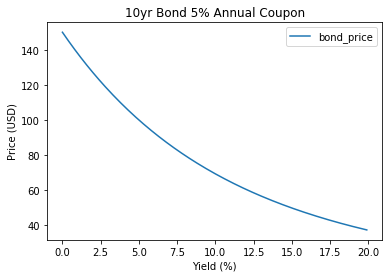

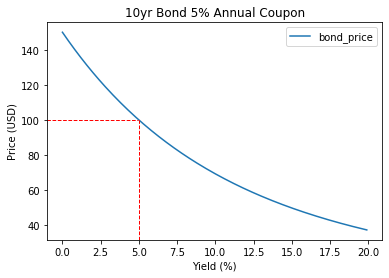

Bond prices vs. bond yields

Bond Valuation and Analysis in Python

Joshua Mayhew

Options Trader

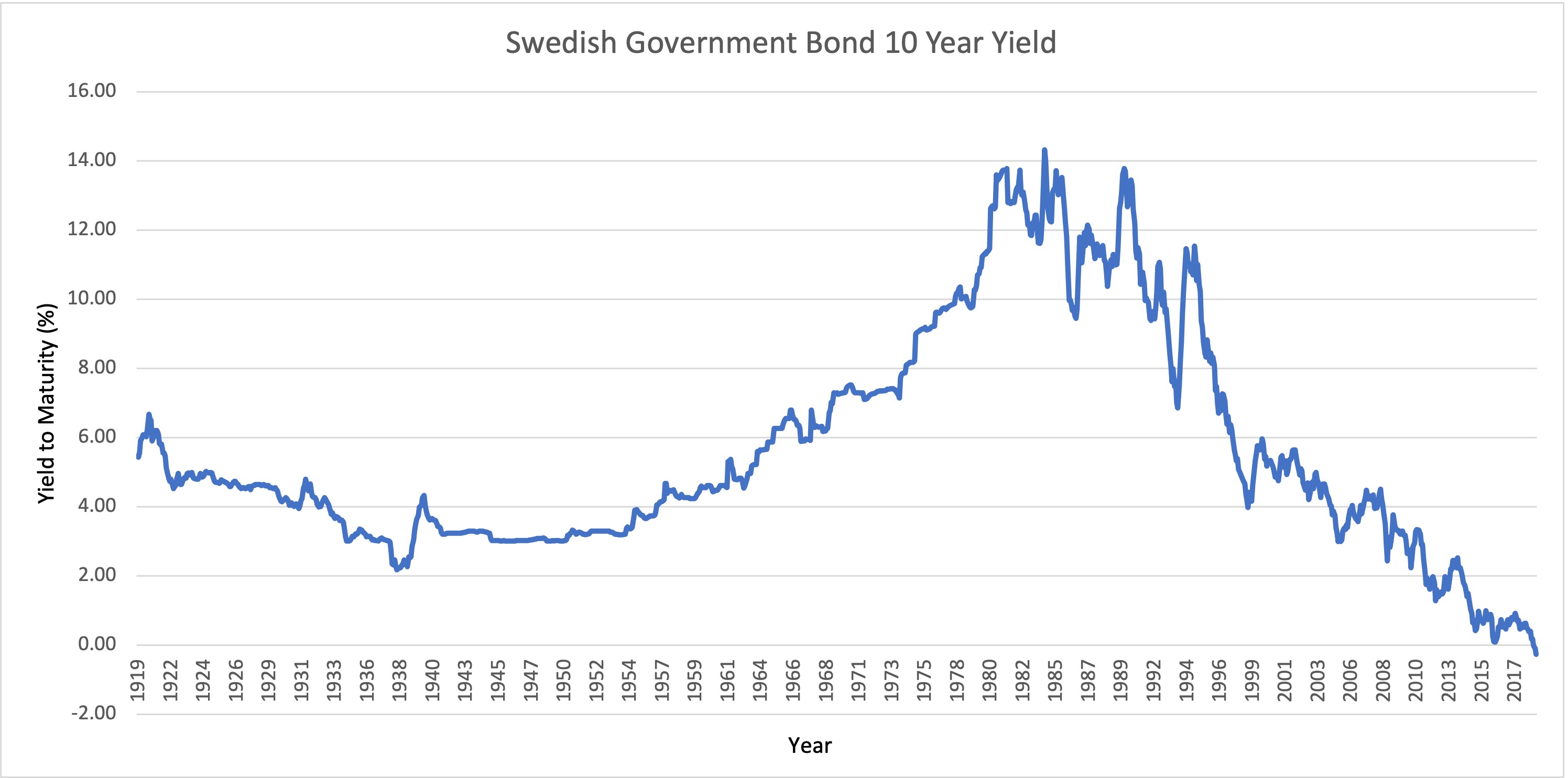

Historical government bond yields

Plotting bond prices vs. yields

plt.plot(bond['bond_yield'], bond['bond_price'])plt.xlabel('Yield (%)')plt.ylabel('Bond Price (USD)')plt.title("10 Year Bond 5% Annual Coupon")plt.show()

The relationship between price and yield

The relationship between price and yield

The relationship between price and yield

The relationship between price and yield