Coupon paying bonds

Bond Valuation and Analysis in Python

Joshua Mayhew

Options Trader

Coupon bond example

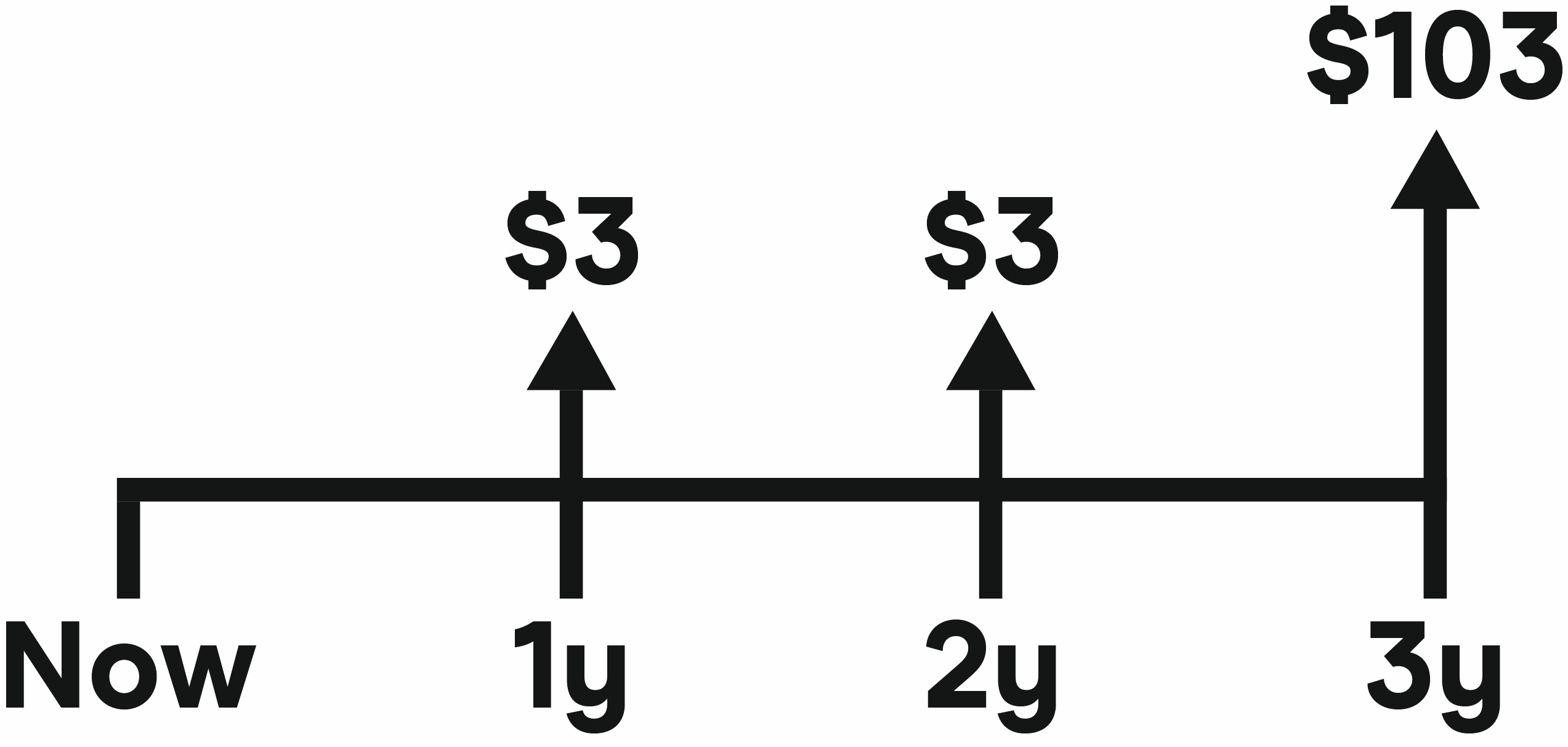

Take a 3 year bond with a 3% annual coupon, face value of USD 100, and yield of 4%:

WARNING: The coupon is fixed and doesn't change!

Bond Valuation and Analysis in Python

Joshua Mayhew

Options Trader

Take a 3 year bond with a 3% annual coupon, face value of USD 100, and yield of 4%:

WARNING: The coupon is fixed and doesn't change!