Drawdown

Financial Trading in Python

Chelsea Yang

Data Science Instructor

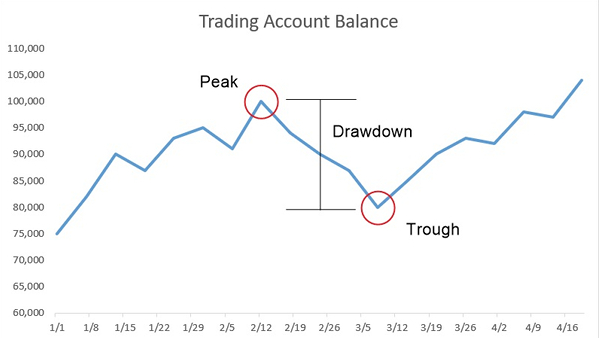

What is a drawdown?

A drawdown is a peak-to-trough decline during a specific period for an asset or a trading account.

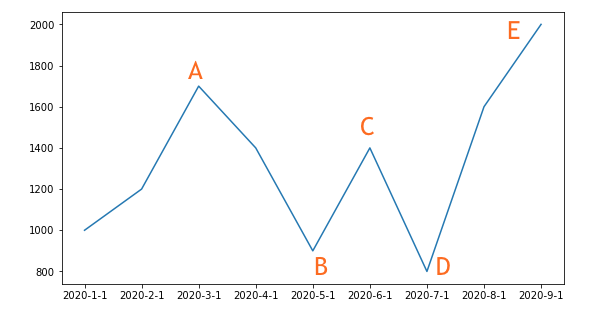

Max drawdown

Financial Trading in Python

Chelsea Yang

Data Science Instructor

A drawdown is a peak-to-trough decline during a specific period for an asset or a trading account.