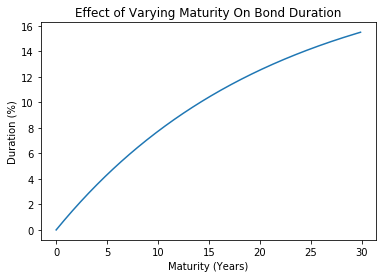

Factors affecting duration

Bond Valuation and Analysis in Python

Joshua Mayhew

Options Trader

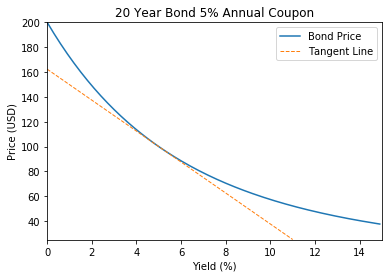

Duration as the slope of the tangent line

Duration is the derivative (rate of change) of price with respect to yield

The slope of the tangent line is the duration

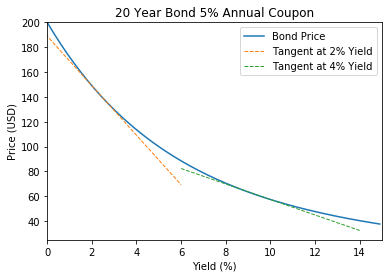

Bond yield vs. duration

- Bond price curve is steeper for lower yields

- Lower yields = higher sensitivity to interest rates = higher duration

Plotting bond maturity against duration

plt.plot(bond['bond_maturity'], bond['duration'])plt.xlabel('Maturity (Years)')plt.ylabel('Duration (%)')plt.title("Effect of Varying Maturity On Bond Duration")plt.show()