Financial trading with bt

Financial Trading in Python

Chelsea Yang

Data Science Instructor

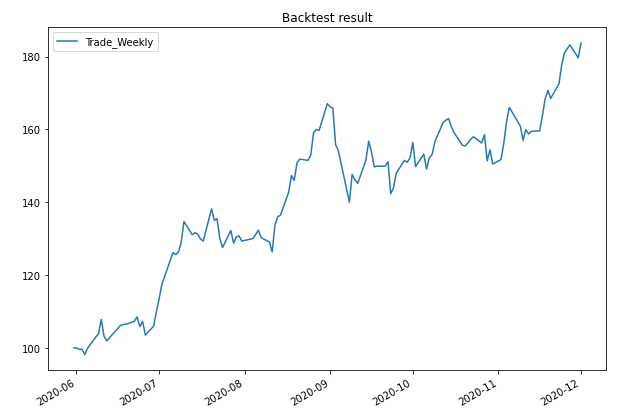

Evaluate the result

# Plot the result

bt_res.plot(title="Backtest result")

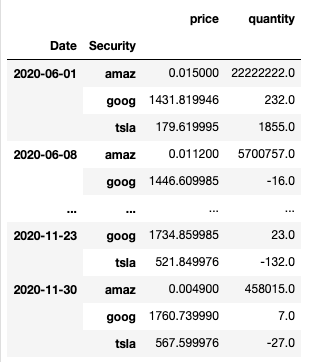

# Get trade details

bt_res.get_transactions()

Financial Trading in Python

Chelsea Yang

Data Science Instructor

# Plot the result

bt_res.plot(title="Backtest result")

# Get trade details

bt_res.get_transactions()