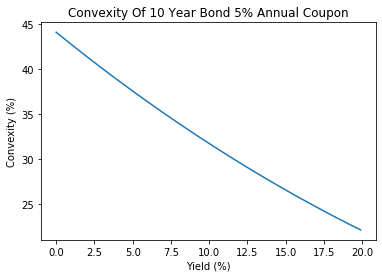

- 10 year bonds with 5% yield, first pays no coupon, second pays 10% coupon

price_1 = -npf.pv(rate=0.05, nper=10, pmt=0, fv=100)

price_up_1 = -npf.pv(rate=0.06, nper=10, pmt=0, fv=100)

price_down_1 = -npf.pv(rate=0.04, nper=10, pmt=0, fv=100)

convexity_1 = (price_down_1 + price_up_1 - 2 * price_1) / (price_1 * 0.01 ** 2)

price_2 = -npf.pv(rate=0.05, nper=10, pmt=10, fv=100)

price_up_2 = -npf.pv(rate=0.06, nper=10, pmt=10, fv=100)

price_down_2 = -npf.pv(rate=0.04, nper=10, pmt=10, fv=100)

convexity_2 = (price_down_2 + price_up_2 - 2 * price_2) / (price_2 * 0.01 ** 2)

print("Low Coupon Bond Convexity: ", convexity_1)

print("High Coupon Bond Convexity: ", convexity_2)

Low Coupon Bond Convexity: 99.89

High Coupon Bond Convexity: 64.09