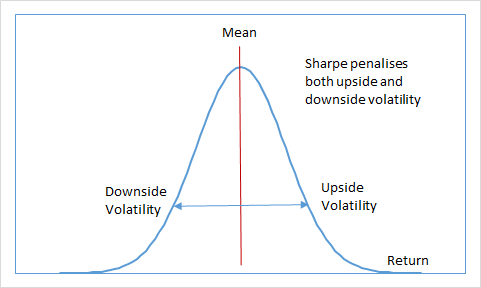

Limitations of Sharpe ratio

- Penalize both the "good" and "bad" volatility

- Upside volatility can skew the ratio downward

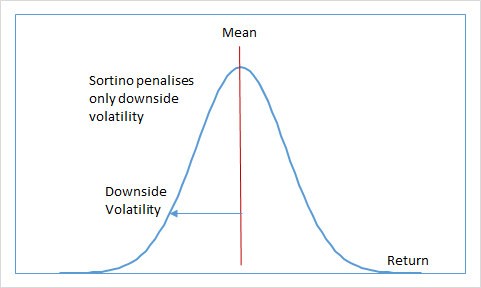

Sortino ratio

$$ \text{Sortino Ratio} = (R_p - R_r)/\sigma_d $$

- $R_p $: Return of a strategy, portfolio, asset, etc

- $R_r $: Risk-free rate

- $\sigma_d $: Downside deviation of the excess return ($R_p-R_f$)