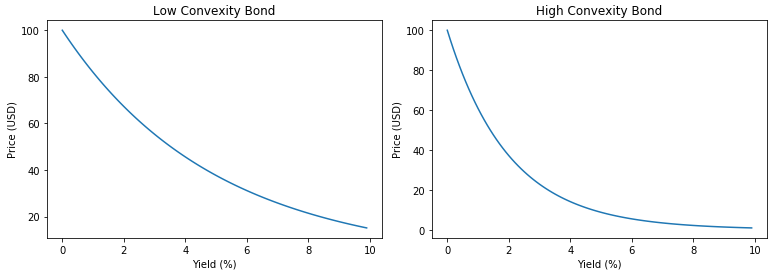

Convexity

Bond Valuation and Analysis in Python

Joshua Mayhew

Options Trader

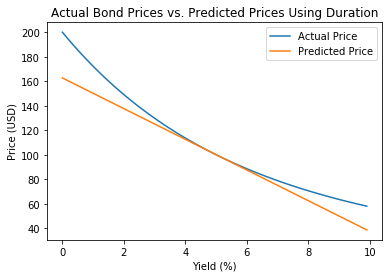

Plotting predicted vs. actual prices

Limitations of duration

What is convexity?

- Measures the curvature of bond prices

- Used to improve bond price prediction and risk measurement

- Higher convexity = more curved price/yield relationship